Survey Reveals Surprising Results About Card Loan Application Failures

Understanding the Realities of Card Loan Application Failures

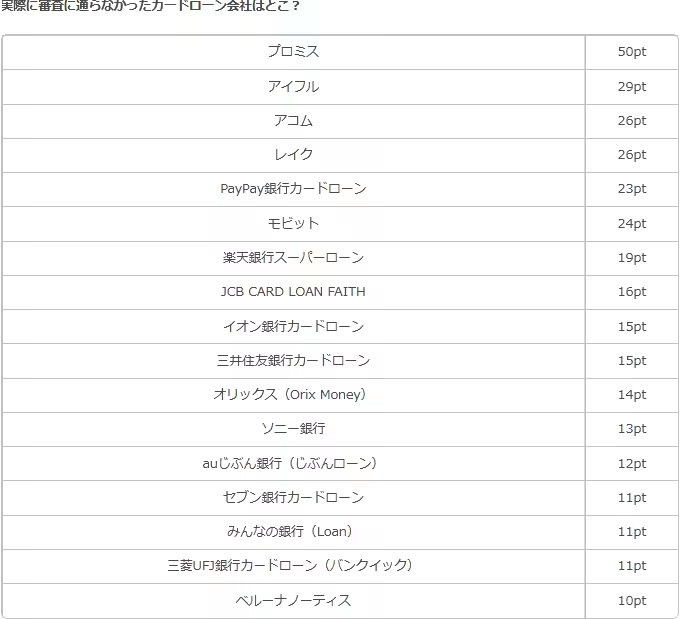

In recent months, Selectra Japan conducted a comprehensive survey among 779 individuals who have applied for card loans. The aim was to uncover insights about the application process, particularly focusing on the experiences of the 100 respondents who faced rejections. The study highlights the obscured criteria of card loan approvals, emphasizing how crucial consumer experiences are to understanding this financial aspect.

