The Limits of Auditing: How AI Can Deter Corporate Fraud

The Rise of Corporate Fraud and the Role of AI

In recent years, there has been a sharp increase in corporate accounting fraud. According to the latest report released by the Japanese Institute of Certified Public Accountants, 56 listed companies disclosed accounting fraud in the fiscal year ending in March 2025—more than double the number from five years ago. Alarmingly, there have been multiple cases where fraudulent activities went unnoticed for years, despite audits yielding clean opinions from audit firms. This raises critical questions regarding the fundamental limits of traditional auditing methods.

A New Perspective on Fraud Prevention

Kenji Uba, CEO of Júriō Inc. and a certified public accountant with an engineering background, has long argued that merely detecting fraud is insufficient. Instead, he believes a deterrent mechanism is necessary to prevent dishonest activities from occurring in the first place. Traditional auditing often relies on a sample testing method, where auditors extract significant transactions for verification. In contrast, Uba suggests that by applying AI technology to examine complete datasets, executing fraud would become unappealing due to the increased likelihood of detection.

By heightening the barriers to committing fraud rather than merely identifying it after the fact, his approach has become a cornerstone of Júriō Inc.'s technology development.

The company has recently developed a technological foundation embodying this philosophy and completed three patent applications. Ongoing verification tests are being conducted, especially within internal audit and investment sectors of major corporations, with promising results noted by participating stakeholders. The patented technologies leverage large language models combined with unique algorithms, allowing multi-faceted detection of corporate fraud from three perspectives—documents, explanations, and relationships.

Shifting from Detection to Prevention

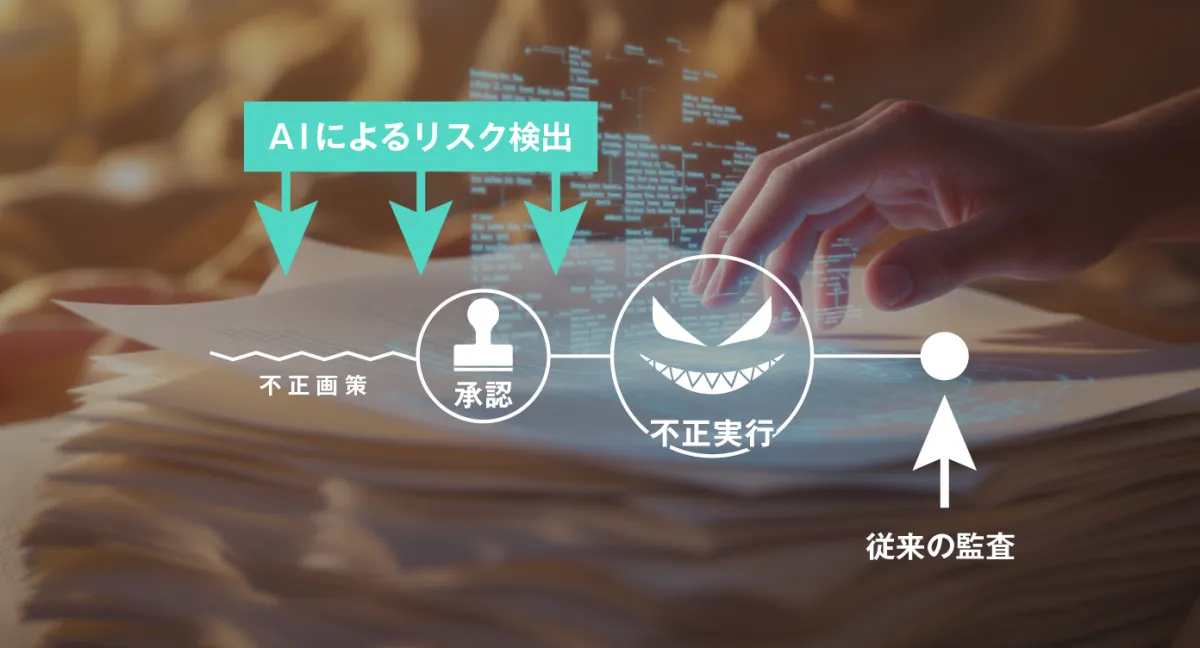

Traditional auditing adopts a reactive approach, discovering fraud only after it has been executed. Limited time and resources force auditors to select significant transactions to check. However, cleverly executed fraud often hides within transactions that have been overlooked.

This new technology supports auditors by analyzing vast amounts of internal data, including requests, contracts, and expense reports, and identifying possibly overlooked anomalies. With AI helping auditors focus on high-risk areas highlighted by its analysis, overall audit quality can improve even with limited resources.

Moreover, the technology can strengthen existing approval processes by pointing out inconsistencies before a request is approved, preventing inappropriate transactions from occurring. Importantly, AI does not replace human judgment but enhances decision-making capabilities.

The Importance of Deterrence

Even the best auditing can only detect fraud after it happens. By the time fraud is discovered, funds may have already been lost, trust undermined, and stock prices plummeted—making timely detection often too late.

The goal of this technology is to prevent fraud from occurring altogether. By instilling a strong sense of risk of detection in potential fraudsters, the technology aims to make them feel that complete disguise is impossible, thus deterring wrongdoing. This proactive approach serves as a psychological deterrent against fraud.

