Investigation Reveals Crisis: One in Three Face Mortgage Issues During Divorce

Investigation Reveals Crisis: One in Three Face Mortgage Issues During Divorce

In a detailed survey conducted by Improvement Inc., a company based in Minato City, Tokyo, that specializes in voluntary sale services, alarming insights have emerged regarding mortgage challenges during divorce proceedings. The survey gathered responses from 202 individuals who had taken out mortgages during their marriage and were either divorced or in the process of divorce. About 35% reported having faced significant issues related to their mortgages during this challenging time.

Background and Purpose of the Survey

With rising housing prices and an increase in dual-income households, many couples have opted for shared debts or joint mortgages to purchase their homes. However, during divorce, critical decisions regarding the future of the home—such as whether to sell it or to whom the mortgage should be transferred—often become contentious points, leading to serious disputes. Drawing from numerous inquiries received, Improvement Inc. aimed to understand the prevailing issues regarding how individuals are dealing with their mortgages post-divorce, who they consult for advice, and the general awareness of voluntary sale options.

Summary of Findings

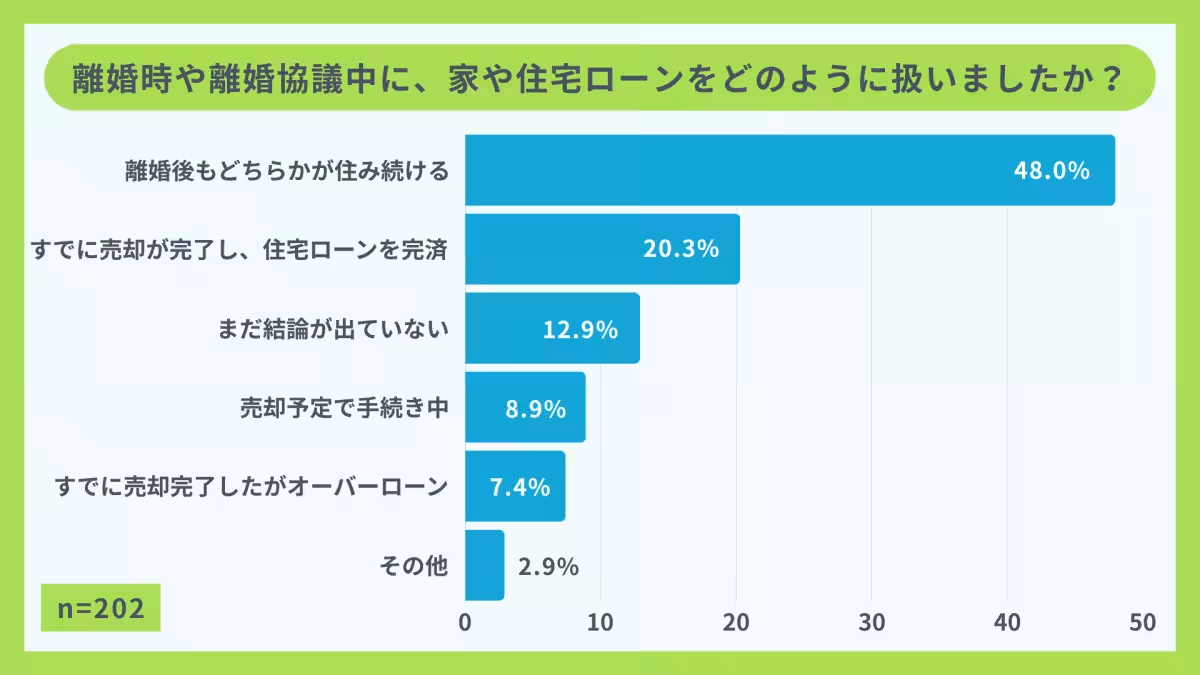

Handling of Properties Post-Divorce

Regarding the handling of homes post-divorce, 48% of respondents chose to continue living in the home, while about 20% found themselves in situations where they either still owed more on the mortgage after selling or were uncertain about the future. This indicates a complex web of mortgage troubles that many are experiencing during and after their divorce.

