Understanding the Gap between Responsibility and Preparedness for Aging Parents' Assets

The Emotional Dissonance: Responsibility vs. Preparedness

A collaborative survey conducted by Famitra and Tokyo Gas has unveiled a significant disparity in awareness and preparedness regarding the aging of parents among their children. The research involved 1,697 participants aged between 40 and 60 whose parents are alive, aiming to assess how they perceive their roles in the future care and asset management of their parents.

Key Findings from the Survey

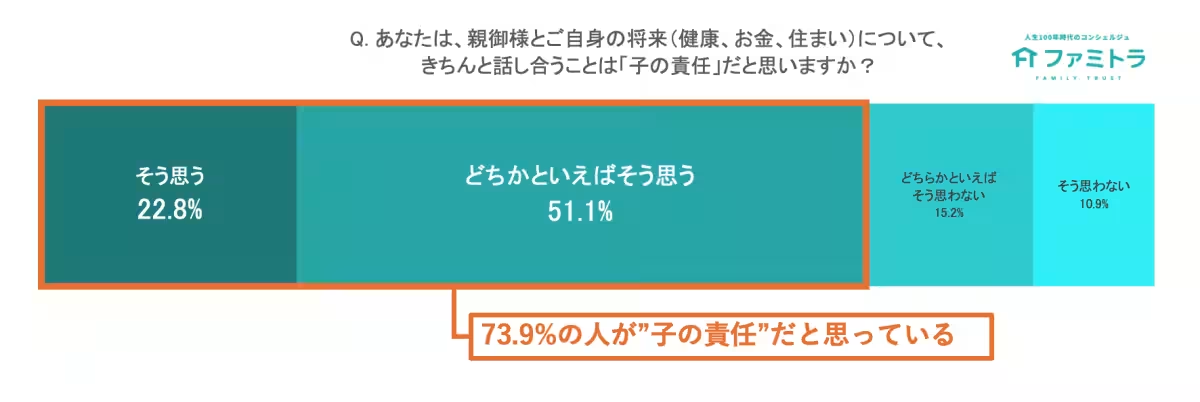

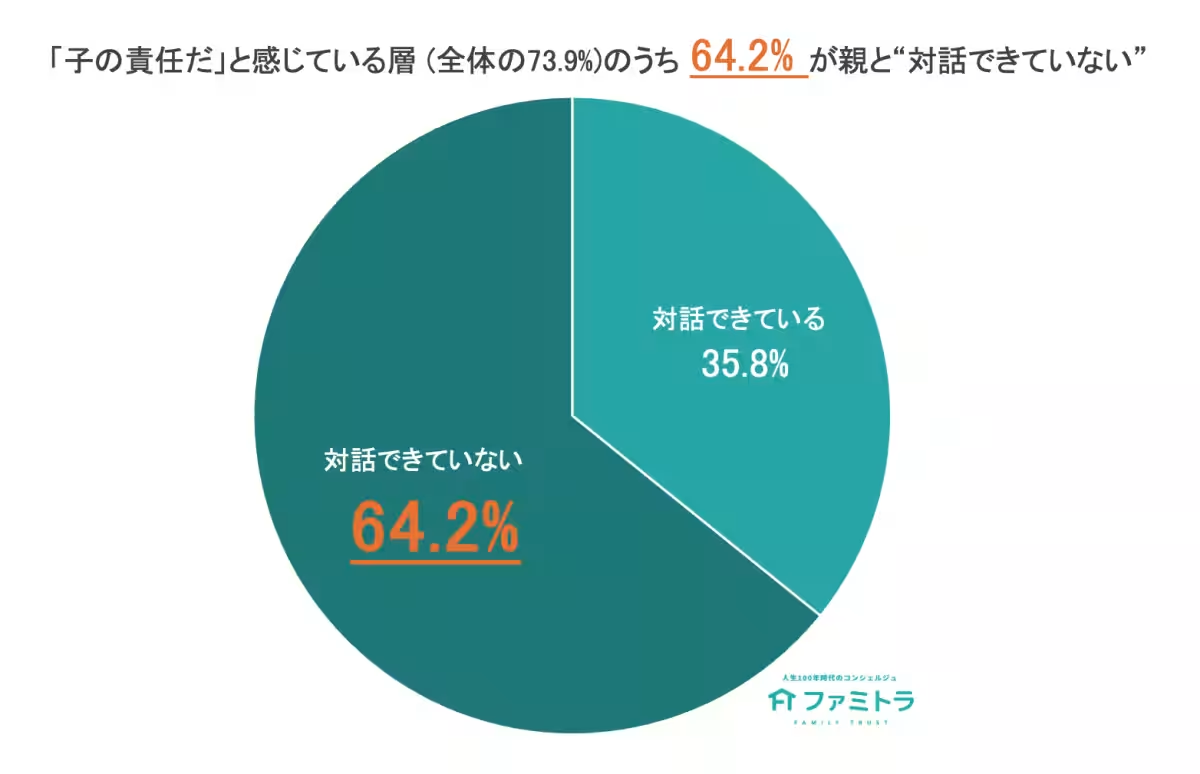