Three Innovative Technologies Leading Deterrence

The desired deterrent effect of the technology is achieved through a two-tiered structure. First, AI applies 'quantitative pressure' by monitoring all transactions and log data, which traditional sampling cannot achieve. Secondly, it analyzes 'qualitative pressure', considering contextual information like descriptions from requests, email communications, and interpersonal relationships that conventional AI often overlooks.

The three newly patented technologies offer distinct methods of fraud detection, complicating any perfect alibi construction for potential fraudsters:

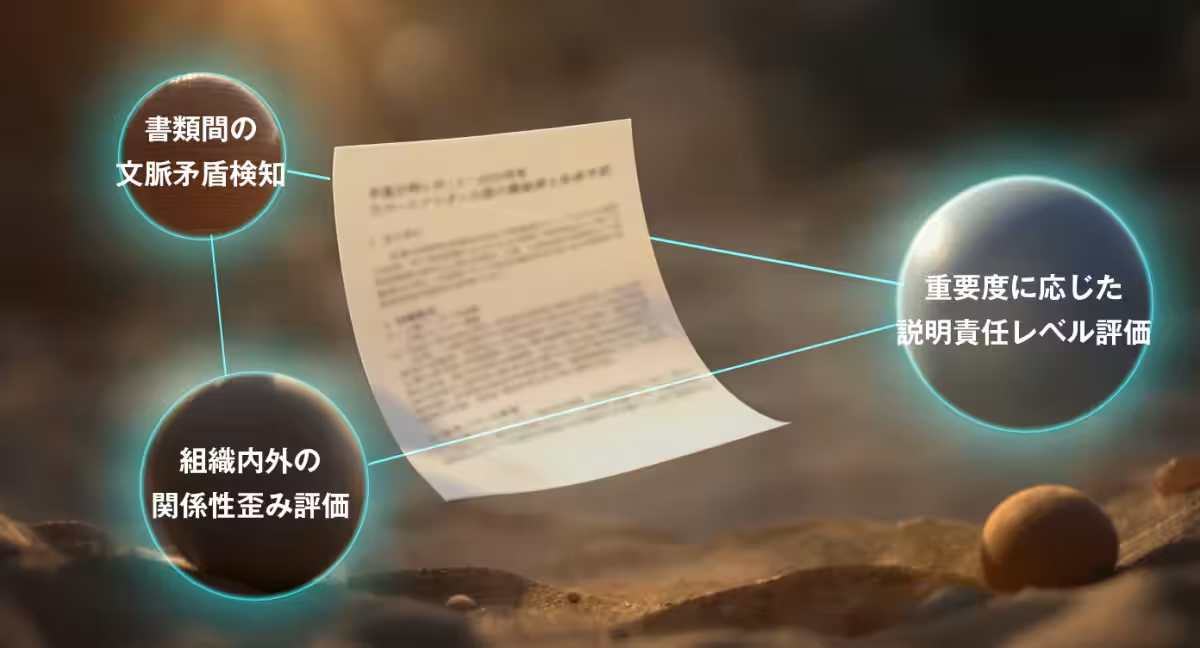

1. Automated Detection of Contextual Discrepancies: This technology cross-analyzes multiple data sources within an organization—such as requests, contracts, and expense reports—detecting semantic contradictions. For instance, if a travel report states a meeting was held in Tokyo while the system log indicates access from Osaka at the same time, it will flag this inconsistency.

2. Automatic Assessment of Accountability Levels: Automatically evaluates whether the level of explanation provided matches the investment’s significance. If a high-value contract is described merely as 'for a meeting', the system flags this as a potential anomaly, even suggesting improvements.

3. Multi-Dimensional Evaluation of Relation Distortions: This technology integrates various organizational data, such as HR, purchasing systems, and email, to create a visual representation of relationships between individuals, companies, and projects, allowing it to pinpoint unusual concentrations or irregularities in communications.

Verifying Application in Internal Audit and Financial Screening

Currently, testing is underway in internal auditing and investment screenings across multiple countries, including branches with physical separation from headquarters. This technology hopes to demonstrate the capability to detect anomalies early, overcoming traditional auditing challenges like language and cultural barriers.

Additionally, discussions are ongoing with financial institutions for potential applications in assessing corporate creditworthiness and analyzing fraud risk in investment opportunities.

The demand for such technology extends beyond internal auditing and finance. As companies undergo restructuring from active mergers and acquisitions or delegate significant authority to local branches during rapid growth phases, there is a pressing need to bolster internal oversight. Every industry faces the risk of corporate fraud, driving the necessity for enhanced auditing through AI technology.

Insights from Experience in Auditing

Kenji Uba reflects on his experiences while at Deloitte, where he noticed discrepancies in documents that seemed fine at first glance, only to later reveal instances of fraudulent activities. “After a thorough review of all data, subtle contradictions became evident,” he recalls. “While individual checks might not flag issues, looking at the overall picture often reveals telltale signs.” This realization underscored the urgent need for a layered detection system, provoking the thought: had such a system been implemented, would it have deterred the fraudsters, making them wary of detection?

Uba’s unique dual expertise in both technology and accounting positions Júriō Inc. as a pioneer in developing useful fraud detection systems, guiding organizations toward ethical practices.

For more information about Júriō Inc.’s services or partnerships, please visit Júriō Inc..

Topics Business Technology)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.