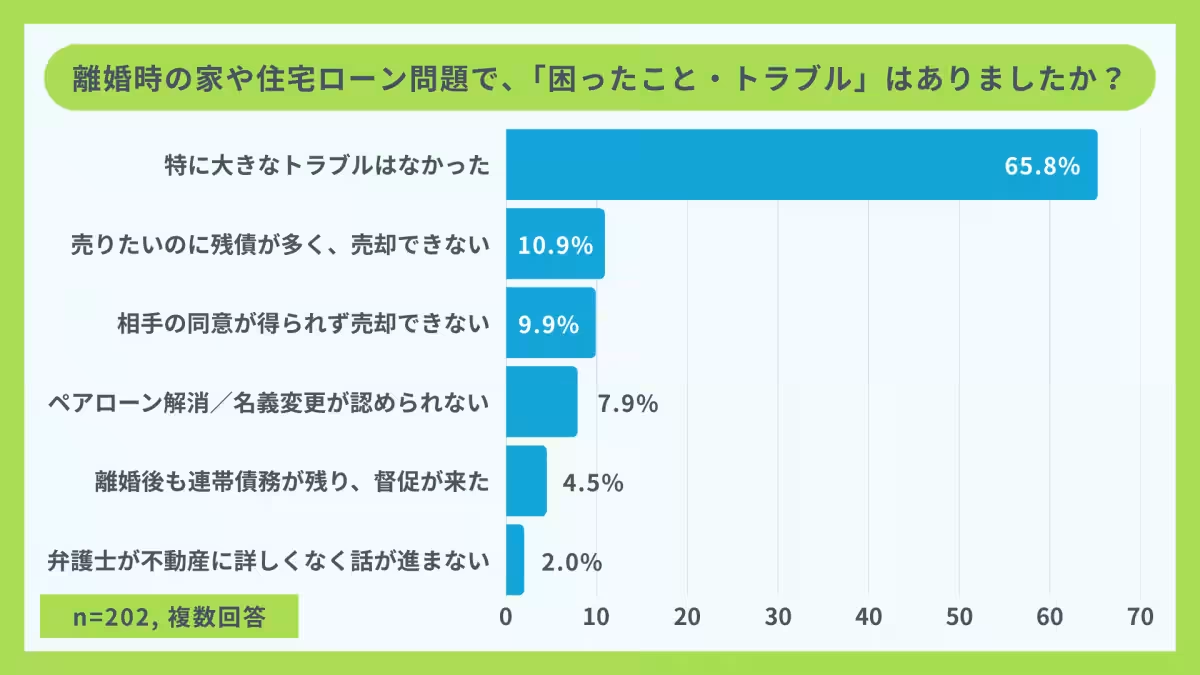

Experience of Issues

Approximately one-third, or 35%, of participants reported facing stressful complications when dealing with their mortgages during divorce. Issues such as wanting to sell but being unable to do so, complications in changing the mortgage name, or persistent shared debts were most frequently cited, specifically among those with joint financing.