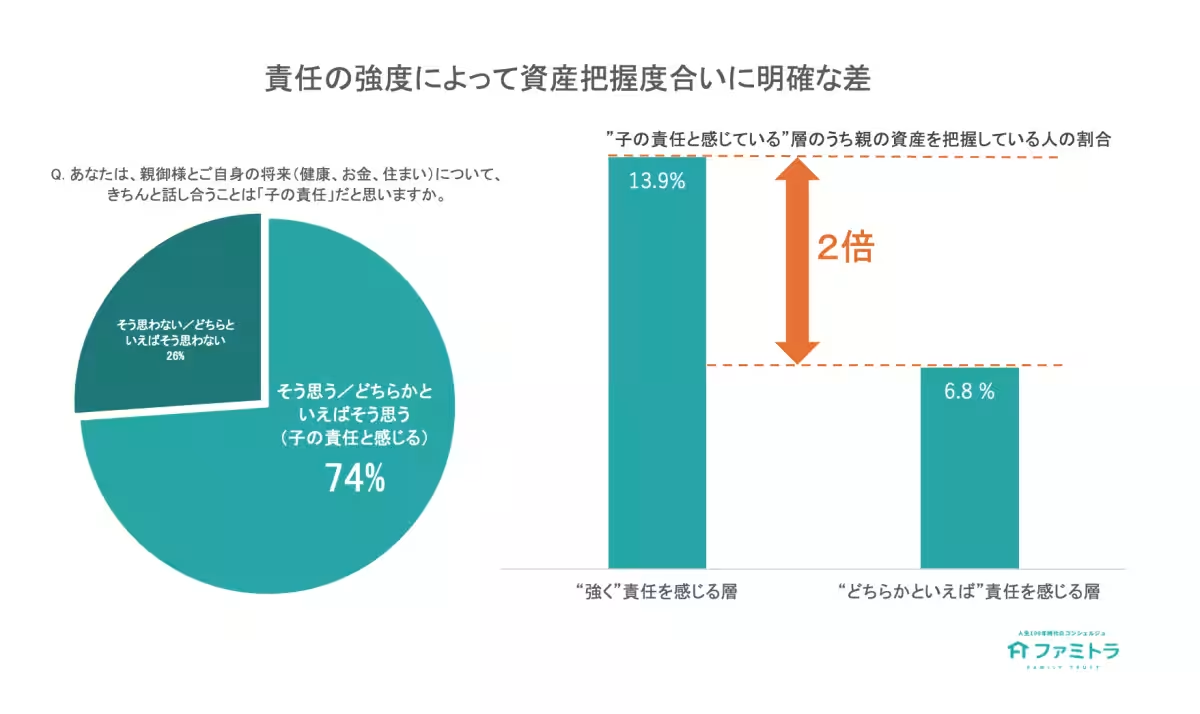

The survey results indicate that a striking 73.9% of respondents feel that discussing their parents' futures is a responsibility of the children. This indicates a strong sense of duty and affection. However, alarmingly, 57% of these individuals admitted to being unaware of their parents' financial status. Furthermore, among those who felt a sense of responsibility, 64.2% stated they had never had a concrete conversation with their parents about these matters. This disconnection between caring feelings and practical preparation leads to what the survey terms 'Silent Care Anxiety'.

