The Diverging Financial Perspectives of Generation Z and the Bubble Generation

Understanding Financial Perspectives: Gen Z vs. Bubble Generation

In a significant exploration of financial values between two distinct age groups, the Generation Z (age 20-30) and the Bubble Generation (age 55-60), a recent study by WOZ, LLC sheds light on how these generations approach asset formation and financial decision-making.

As various financial contexts evolve, including the expansion of new NISA accounts aimed at encouraging youth investment, interest in asset formation is surging among the younger generation. This enthusiasm is often juxtaposed against the older generation's deep-rooted experiences from past economic booms, creating a fascinating generational divide.

Survey Overview

Conducted from June 2 to June 3, 2026, the survey received responses from 1,040 employees equally split between both generations who are actively engaged in economic asset formation via savings and investments. The survey aims to delve into the informational resources and financial values shaping their asset-building strategies.

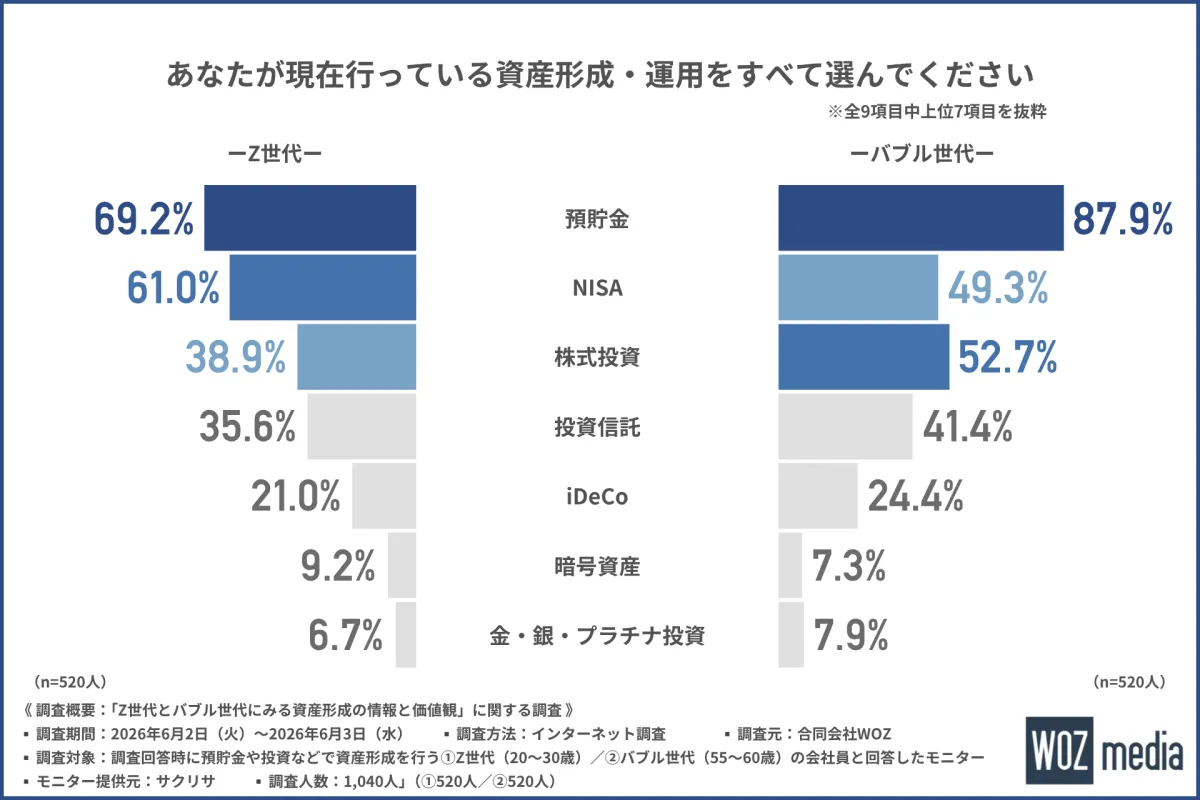

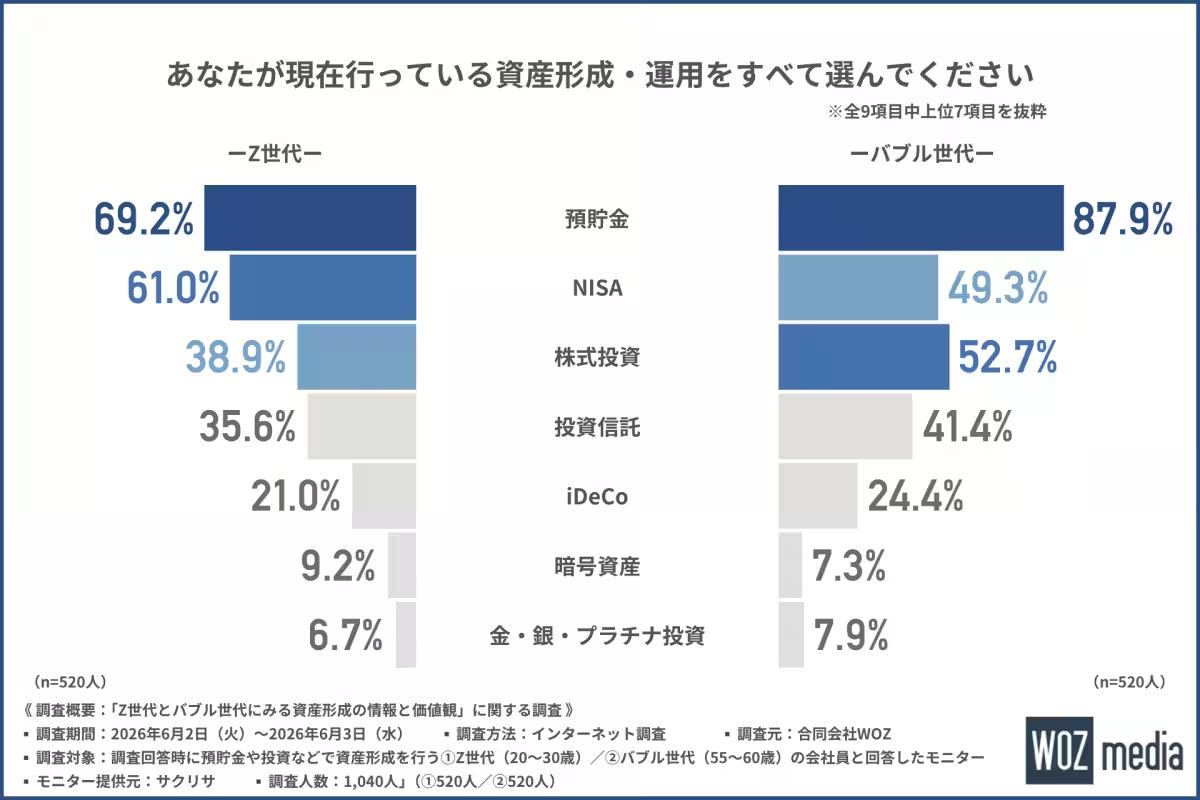

Key Findings on Asset Formation Methods

Both generations primarily rely on savings as their asset formation method, with significant statistical distinctions:

- - Gen Z: 69.2% utilize savings, 61.0% invest through NISA accounts, and 38.9% participate in stock market investments.

- - Bubble Generation: 87.9% depend on savings, followed by 52.7% actively investing in stocks, and 49.3% using NISA accounts.

The emphasis on savings shows a notable increase among the Bubble Generation, reflecting a broader focus on security compared to Gen Z's tendency towards innovative investment options like NISA, indicating a shift in preferences and strategies between the generations.