The Application Landscape

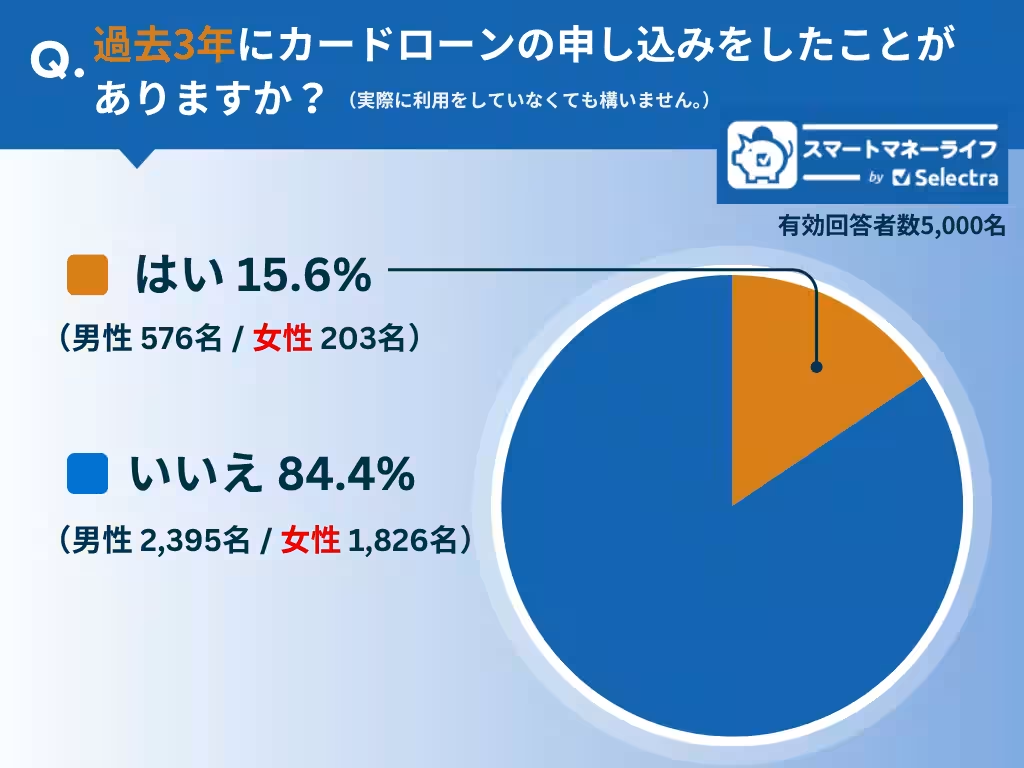

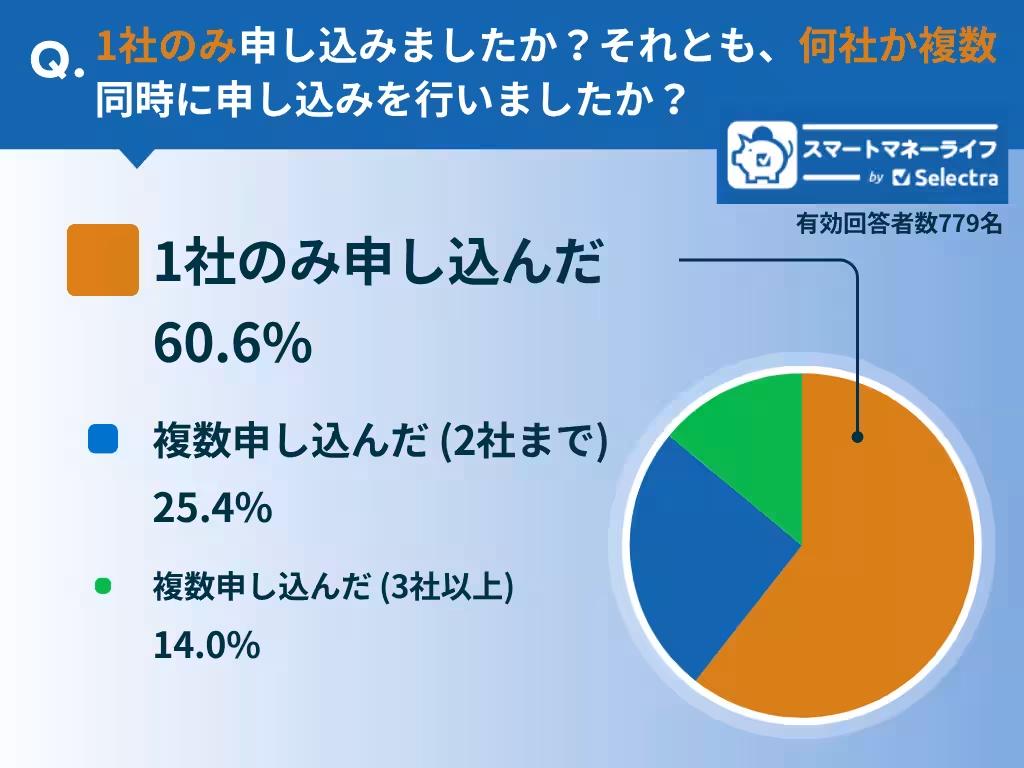

Approximately 15.6% of those surveyed—equivalent to 6 to 7 individuals out of every 100—have applied for card loans, signifying that such loans have become more common in Japan's financial landscape. When questioned about whether they applied to multiple lenders simultaneously, 60.6% opted for a single firm, while 25.4% applied to two lenders and 14% approached three or more.

Interestingly, the rejection rates provide a nuanced picture. While applying to multiple lenders can lower the chances of approval, it does not guarantee failure. The approval rates revealed a stark contrast: 88.1% of those who applied to one lender succeeded, while the success rates plumet to 77.8% for two lenders and 61.5% for three or more.

