New Report Reveals the Profit Landscape and Success Factors for 55 Companies Entering Agriculture

Introduction

In recent years, there has been a noticeable trend of companies from varying industries entering the agricultural sector. A recently published report by Archetype Inc., centered in Minato-ku, Tokyo, sheds light on the motivations, challenges, and dynamics of this transition. The comprehensive study assesses 55 key players in agriculture, unveiling insights into their profit margins, strategic fit, and connectivity factors that dictate their success or failure.

Background of the Investigation

Japan's agricultural landscape is undergoing significant shifts. According to data, the number of agricultural workers has declined by 230,000 over just five years, correlating with a growing trend of corporate farmers. In stark contrast, the number of agricultural corporations has surged by 57% from 8,690 in 2000 to 13,630 expected by 2024. This shift represents an emerging opportunity for industries outside of farming to capitalize on agricultural practices.

Large-scale mergers and acquisitions (M&A) underscore this trend. A recent example is Idemitsu Kosan’s planned acquisition of Agro Kanesho for approximately 23 billion yen, scheduled for November 2024. Similarly, SOMPO Holdings intends to acquire Agricultural Research Institute for around 13.8 billion yen by December 2025. However, it's not just about entry; notable exits from the agricultural domain have also been witnessed. SoftBank's sale of its e-kakashi business and Fujitsu's discontinuation of key services for Akisai highlight that navigating this space is fraught with difficulty.

Report Overview

The report titled 'Agricultural Entry and Diversification Strategy Survey Report 2026' spans 43 pages and categorizes the 55 companies into 13 segments, including sectors like agricultural chemicals, general trading, IT, and agri-tech, among others. It aims to answer a crucial question: "Why do some companies succeed in agriculture while others fail?" The findings provide a structured analysis based on public information such as medium-term management plans and press releases.

Chapter 1: The Importance of Agriculture Now

The report opens by examining the structural transformation within domestic agriculture, emphasizing the shift from individual farmers to corporate entities. It outlines the current scale of the food business industry, valued at approximately 227 trillion yen while evaluating the 55 companies across six dimensions: strategic clarity, resource allocation, decision-making benchmarks, pathways to commercialization, external collaborations, and data/AI utilization. It reveals a marked difference in the approach of firms entering agriculture compared to peers across other sectors, with 45% classified as a 'passive group' compared to 17% across all industries.