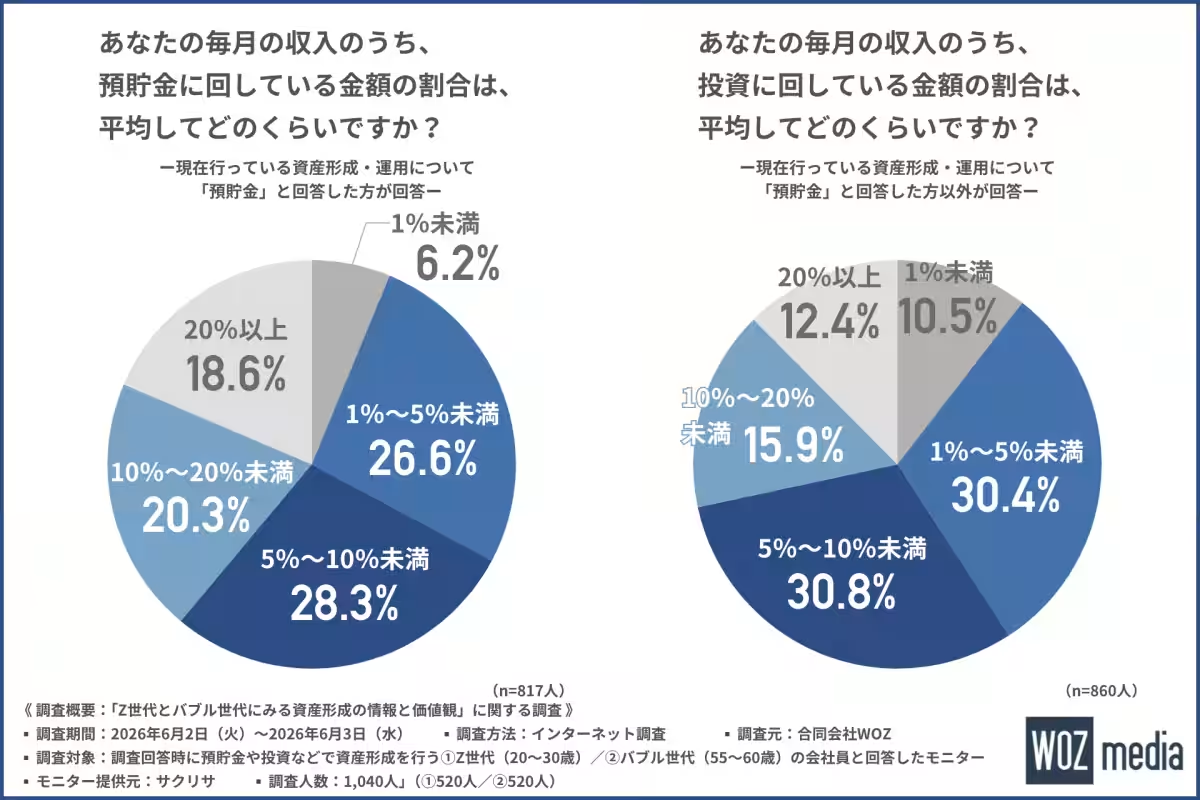

Monthly Savings Allocation

The survey investigated how much income each group allocates to savings:

- - Approximately half of respondents in both generations contribute less than 10% of their income to savings.

- - Savings plans indicate cautious financial habits, with some respondents saving 10%-20% of their income indicating a contrasting risk appetite.

In terms of investment contributions, the findings reveal:

- - 60% of respondents invest less than 10% of their income, suggesting a conservative approach towards investment strategies, although about 30% invest more than this amount.

