Uncertain Outlook for Used Car Purchase Prices Amid Strait Closures: March 2026 Report

March 2026 Used Car Purchase Price Report: Effects of the Hormuz Strait Closure

In the latest report by Fabrica Communications, a subsidiary of Fabrica Holdings, the used car purchase market shows a complex landscape influenced by geopolitical events. The closure of the Hormuz Strait is poised to expatriate substantial effects on both car exportation and domestic purchase prices, as detailed in this comprehensive assessment.

Overview of the Current Market

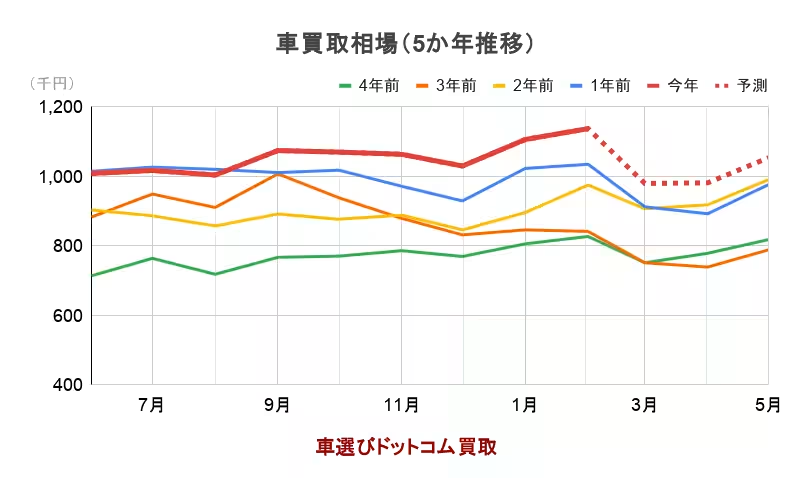

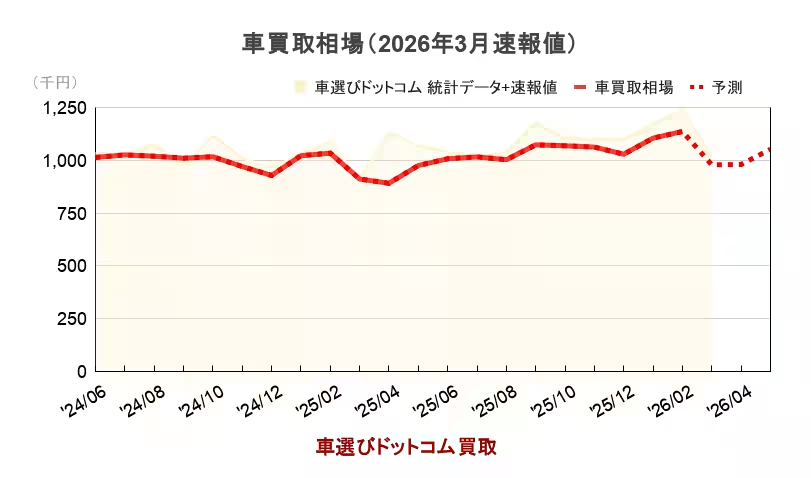

The February report noted that the purchase price for used cars reached a historical apex, driven primarily by the high demand for domestically manufactured vehicles aged 3 to 5 years. This upward trend was further fortified by Japan's used vehicle export activity, which saw a record high in 2025 of 1,708,604 units exported. However, the tension in the Strait of Hormuz has cast a shadow over future expectations, creating a more uncertain environment.

Immediate Consequences of the Hormuz Strait Closure

The United Arab Emirates (UAE), as Japan’s largest used car export destination, accounted for approximately 250,000 units exported in the previous year. Aside from being a primary destination, the UAE is a critical re-export hub to regions such as the Middle East, Africa, and Central Asia. Thus, the cessation of maritime transport due to the Hormuz Strait blockade is anticipated to disrupt about 20% of Japan's total used car exports.

The immediate fallout could see an influx of vehicles into domestic supply chains, leading to a drop in purchase prices. Used cars previously bound for export are now stagnating in ports and storage yards, heightening the associated holding costs. If this situation lingers, it could result in unsold inventory compelling exporters to divert these units to domestic auctions or markets—further destabilizing local supply and demand.

Potential Scenarios

As per analyses mentioned by CNN, which highlighted a potential blockade lasting between one to six months, the implications for used car purchase prices could vary:

- - Short-Term Blockade (1-2 months): Expect temporary disruptions with potential recovery as supply routes normalize and summer demand rebounds. While there might be a short-term increase in supply decreasing purchase prices, the longer-term outlook remains stable as recovery prospects loom.

- - Long-Term Blockade (up to 6 months): Continued oversupply could establish an extended downward pressure on prices. The saturation in the domestic market could keep values under persistent strain, particularly impacting high-demand vehicles like the Toyota Land Cruiser, popular in Middle Eastern markets.

Trends in the Used Car Market

In terms of pricing trends, the average purchase price data from Toyota shows a significant elevation, exceeding 1.1 million yen, reflecting peak historical price levels. However, projections indicate a decline for March, predicting an average below 1 million yen. Nevertheless, as trends suggest, there may be potential for price stabilization and even appreciation as consumer demand typically increases during the summer months.

The demand for domestic vehicles manufactured over the last three to five years continues to support elevated purchase prices. Simultaneously, older vehicles exceeding ten years of manufacture are seeing a rise in demand in emerging markets, enhancing their value within that segment. However, prices for these older models remain relatively modest and won't substantially influence overall market averages.

Insights into Purchase Price Rankings

Fabrica Communications has issued an update on the body style-specific rankings of used car purchase prices. For domestic vehicles, the leaderboard remains consistent but with some minor fluctuations:

1. Light Commercial Vehicles: 29.4% (up by 0.8%)

2. Minivans/One-box: 19.5% (down by 0.9%)

3. Compact/Hatchbacks: 16.3% (down by 1.3%)

4. Sedans/Hardtops: 7.6% (up by 0.6%)

5. SUVs/Crossovers: 7.1% (down by 0.3%)

On the import side, while the top three body types saw no change, their share in the overall market has increased:

1. SUVs/Crossovers: 25.9% (up by 3.0%)

2. Sedans/Hardtops: 24.3% (up by 2.5%)

3. Compact/Hatchbacks: 23.5% (up by 3.1%)

Conclusion

In the face of geopolitical uncertainties, the used car market remains dynamic, yet potentially volatile. As these trends continue to evolve with market drivers influenced by both demand and supply mechanics, observers and stakeholders are encouraged to monitor shifts carefully. Fabrica’s commitment to providing real-time data through their website, Kuruma Erabi, continues to serve as an essential resource for stakeholders navigating these turbulent market conditions.

Topics Consumer Products & Retail)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.