Understanding the True Challenges of Financing for SMEs Beyond Interest Rates

Understanding the True Challenges of Financing for SMEs Beyond Interest Rates

In recent years, the financial landscape for small and medium-sized enterprises (SMEs) in Japan has been marred by rising interest rates, prompting many business owners to express concerns about their borrowing prospects. However, a survey conducted by Yushi Daiko Pro, led by the company's CEO, Koutarou Okajima, indicates that the real issues haunting SMEs extend beyond the obvious anxiety around interest rates and accessibility of loans. Based on insights from a survey of 306 SME owners who had sought financing within the last three years, this article sheds light on the nuanced challenges inherent in the financing process.

Key Findings from the Survey

1. Practical Challenges in Securing Financing

The survey reveals that 27.5% of owners feel burdened by the inability to secure funding quickly, while 27.1% cite the daunting task of preparing necessary documentation, such as business plans. Additionally, 19.0% expressed anxiety around unclear approval criteria and evaluation standards that leave them in the dark during critical decision-making moments.

Surprisingly, although only 13.4% of business owners reported concerns about having insufficient collateral and 13.1% are worried about the implications of personal guarantees, the data suggest these issues are not sufficiently recognized, possibly because they often go unaddressed until major implications arise.

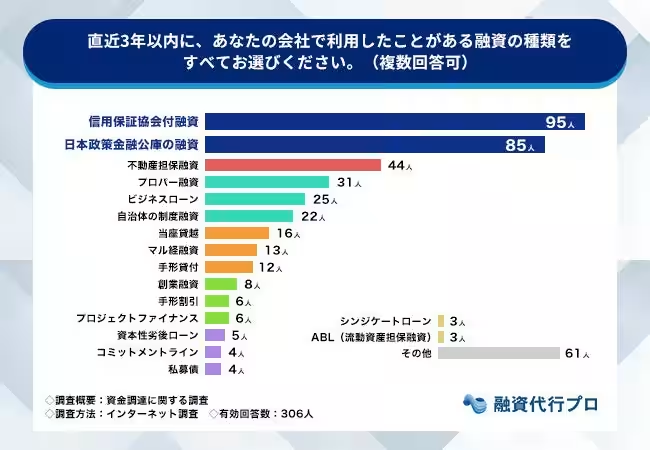

2. The Dominance of Institutional Financing

Recent trends indicate that many SMEs are opting for institutional financing methods such as loans backed by the Credit Guarantee Corporation (31.1%) and Japan Finance Corporation (27.8%). These routes are attractive as they provide comparatively easier access. Furthermore, there’s a notable reliance on non-guaranteed loans, including real estate-backed loans (14.4%) and proprietary loans (10.1%), which often carry stringent requirements like personal guarantees and collateral.

Business owners may find themselves focusing on immediate concerns like interest rates while overlooking the long-term ramifications of these financing conditions on their personal assets and livelihoods.

3. Reframing the Approach to Financing

A fundamental takeaway from both the survey findings and daily advisory practices is that the challenges surrounding financing do not align with self-identified issues by SME owners. The straightforward concerns regarding interest rates and procedural burdens overshadow the reality that the essence of strategic financing lies in designing the terms of borrowing rather than merely securing funds.

Each financial institution adopts varying criteria and methodologies for assessment, hence the process of acquiring funds has evolved into a consideration of 'which conditions to choose and from which lender to borrow.' This points to a pressing need for a well-informed approach grounded in an understanding of institutional characteristics and products.

Insights from Koutarou Okajima

As Koutarou Okajima underscores, “Many clients initially focus on the convenience of borrowing—such as favorable interest rates—yet frequently neglect to evaluate the potential future impact of collateral and personal guarantees on their financial health.” This sentiment accentuates the pressing need for a paradigm shift in the approach towards financing, where the focus must shift to understanding the consequences of conditions set by lenders and how they affect future operations.

In light of this, it is crucial for business owners to recognize the importance of thorough deliberation over the implications of the financial commitments they undertake. The intent should be to secure financing not solely based on attractiveness at the moment but to ensure that the derived conditions foster sustainable growth without jeopardizing personal resources.

Conclusion

Small business owners must navigate the complex world of financing with a comprehensive understanding of not only their immediate responsibilities but also the lasting implications these agreements bring. Working closely with experienced consultancy firms such as Yushi Daiko Pro can provide insights into effectively organizing one's financing strategy to align with both current needs and future growth prospects. By prioritizing structure over expedience, SMEs can better manage the challenges that lie beyond just securing a loan.

Company Overview:

- - Name: Yushi Daiko Pro

- - URL: https://financing.web-matching.com/

- - CEO: Koutarou Okajima

- - Location: 2-2 Minami-Aoyama, Minato-ku, Tokyo, Japan

- - Key Services: Financial consulting, loan consultancy, and development of banking financing content.

Topics Business Technology)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.