Unexpected Rejections

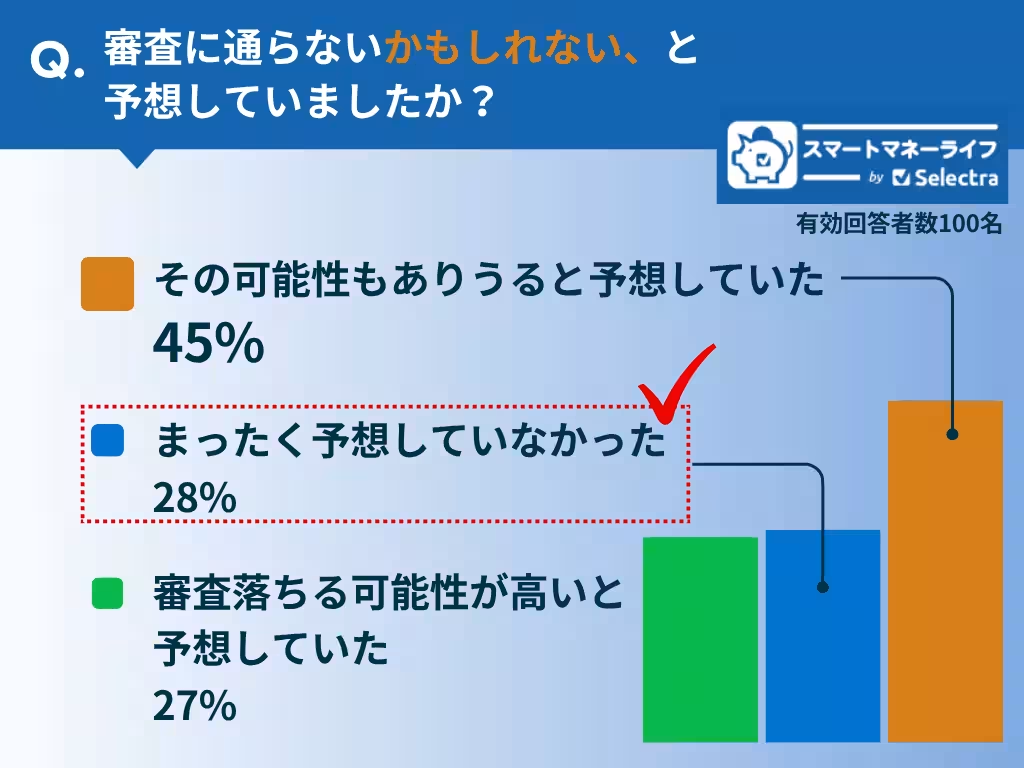

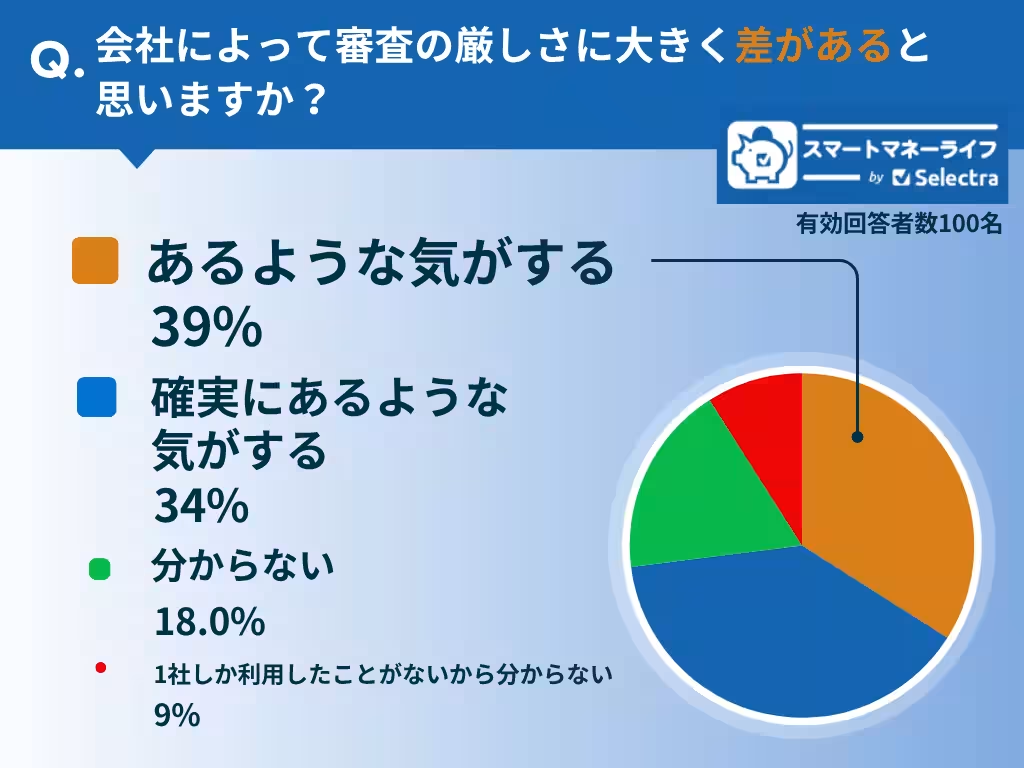

What stands out from this survey is the feeling of disbelief among those who were rejected. A significant portion did not foresee their application would fail. Specifically, 28 out of 100 rejected applicants had completely unexpected outcomes. When asked about their reasons for rejection, they speculated but received no clear answers, given that reasons for such failures are typically undisclosed by financial institutions.