An Analysis of Silent Care Anxiety

Famitra analyzes this phenomenon, suggesting that while children may have a heartfelt desire to care for their parents, many lack the initiative or knowledge to begin the conversation. This state perpetuates anxiety regarding elder care, as they grapple with uncertainty about their parents' financial health and future needs.

The Golden Age of Action

One crucial finding of the study is that the ideal time to begin these discussions—termed the 'Golden Age'—is the 50s. With many parents expecting lengthy retirements, it is increasingly evident that waiting until after a parent’s passing to discuss inheritance is no longer adequate. Instead, families should focus on what is being termed 'living inheritance' and maintaining financial vitality, which can transform anxiety into peace of mind for caregivers.

Urgent Reasons to Act Now

Based on the findings, here are ten compelling reasons children of aging parents need to take action now:

1. The Responsibility Gap

Although 74% feel a responsibility towards their parents, over 60% report having no specific discussions yet, highlighting an urgent need for communication.

2. The Source of Anxiety

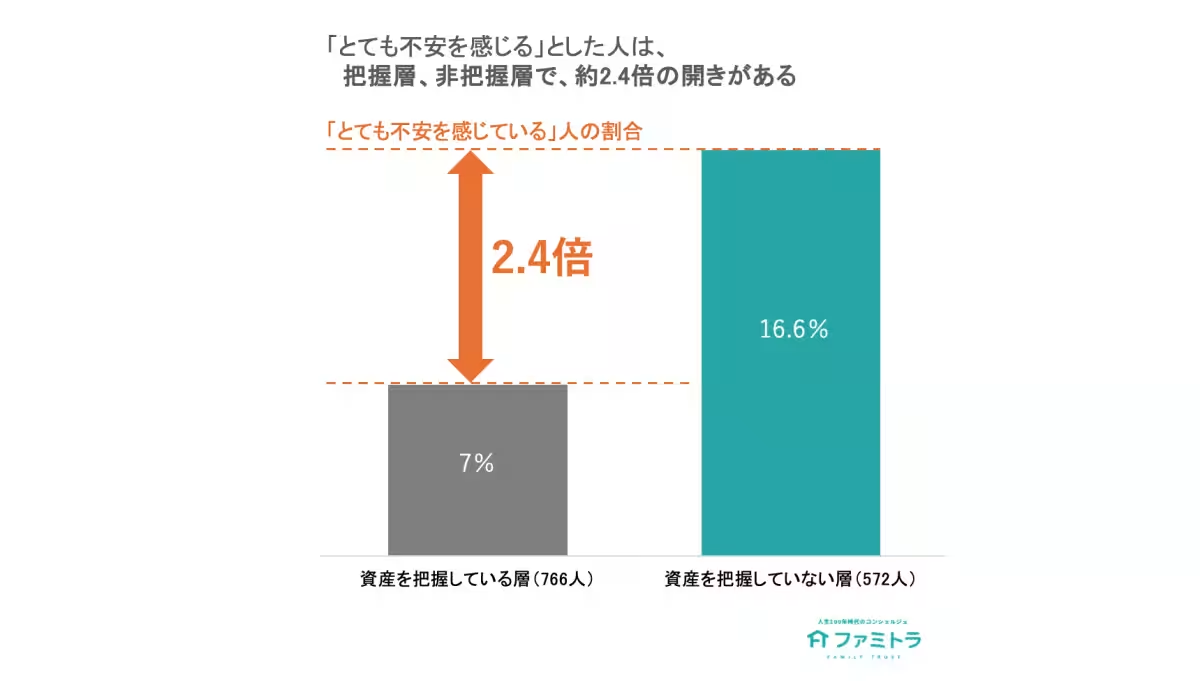

Children who do not understand their parents' assets are significantly more anxious about their financial futures—our data shows they are more than twice as likely to feel unease.

