C&W Unveils Tokyo Office Market Report for Q4 2025 with Insights on Trends

Cushman & Wakefield's Tokyo Office Market Report for Q4 2025

Cushman & Wakefield (C&W), a global real estate services firm, has released its latest report on the office market in Tokyo for the fourth quarter of 2025. This detailed analysis sheds light on market dynamics, implications of upcoming supply, and the factors driving changes in rental rates.

Key Takeaways from the Report

The report outlines two primary trends expected to shape Tokyo's office market. First, a significant increase in rental prices is anticipated, driven by an influx of new supply concentrated in areas such as Kyobashi, Yaesu, and Nihonbashi. With rental agreements likely to be signed at levels exceeding the current market average, an upward momentum in existing building rents will likely persist.

Second, as inflation affects the broader economic landscape, landlords are expected to pass increased operational and capital expenses onto tenants. The report highlights how, since 2020, indices such as the domestic corporate goods price and core consumer price have surged significantly, impacting the operational costs faced by property owners. Meanwhile, tenant companies are experiencing notable increases in relocation costs due to rising expenses for interior construction and restoration work.

As a result, the Tokyo office rental market is transitioning from a recovery phase to one where price increases reflect broader economic inflation, indicating a more sustained upward trajectory.

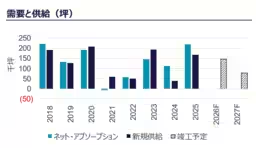

Supply and Demand Trends

The demand-supply balance for Grade A offices in Central Tokyo tightened significantly throughout the year owing to robust demand. The vacancy rate dipped below 1% for the first time in approximately five years, hitting 0.9% in Q3 2025, before closing the year at an unprecedented low of 0.5%. This trend has been driven by an increase in demand due to corporate expansions, consolidations, and relocations to higher-grade buildings.

The sectors driving this demand include Technology, Media, and Telecommunications (TMT), alongside manufacturing firms. Upcoming supply is projected to have a pre-leasing rate of 89.7%, demonstrating strong market confidence. While secondary vacancies might emerge, ongoing demand for in-building expansions and the lengthy duration of restoration work will likely keep vacancy levels low.

The critical shortage of office inventory has become prominently evident across the market, exacerbating competition among tenants.

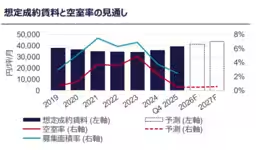

In Q4 2025, the average anticipated contract rent is expected to reach 39,270 yen/month per tsubo, surpassing the pre-pandemic peak of 38,258 yen observed in Q3 2019, when the vacancy rate was 0.5%. This signals an 8.2% year-on-year increase, underscoring the market's recovery trajectory post-pandemic.

Conclusion

C&W's report not only provides insights into present conditions but also presents implications for the future of the Tokyo office market. With ongoing economic factors shaping tenant behavior and landlord strategies, stakeholders in the real estate sector are advised to stay alert to the evolving landscape as challenges and opportunities arise.

For further details, the full report is available for download, offering a wealth of insights into the Tokyo office market's current state and trends.

For those interested in learning more about Cushman & Wakefield, the company has established itself as a leading player in the global commercial real estate market, listed on the New York Stock Exchange. With over 52,000 employees operating in around 400 locations across approximately 60 countries, C&W offers a diverse array of services including facilities management, brokerage, valuation, tenant representation, leasing, and project management.

To delve deeper, visit Cushman & Wakefield's official website.

Topics Business Technology)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.