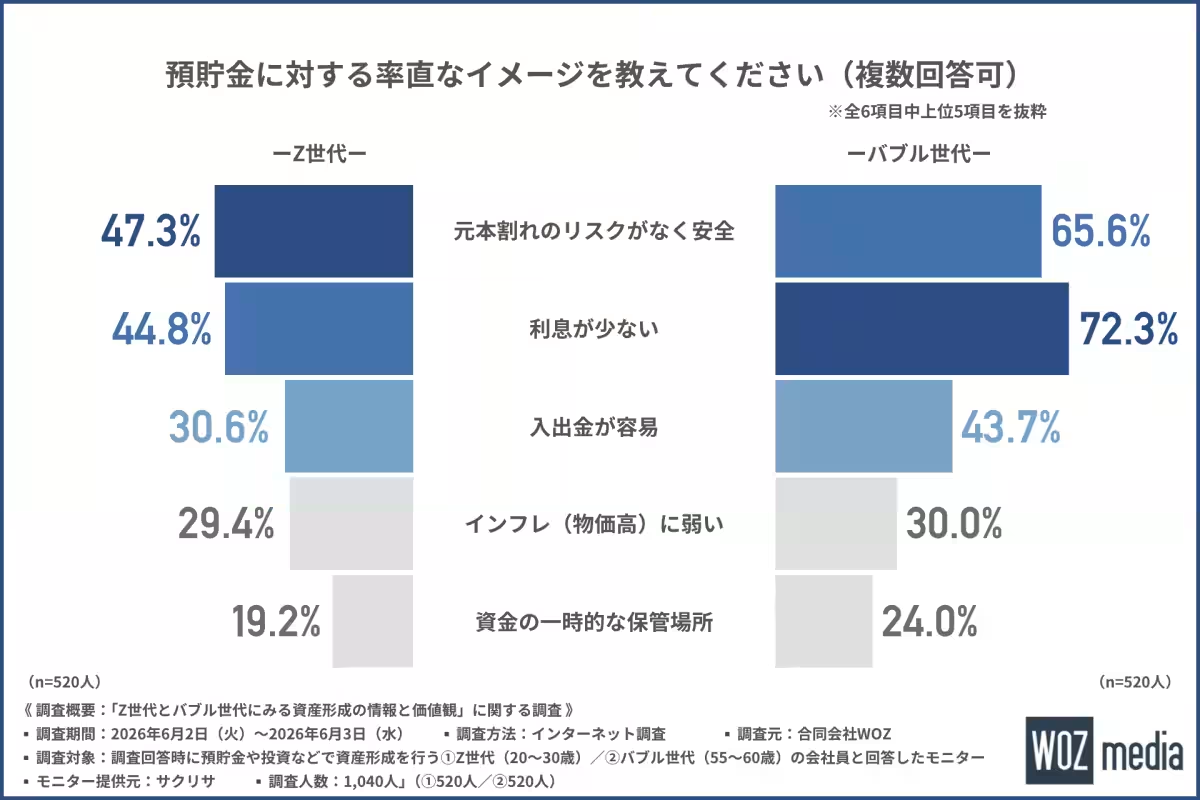

Perception of Savings Accounts

The outlook towards saving accounts further highlights different attitudes:

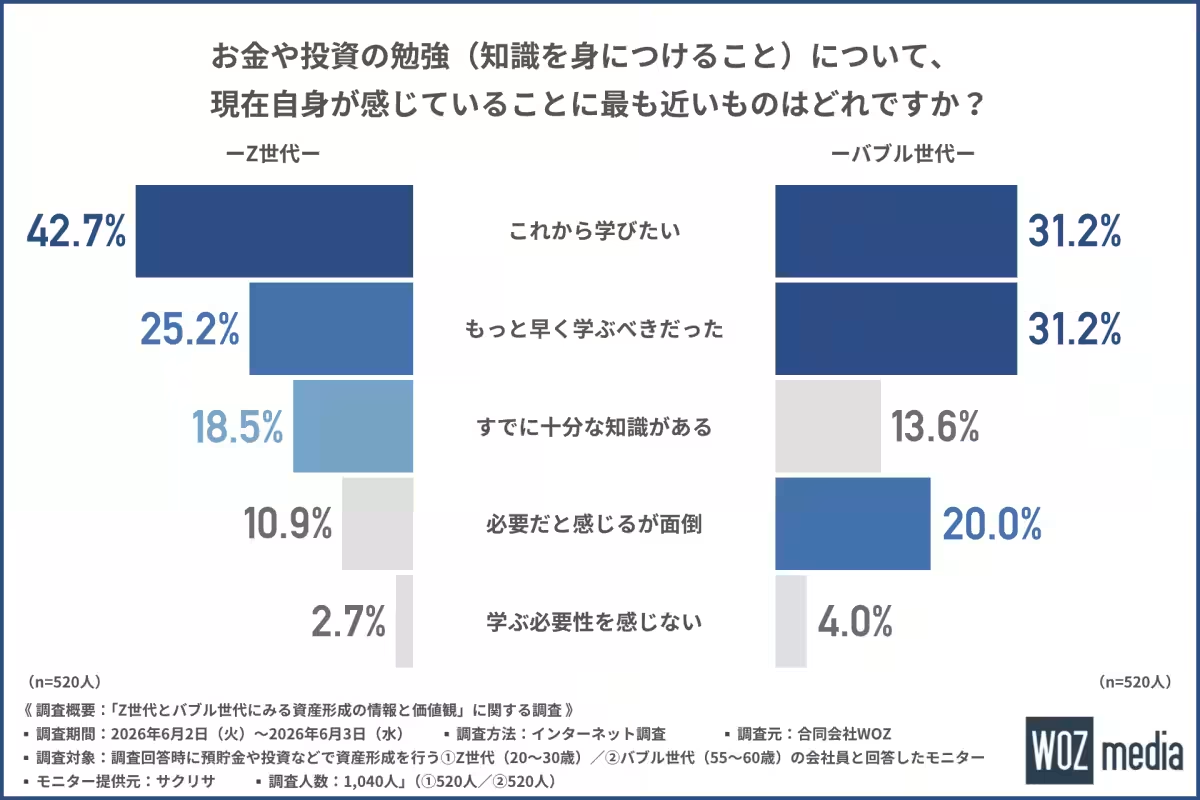

- - For Gen Z: 47.3% view savings as a safe option with no risk of losing principal, while 44.8% express concerns about minimal interest rates.

- - Bubble Generation: 72.3% acknowledge low-interest rates as a disadvantage, whereas 65.6% also find the principal protection an appealing factor.