Key Factors in Rejections

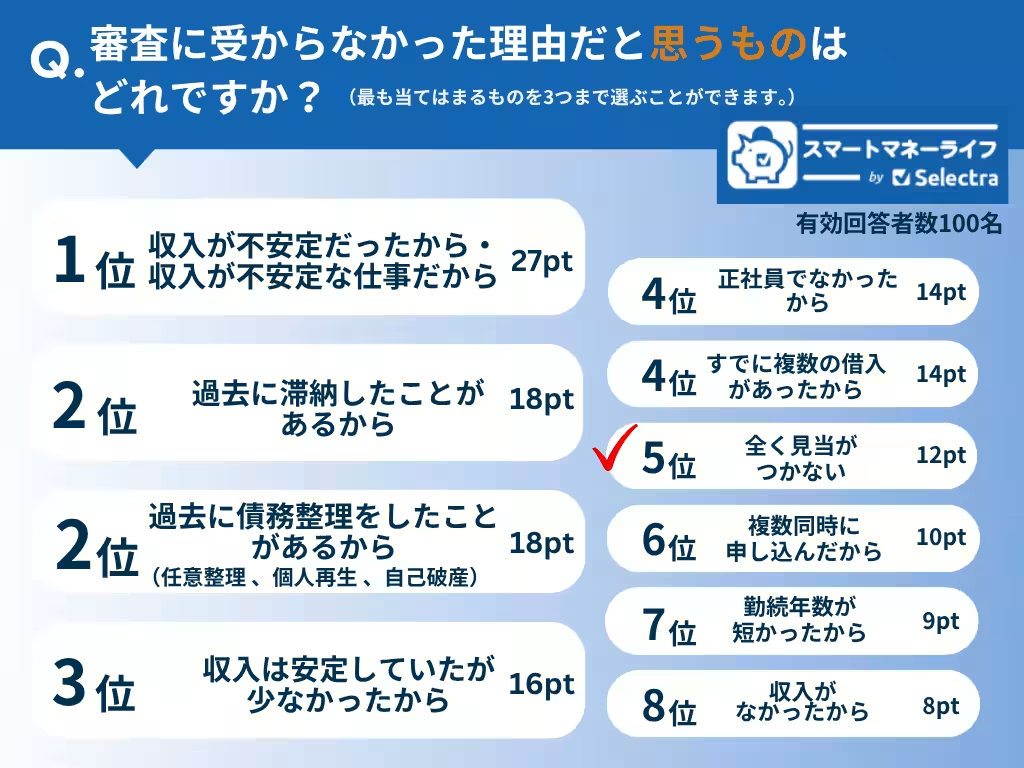

In attempting to understand why applicants might fail, several reasons were seen as major contributors:

1. Unstable Income: Even with a high income, lack of stability can lead to harsh evaluations during the approval process.

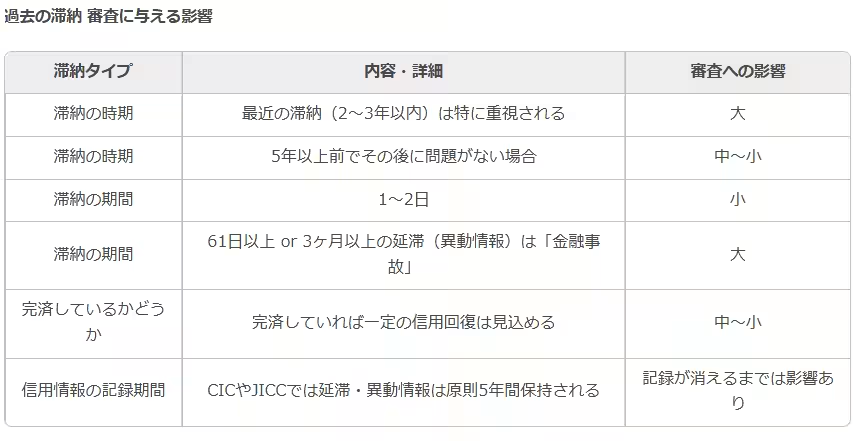

2. Past Defaults: Individuals with previous payment delays face greater hurdles during evaluations since financial institutions check personal credit histories meticulously.

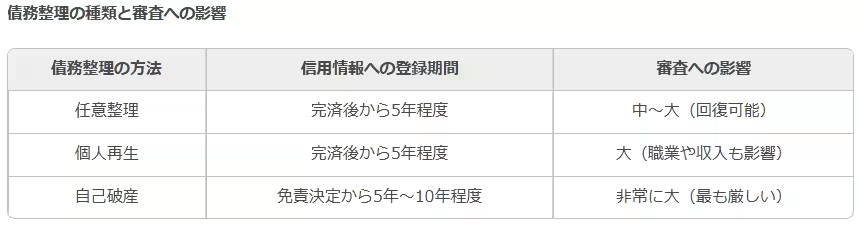

3. Debt Restructuring: Those who have undergone debt restructuring face significant struggles in securing loans.

Other reasons included inaccuracies in submitted information, which serve as red flags for lenders, leading to immediate disqualification.

Navigating Rejections

From the findings, it's clear that if applicants face rejection, they should take proactive steps. Checking for overdue payments through credit scoring agencies like CIC can help clear previous anomalies affecting one’s credit. Moreover, considering alternative loan companies can provide varied chances of approval.

Conclusion: The insights gathered from this survey reflect not only the intricate landscape of card loan applications but also serve to inform applicants about the critical factors influencing their acceptance rates. The importance of stable income and clear personal records cannot be overstated, as they significantly influence potential outcomes. This study by Selectra Japan underscores the necessity for potential borrowers to navigate these waters with caution and preparedness.

Topics Financial Services & Investing)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.