3. Misconceptions about Inheritance

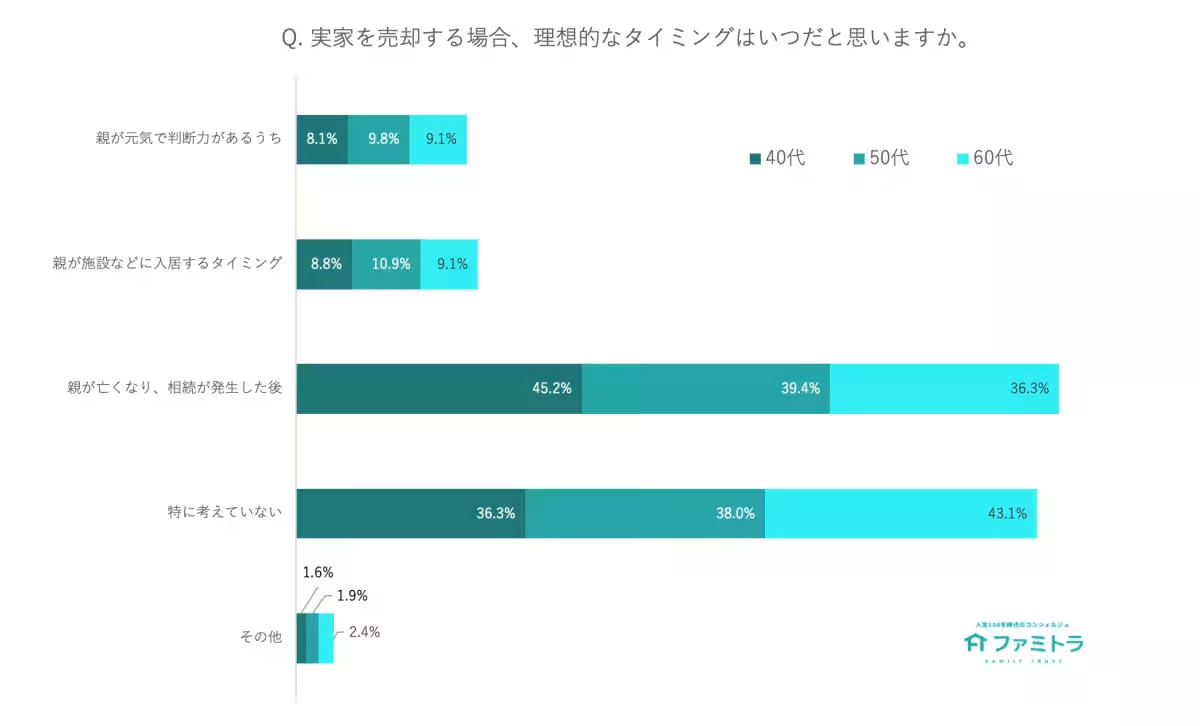

Approximately 40% of respondents dream of selling the family home posthumously, which poses the risk of disputes and asset freezes.