The responses indicate a divergence in attitudes towards savings; Gen Z appears more optimistic about savings as a safe haven, whereas the Bubble Generation seems more discontented with the return on their savings, showcasing a generational disconnect regarding bank finances.

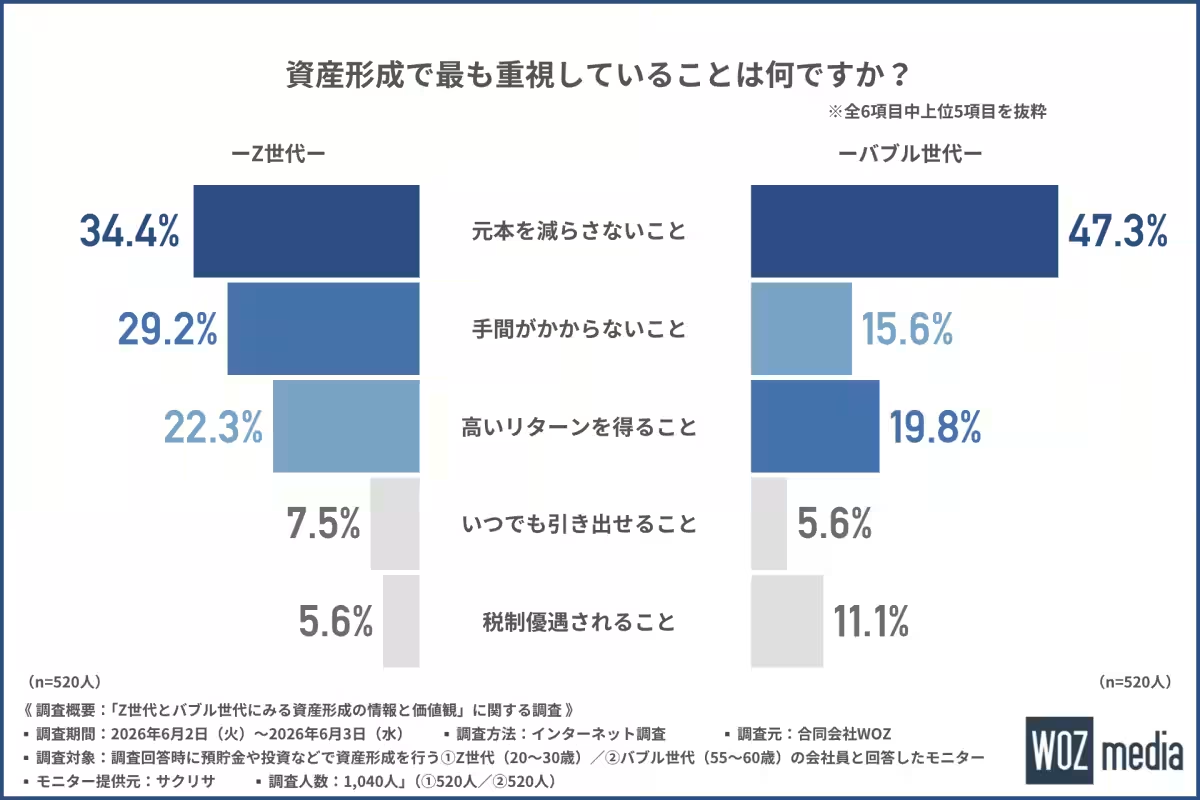

Priorities in Asset Formation

Both groups prioritize not losing the principal in their investments, yet their next priorities diverge significantly. Gen Z highlights the importance of ease and convenience in investment processes, while the Bubble Generation prioritizes high returns. This distinction implies that Gen Z is more inclined to seek simple and straightforward financial products compared to their predecessors who appear geared towards maximizing their investment returns.

