Analysis of Rental Trends for Small Retail Spaces Under 50 Tsubo in Japan for Late 2024

Overview of Rental Trends for Small Retail Spaces Under 50 Tsubo

In a recent analysis conducted by Athome Lab, commissioned by Athome, Inc., the rental trends for small retail spaces measuring less than 50 tsubo (approximately 165 square meters) have been evaluated for the latter half of 2024, particularly from October 2024 to March 2025. This report focuses on key urban areas in Japan, specifically Tokyo, Nagoya, and Osaka, and reveals significant shifts in rental prices and property availability.

Rental Trends in Tokyo

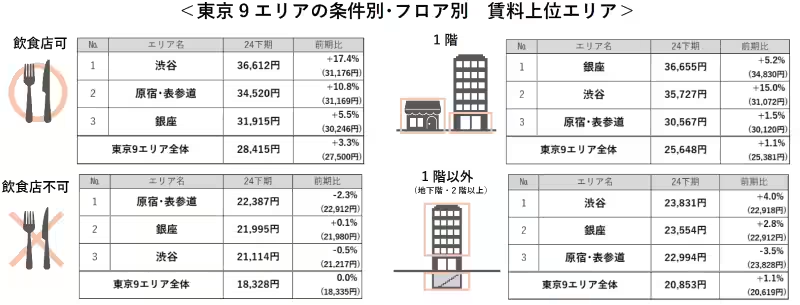

The rental prices for small retail spaces in nine areas of Tokyo have shown distinct trends. For properties that allow food and beverage businesses, the average rental cost has risen to ¥28,415 per tsubo, marking a notable increase of 3.3% compared to the previous period. In contrast, spaces that do not permit food and beverage operations remain stable at ¥18,328 per tsubo, reflecting no change.

This data demonstrates a substantial disparity between the two categories, with food and beverage permitting spaces costing an average of ¥10,087 more per tsubo, which translates to a 55% increase over the non-allowing counterparts.

Additionally, when comparing spaces by floor level, first-floor properties command an average rental price of ¥25,648 per tsubo, an increase of 1.1%, while properties on other floors are priced at ¥20,853 per tsubo, also showing a 1.1% gain. In this case, first-floor spaces are premium, exceeding the average rental price of the upper floors by ¥4,795, or 23%.

However, the overall count of available properties has seen a decline, dropping by 2.8% compared to the previous term. This marks the fifth consecutive period of decreasing availability, signaling a tightening market landscape for small retail spaces in Tokyo.

Insights for Nagoya and Osaka

In Nagoya, rental rates around Nagoya Station for food and beverage businesses and properties on the first floor have reached their highest levels since the first half of 2018, indicating a robust demand in this key area. Likewise, Osaka's Namba and Shinsaibashi regions have also set new precedents, with rental prices in every specified category and floor type hitting their peak since 2018. This trend showcases the vital role these locations play within their respective urban markets.

Research Methodology

The analysis targeted major areas in Tokyo—including Ginza, Shimbashi/Toranomon, Roppongi, Shibuya, Harajuku/Omotesando, Ebisu/Meguro/Nakameguro, Shinjuku, Ikebukuro, and Ueno/Asakusa—as well as central Nagoya and Osaka areas like Umeda and Namba/Shinsaibashi. The data was compiled from properties registered and publicly disclosed on the real estate information network specializing in rentals from 5 to 50 tsubo in size, focusing on properties located within a 10-minute walk of train stations.

The methodology encompassed the latest median rental prices, inclusive of common area fees and applicable taxes, ensuring accuracy in the figures presented. If multiple properties within the same building and floor were listed, only the most recent data point was utilized for analysis.

Properties were categorized into two segments: those allowing food services and those that do not, further classified by floor level into first floors and non-first floors (including underground and second floors or higher).

For a comprehensive analysis of the rental trends and detailed insights, the full report can be accessed via the following link: Download PDF.

Topics Consumer Products & Retail)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.