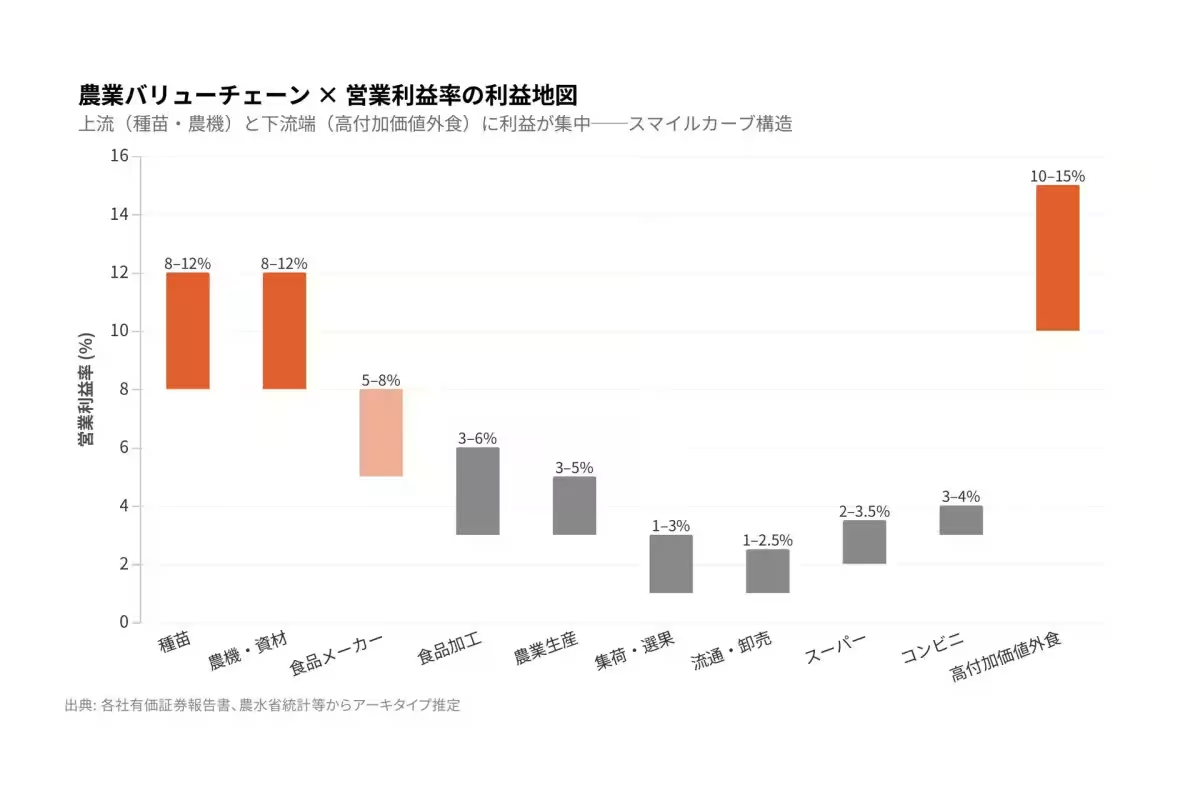

Chapter 2: Profit Map of the Agricultural Value Chain

This section visualizes the typical operating profit margins across ten layers of the agricultural value chain. It highlights the reasons behind the significant structural differences, such as the concentration on intellectual property and brand equity. Moreover, the report designates four key directions where profit pools are currently shifting—ranging from pesticides to bio-stimulants, data platforms for smart agriculture, direct-to-consumer distribution channels, and carbon credit markets, showcasing a dynamic agricultural landscape.