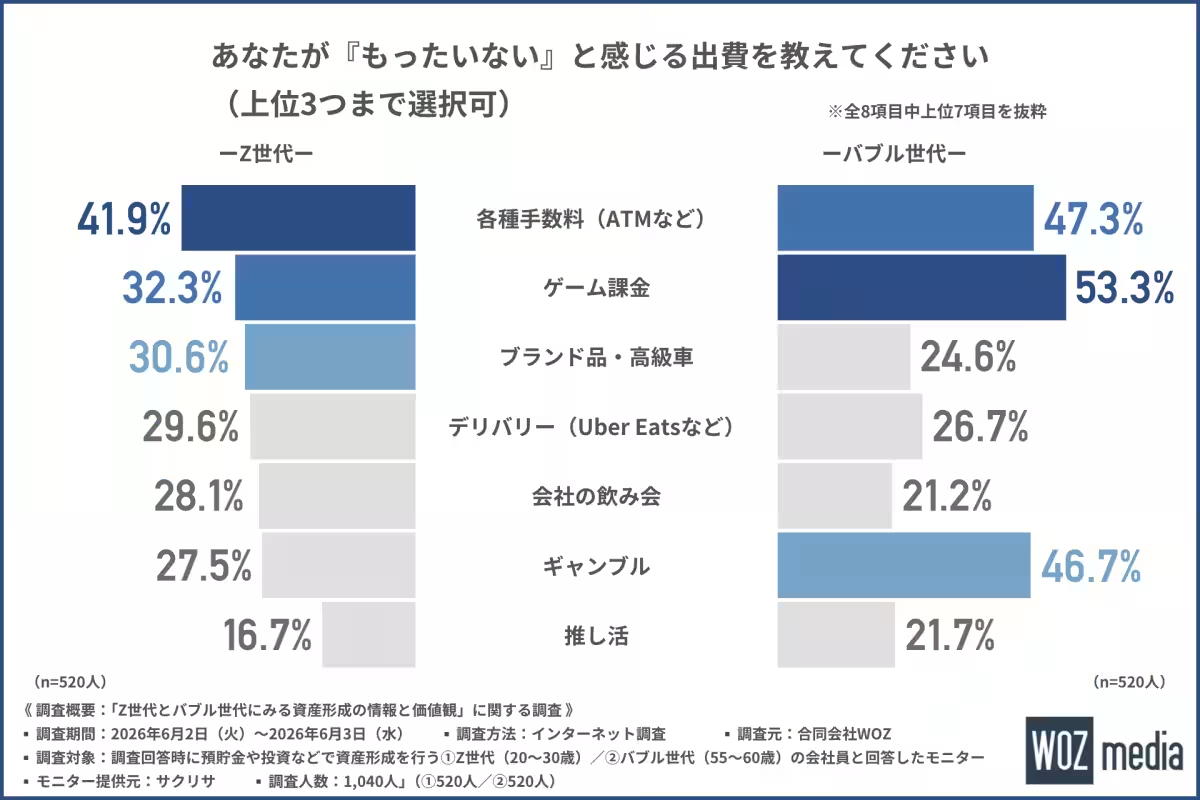

Wastefulness in Spending

A fascinating aspect of this survey was investigating perceptions of wasteful spending. Gen Z reported excessive fees (41.9%) and in-game purchases (32.3%) as wasteful, reflecting their cautious approach to daily expenditures. Conversely, the Bubble Generation noted game purchases as the top wasteful spending category (53.3%), which may reflect a cultural gap regarding online spending habits.