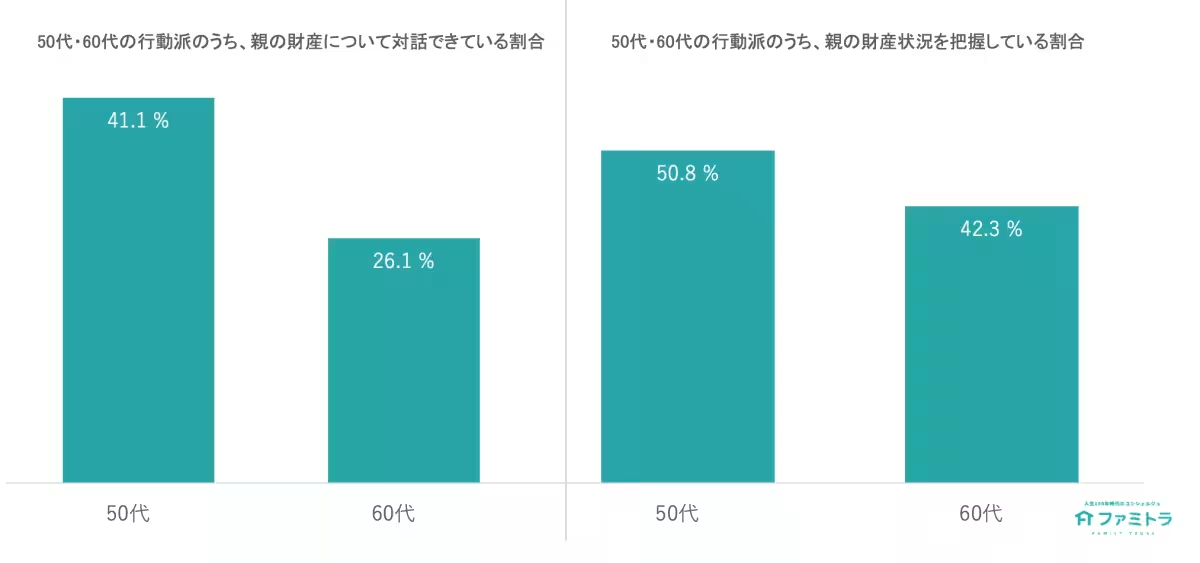

4. The Right Time to Step Up

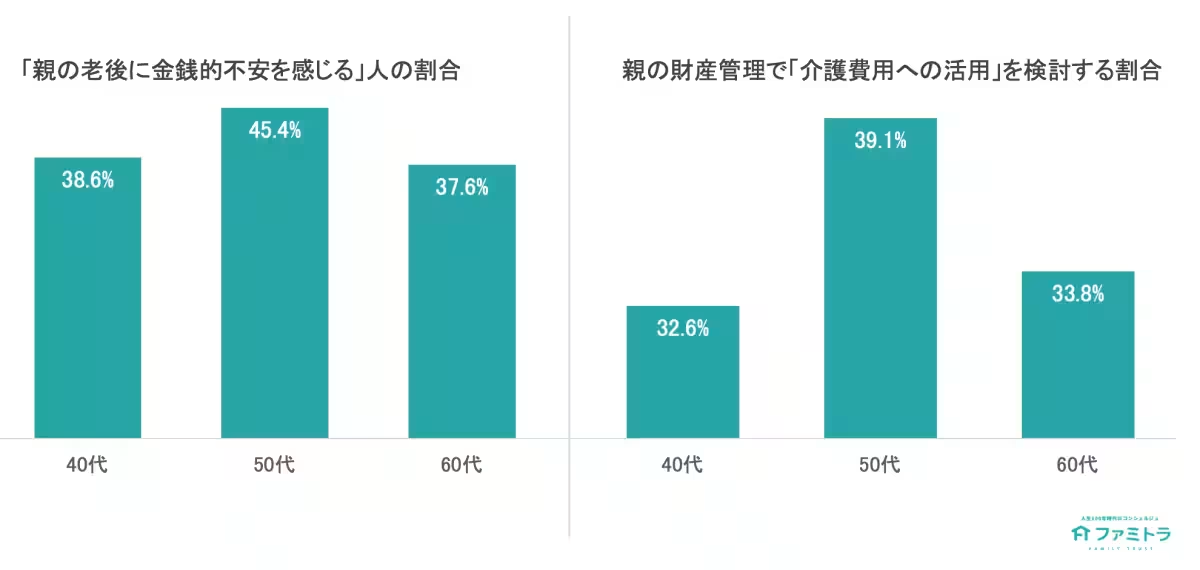

The 50s peak as the age where children feel the most uncertainty and recognize their responsibilities towards their aging parents’ finances. This age group is often where individuals start to confront the real implications of elder care.