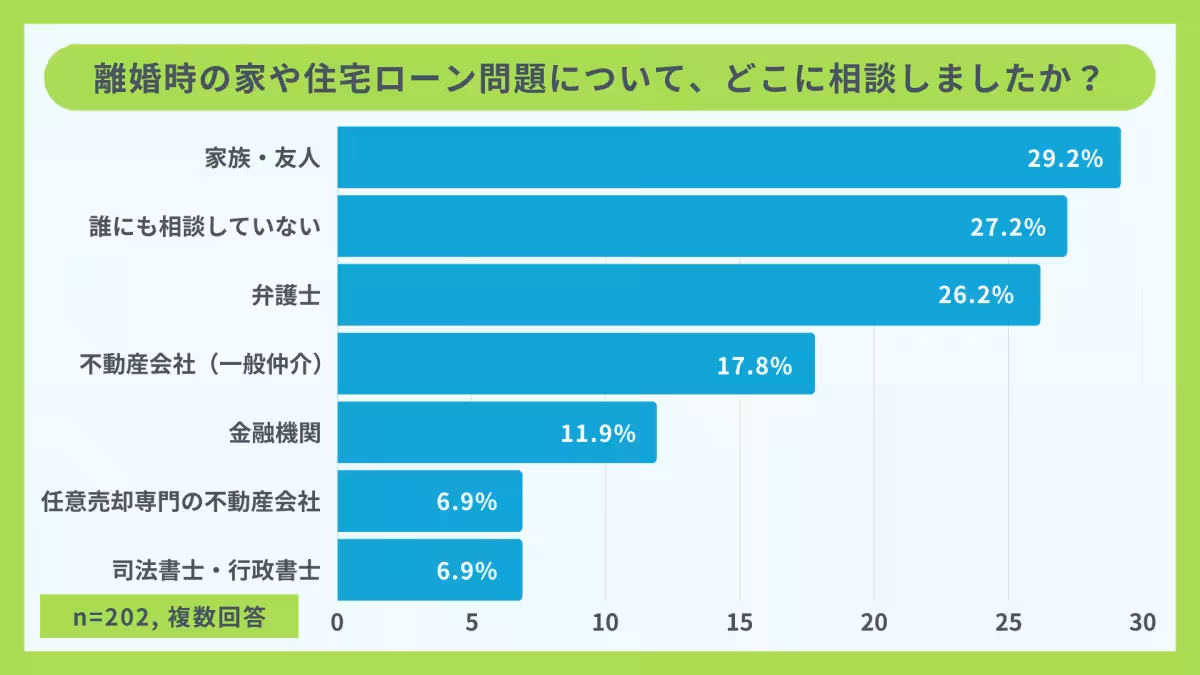

Consultation Trends

When seeking advice, respondents predominantly turned to family and friends (29.2%), while 27.2% revealed they sought no consultation at all. Only about 7% consulted professionals who specialize in voluntary sales or mortgage complications, highlighting a significant gap in accessing expert advice.

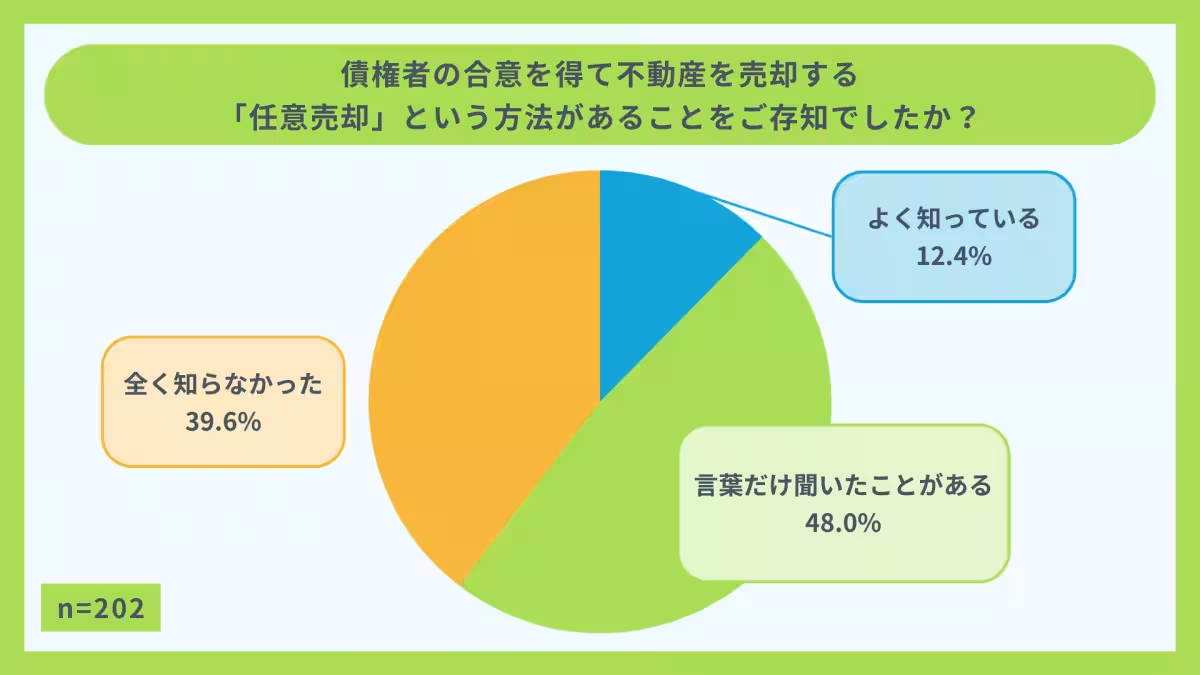

Awareness of Voluntary Sales

Only 12% of respondents were well-informed about the voluntary sale process, while a staggering 39.6% admitted to having no knowledge of it at all. This lack of understanding may delay appropriate actions, particularly when individuals are considering parting with their homes.