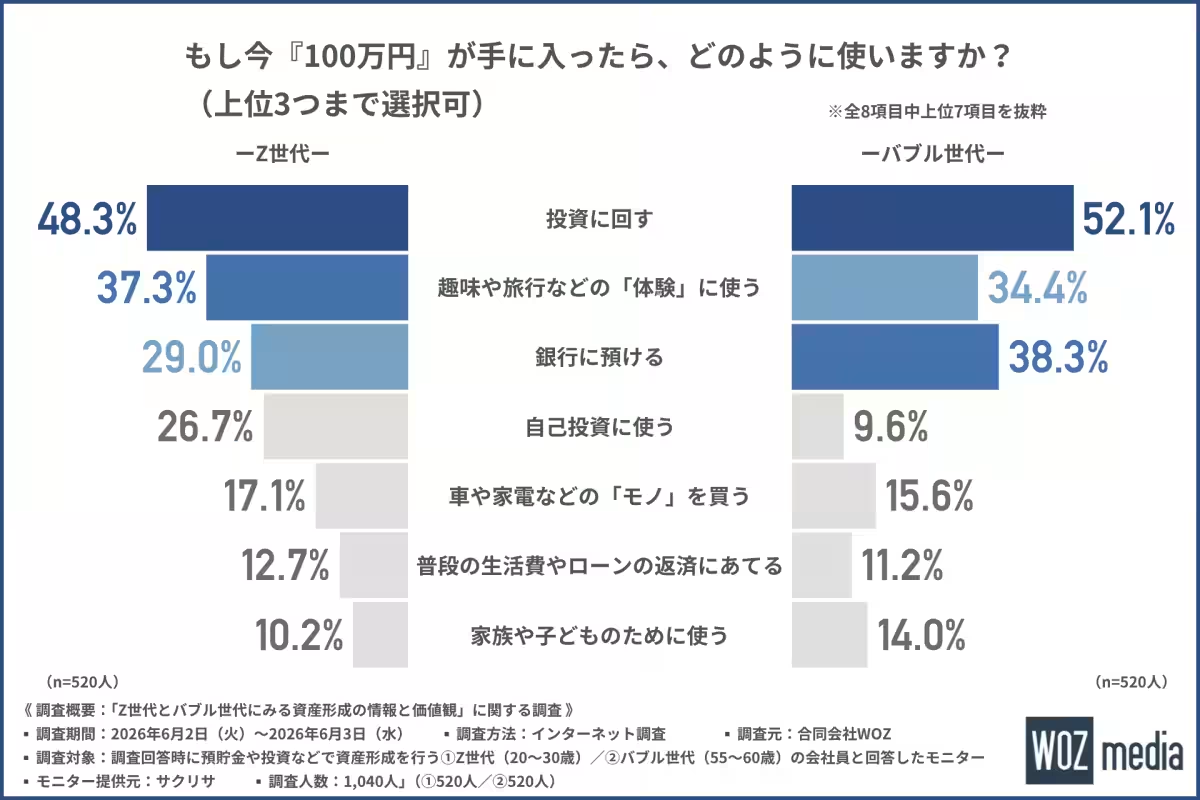

When posed with the hypothetical of receiving $1 million, both generations overwhelmingly indicated they would allocate the money towards investment, with 48.3% of Gen Z preferring to invest, while the Bubble Generation (52.1%) also leaned toward investing but showed a stronger inclination to just deposit it in the bank (38.3%).

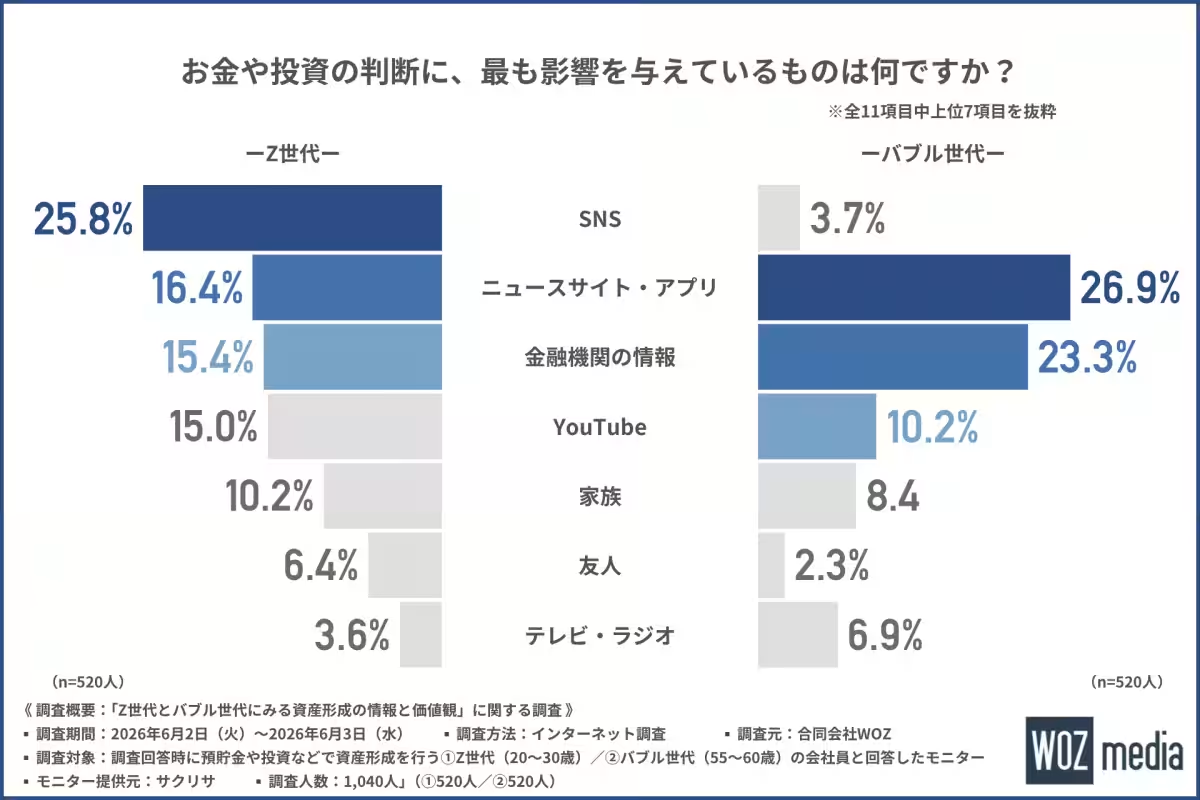

Sources of Financial Information

When it comes to financial decision-making resources:

- - Gen Z relies heavily on social media platforms such as Instagram and TikTok (25.8%), whereas the Bubble Generation favors news sites and apps, underscoring a stark difference in their approaches to gathering financial information.