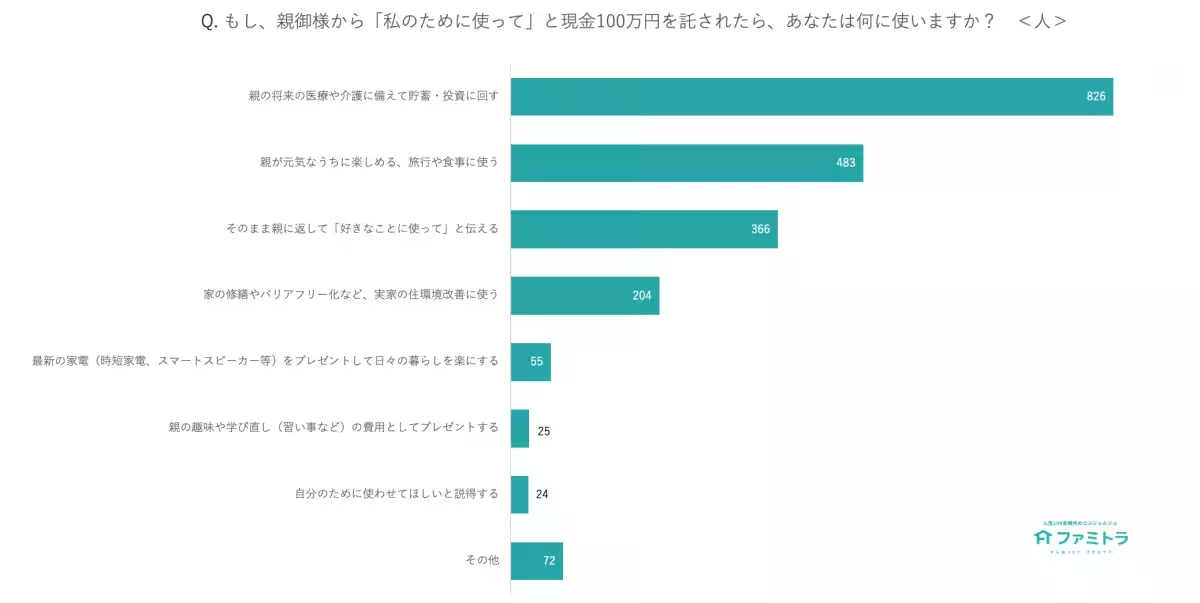

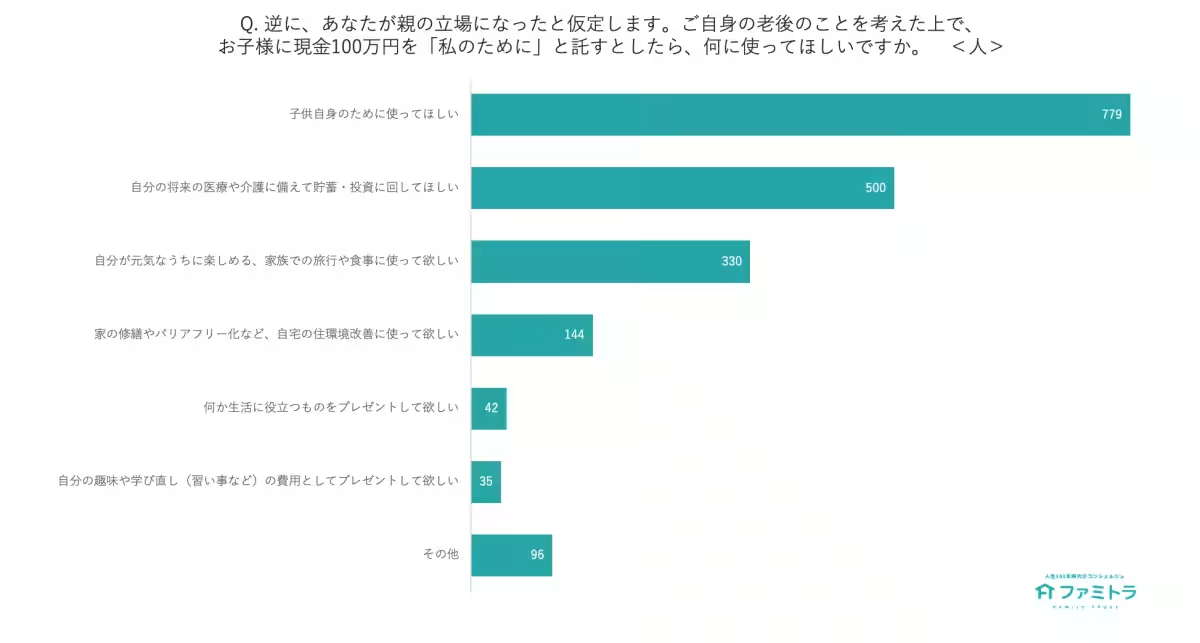

5. Misaligned Expectations

When asked, children often prioritize saving for their parents' care, while many parents wish for their children to use the funds for personal needs, highlighting the need for clearer communication.

6. Real Responsibility