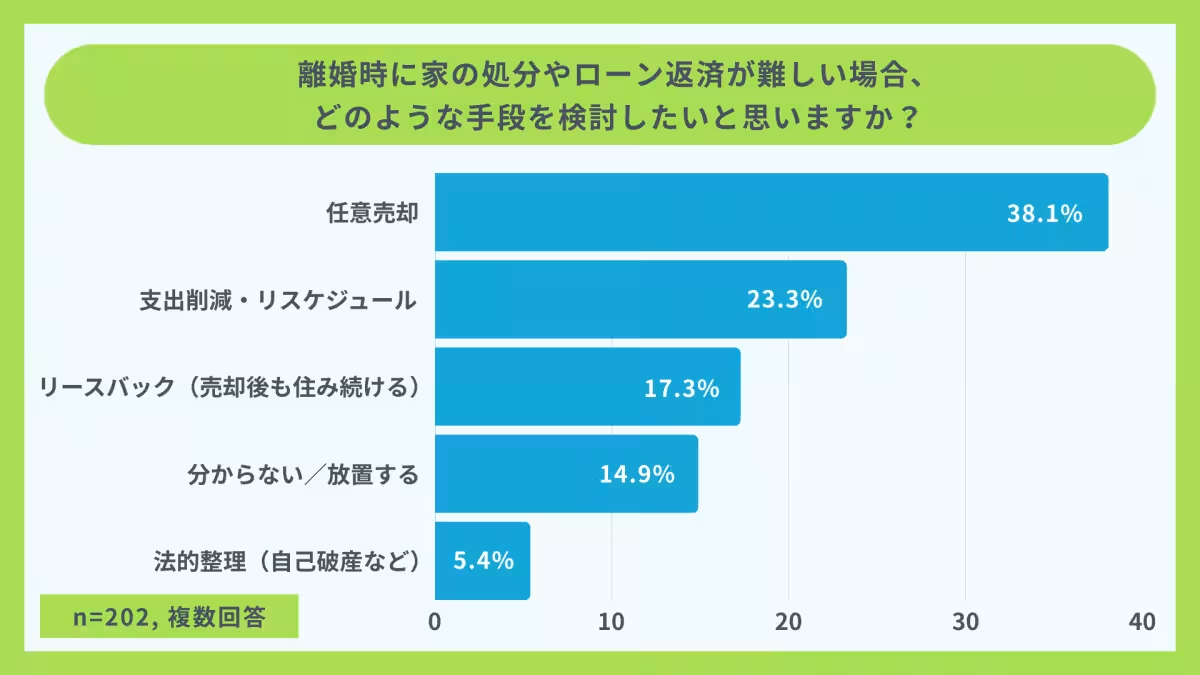

Further Complications in Decision Making

When asked about their potential actions if payment became too difficult, only 38.1% expressed interest in considering voluntary sale options, while about 15% noted they might either ignore the situation or were unsure of what to do. This delay in seeking professional help could escalate their mortgage issues.

In-Depth Analysis of Survey Results

1. Post-Divorce Property Management:

Following divorce, nearly half of the respondents opted to reside in the same home, but the existence of “over-mortgaged loans” and unresolved decisions persist among many, emphasizing the financial strain involved.