- - Both generations recognize the value of credible information sources, with Gen Z showing flexibility in combining social media insights with traditional financial information sources.

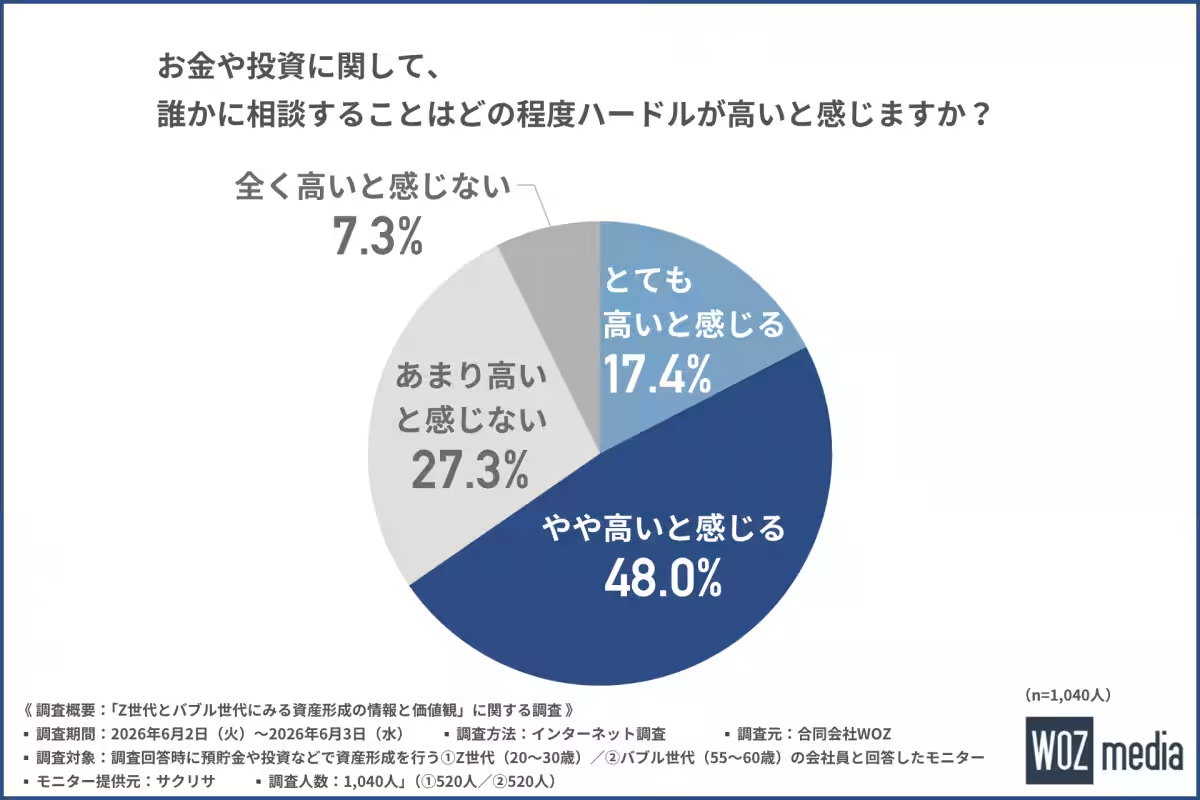

Despite this, nearly 70% of respondents from both generations expressed a high barrier to discussing finances with others, indicating a general discomfort with financial topics in social settings.

Conclusion

The WOZ study highlights a captivating juxtaposition in financial behaviors and perceptions between the generations. While both have a common ground in prioritizing savings and investment, their methods, information channels, and attitudes reveal a broader generational shift concerning finances and investment strategies.

In navigating financial discussions, overcoming barriers to communication and fostering educational opportunities will be essential for enhancing financial literacy, particularly between these two divergent groups. WOZ’s commitment to providing resources through its financial media platform aims to support individuals in understanding and optimally utilizing their financial options.

For more insight into financial trends and educational resources, visit WOZmedia.

Topics Business Technology)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.