Those demonstrating a strong sense of responsibility have usually already started conversations about future planning, unlike those who merely feel a vague obligation.

7. Understanding True Urgency

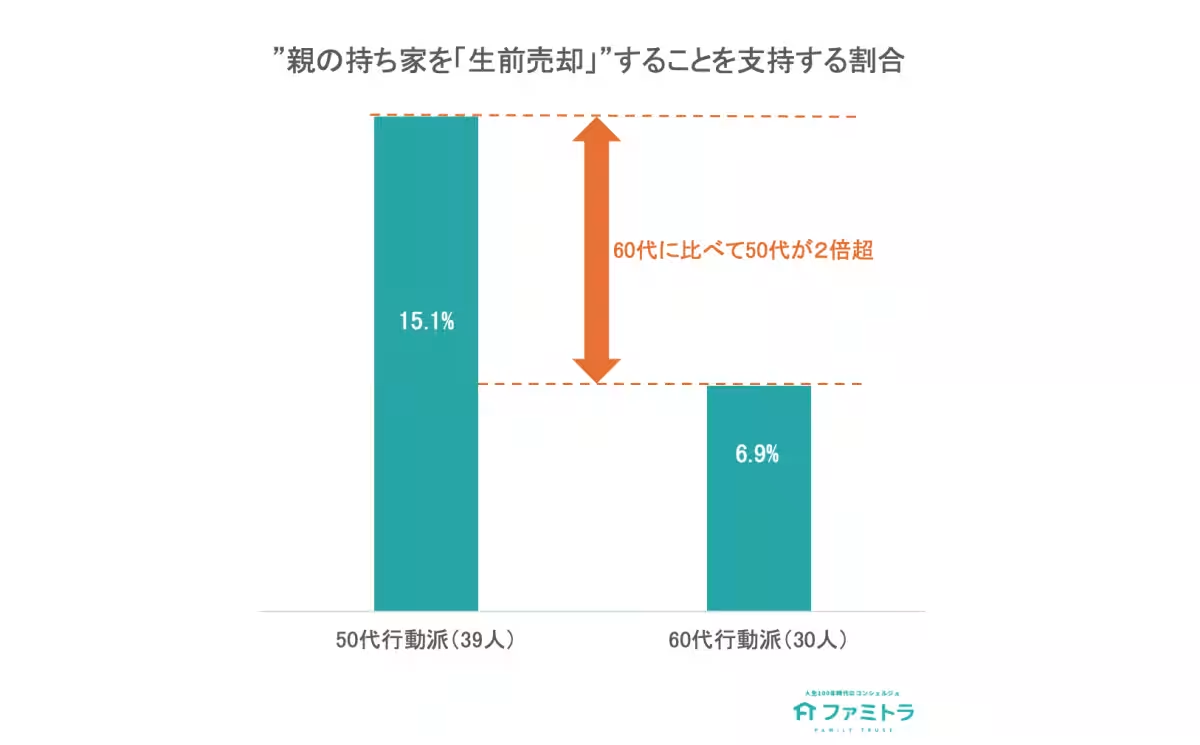

Individuals who recognize the importance of acting in their 50s have better communication and understanding of their parents' assets compared to those who delay until their 60s or later.