2. Risks of Joint Mortgages:

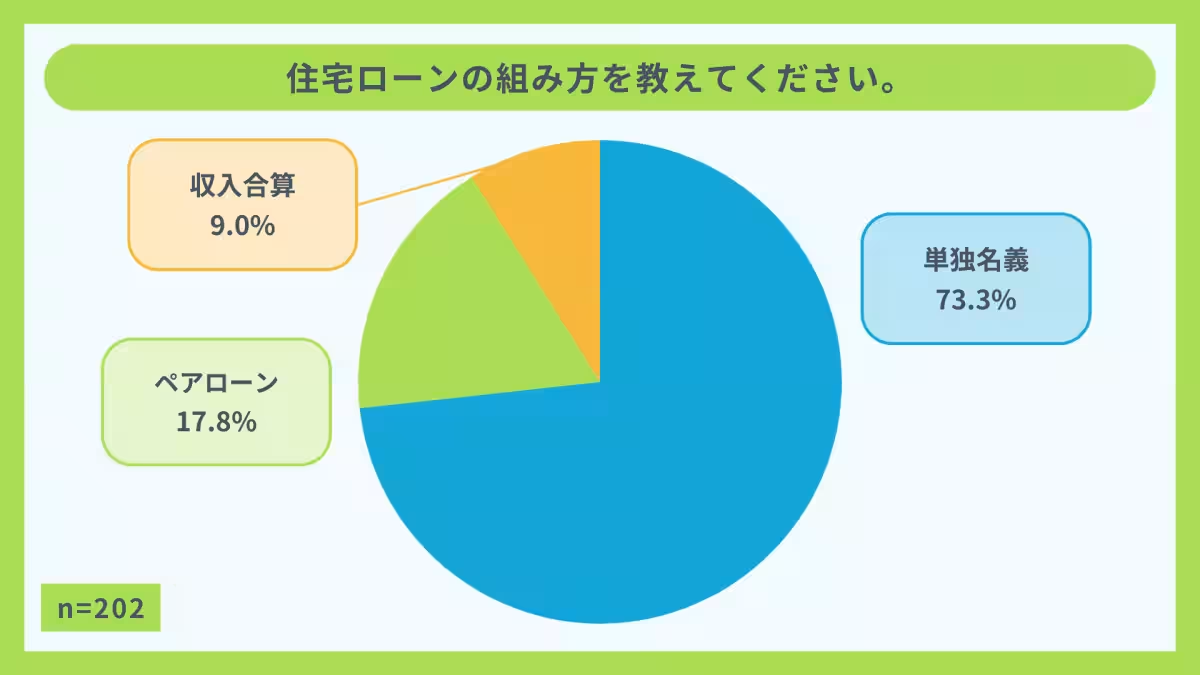

With 27% of the respondents using joint or combined income mortgages, the risks of not being able to transfer the loan to one party or the burden of continued joint debt became apparent, leading to additional stress.

3. Experiences of Distress:

Around 35% encountered various issues, including being unable to sell due to excessive debt or lacking mutual consent from an ex-partner.

4. Gaps in Professional Consultation:

A significant share relied on advice from friends and family, with a minimal number consulting specialists in voluntary sales, indicating a potential oversight in seeking the right type of guidance.

5. Lack of Knowledge on Options:

A vast proportion of respondents were unaware of voluntary sale options, a method that could facilitate quicker resolution without needing to resort to conventional sales or auctions.

6. Considering Options for Resolution:

While many consider voluntary sales when facing financial hardship, a notable proportion remains unsure of their options, suggesting a need for increased educational efforts about financial management during divorce.

Personal Accounts of Distress

Aside from quantitative data, qualitative responses illustrated deep and personal struggles. Many cited instances where they were unable to switch loan names due to bank refusals, leading to financial and emotional distress as their previous partners failed to cooperate.

Conclusion

Shinya Adachi, the CEO of Improvement Inc., emphasized the need for greater awareness among couples regarding their rights and options when dealing with mortgage issues during divorce. He pointed out that many enter agreements without fully understanding the ramifications, particularly concerning joint debts. This lack of foresight can lead to unresolved financial burdens that persist well beyond their marriage.

For individuals facing these complex issues, it remains crucial to seek out specialized advice early in the divorce process to navigate their options effectively and avoid unnecessary hardships.

Survey Overview

- - Subject: Investigation on Mortgage Issues During Divorce

- - Conducted by: Improvement Inc.

- - Period: April 18 - May 20, 2025

- - Method: Internet-based survey

- - Participants: Adults aged 20 and above with mortgage experience during marriage

- - Valid Responses: 202 individuals

Topics Other)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.