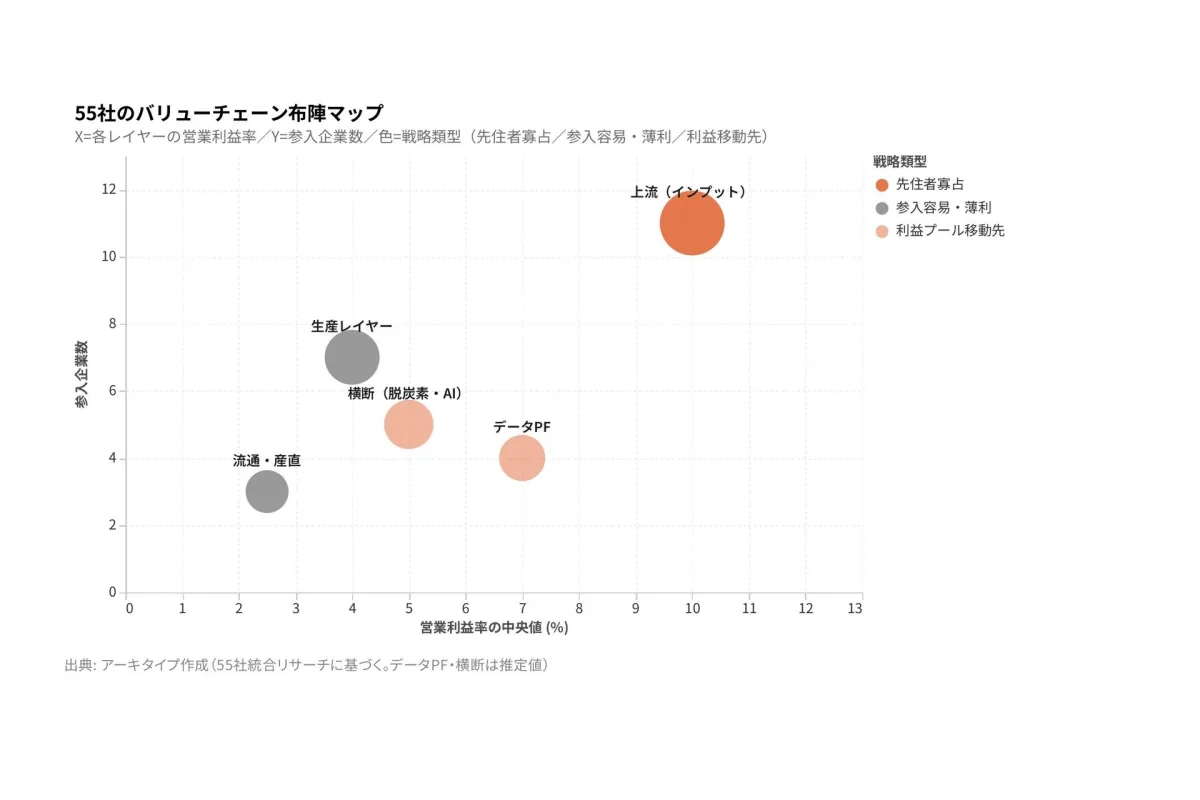

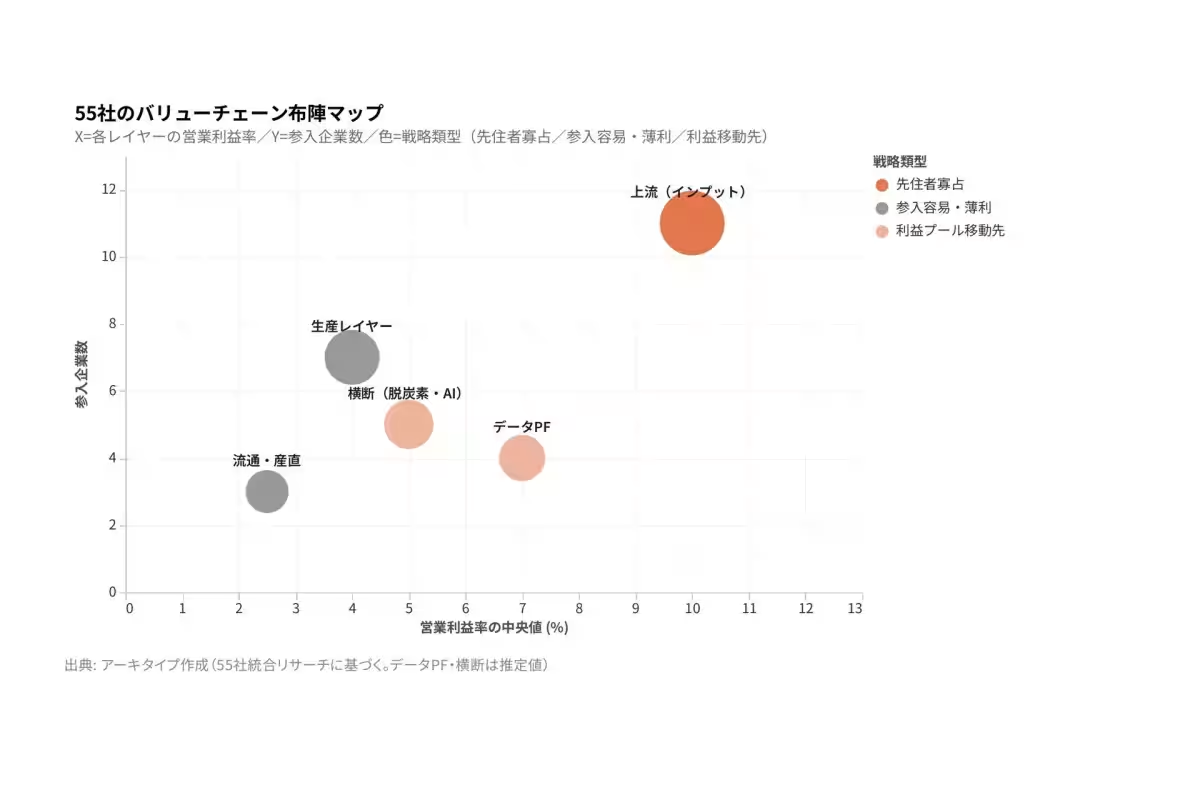

Chapter 3: Positions Targeted by 55 Companies

The report categorizes the 55 companies into five clusters based on their value chain positions: upstream (inputs), production layer, data platforms, distribution/direct sales, and cross-segment dynamics involving AI and decarbonization. Leading firms such as Kubota, Marubeni, and Sumitomo Corporation feature prominently due to their strategic fit across operational dimensions.

Chapter 4: Predictive Framework of Success and Failure

The unique framework proposed in the report for predicting success or failure is based on ‘connectivity points’ and ‘layer suitability’. Companies are sorted into five quadrants: alignment champions, M&A winners, core business players, mismatch cases, and in-house developers. The nuances between these groups provide insight into what drives success in the sector.

Chapter 5: Practical Models for Multi-Industry Entries

For companies from manufacturing, finance, IT, retail, and construction sectors, this section outlines practical steps and real-world case studies to guide their entry into agriculture, using examples from Idemitsu Kosan, SOMPO, and others.

Chapter 6: Steps for the Next 10 Months

The report ends by recommending a three-year plan targeting the initial 10 months for businesses without connectivity points, detailing essential sequential actions towards successful agricultural entry.

Conclusion

As the report concludes, Ryuhiko Kanno, CEO of Archetype, comments on how the success of agricultural entry is reliant more on a company's inherent connectivity points and their alignment with desired entry layers rather than sheer technological prowess or resource availability. The insights are not only applicable within agriculture but can also extend to sectors like semiconductors and new energy initiatives, establishing a framework for diverse industries looking to explore untapped territories.

For those seeking to delve deeper into this analysis, Archetype also offers a self-assessment tool, enabling companies to evaluate their new business potential against industry benchmarks. Visit Archetype's website for further information and resources.

Topics Other)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.