8. The Value of Living Inheritance

Children informed about their parents’ assets are significantly more likely to consider 'family trusts' as a preparatory measure.

9. Break Down Barriers

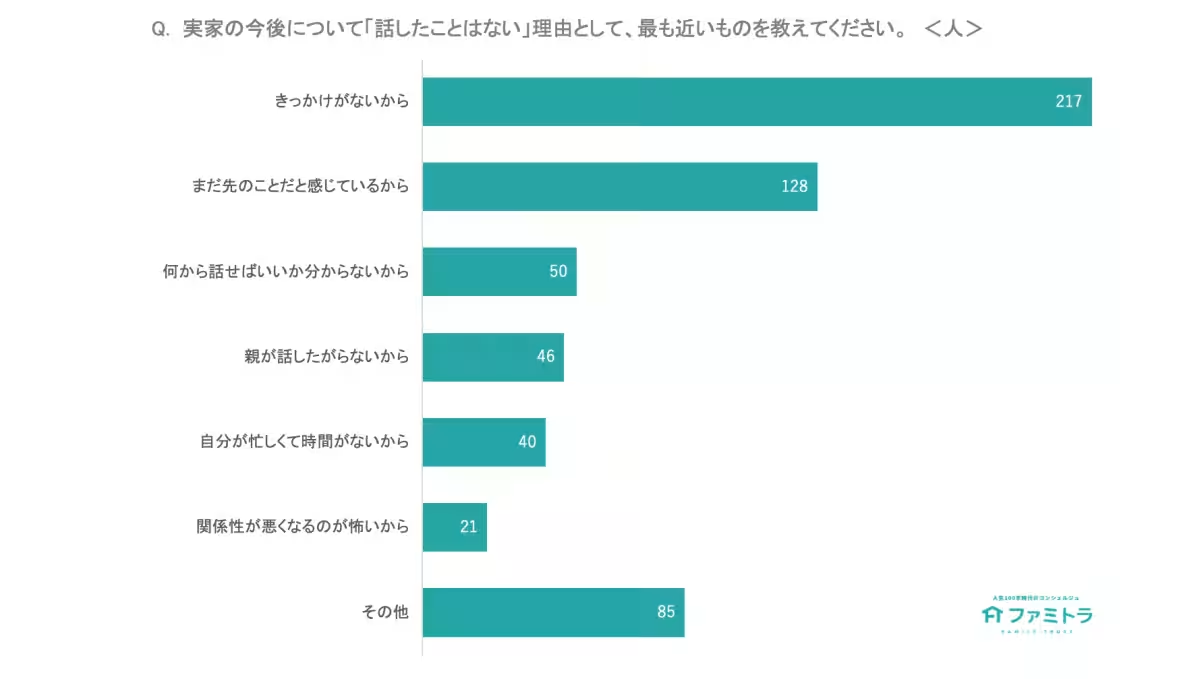

Interestingly, the primary barrier against discussing these issues is not a fear of conflict but rather the absence of 'conversation starters.' Many are eager for reasons to talk about the future.

Conclusion

The investigation clearly illustrates a divide between children's feelings of responsibility and their lack of preparation, resulting in 'Silent Care Anxiety.' Understanding and uncovering this anxiety is crucial, especially as it peaks in the 50s. Famitra advocates for opened discussions about the 'health of their finances' while parents are still able, promoting 'living inheritance' as a new standard for peace of mind within families. The hope is that this research will serve as a catalyst for many families to start vital conversations about the future and their shared responsibilities.

Topics People & Culture)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.