Understanding Japanese Money Mindsets: Insights from the Money Habit Diagnosis

Insights from the Money Habit Diagnosis

In August 2025, Wealth Mind Approach conducted a comprehensive survey known as the Money Habit Diagnosis. This study involved 505 individuals aged between their 20s and 60s, aimed at uncovering prevailing money mindsets among Japanese people. By applying principles from psychology and neuroscience, the findings provide valuable insights into financial behaviors and could potentially guide households in budgeting and financial education.

Purpose of the Money Habit Diagnosis

The Money Habit Diagnosis serves as a friendly assessment tool that helps individuals understand their financial tendencies. It categorizes responses into five types: “Overly Cautious,” “Overspenders,” “Too Scared,” “Hiders,” and “Givers.” This classification is designed to provide tailored advice based on behavioral economics and financial therapy principles.

Survey Overview

- - Survey Title: Money Habit Diagnosis Monitor Survey

- - Survey Period: March 15, 2025 - July 17, 2025

- - Participants: 505 individuals across various ages and genders

- - Sample Method: Conducted by Wealth Mind Approach using the self-administered survey tool, Freeasy.

Key Findings

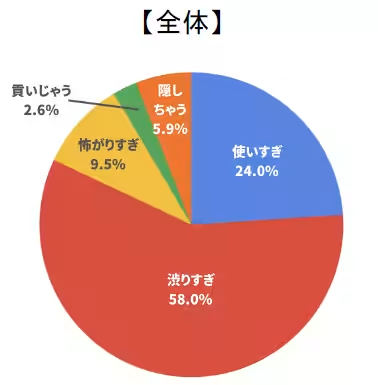

The survey results highlighted that 58.0% of participants fall into the “Overly Cautious” category. These individuals tend to prioritize savings and often hesitate when it comes to spending. This cautious mindset can be linked to Japan's cultural belief that emphasizes thriftiness as a virtue, alongside growing concerns about economic risks.

The rise in living costs and uncertainties surrounding social security has likely contributed to this tendency to minimize expenditures. In contrast, the minority categories of “Overspenders,” “Hiders,” and “Givers” reflect deeper emotional and relational influences on money management, highlighting diverse perspectives that individuals hold about finances.

Characteristics of a Reluctant Investor

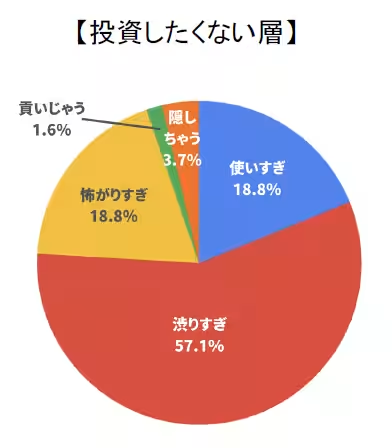

Approximately 38.8% of respondents expressed they have no desire to invest. Among these, 18.8% belonged to the “Too Scared” type, while 57.1% were categorized as “Overly Cautious.” This data suggests a notable psychological hesitance towards investment due to fears regarding market volatility and potential losses.

Conversely, among those who are currently investing, there appears to be a decrease in the “Overly Cautious” classification, indicating increased financial flexibility and risk tolerance among experienced investors. Therefore, delivering not only financial education but also emotional support to first-time investors becomes imperative.

Gender-Based Patterns

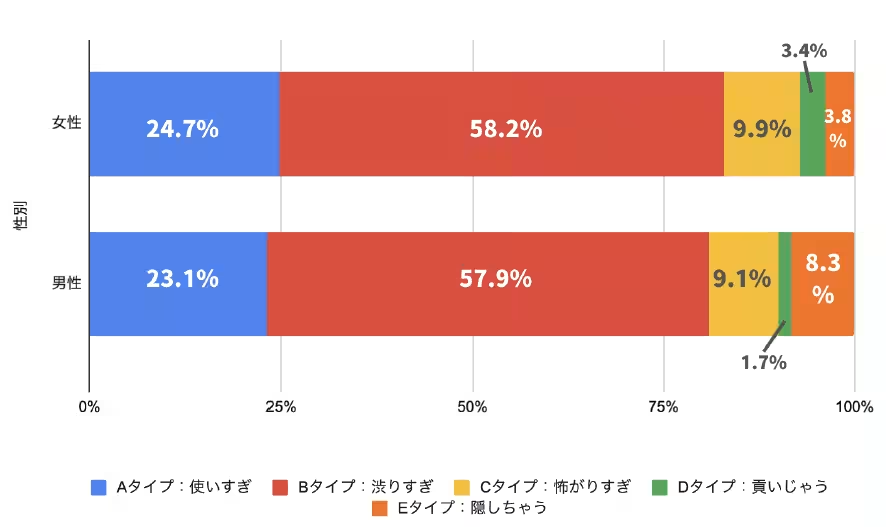

Both genders predominantly fall into the “Overly Cautious” category, but more women identify as “Overspenders.” This behavior may stem from emotional purchasing habits influenced by social media followings and community activities. Men, on the other hand, tend to exhibit a higher percentage of the “Hiders” category, likely linked to societal responsibilities and personal freedom dynamics.

Understanding these gender-specific trends is crucial for tailoring financial education approaches. Open communication about money for males and emotionally considerate spending strategies for females are suggested to enhance financial engagement and literacy.

Trends Across Age and Occupation

Age-wise, the tendency to be “Overly Cautious” rises with age, peaking among seniors aged 60 and above, where nearly 70% identify as such. Younger respondents (20s-30s) show higher rates of “Overspending” and “Hiding,” while middle-aged individuals in their 40s-50s increasingly exhibit caution as they face financial responsibilities.

Occupationally, while “Overly Cautious” remains dominant across fields, stay-at-home parents showcase a notably higher rate of the “Too Scared” category, indicating economic dependency and pressure regarding future financial stability.

Conclusion

The Money Habit Diagnosis reveals the critical importance of understanding financial psychology among Japanese citizens. As our findings indicate, various approaches may need to be implemented for effective financial education that considers emotional, cultural, and individual contexts.

For the complete investigation and findings, please visit Wealth Mind Approach's official website (contact page here). Citing this study requires referencing the URL and acknowledging the research conducted by Wealth Mind Approach led by Chikako Uehara.

Topics Business Technology)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.