Insights from Kokomora's Survey on Housing Loans and Consumer Preferences

Insights from Kokomora's Survey on Housing Loans

Kokomora recently executed an extensive survey to understand consumer preferences and behaviors regarding housing loans. The survey captured data from 200 participants, all of whom had prior experience with housing loans. Here’s a closer examination of the results and what they reveal about the housing loan landscape in Japan.

Loan Duration Preferences

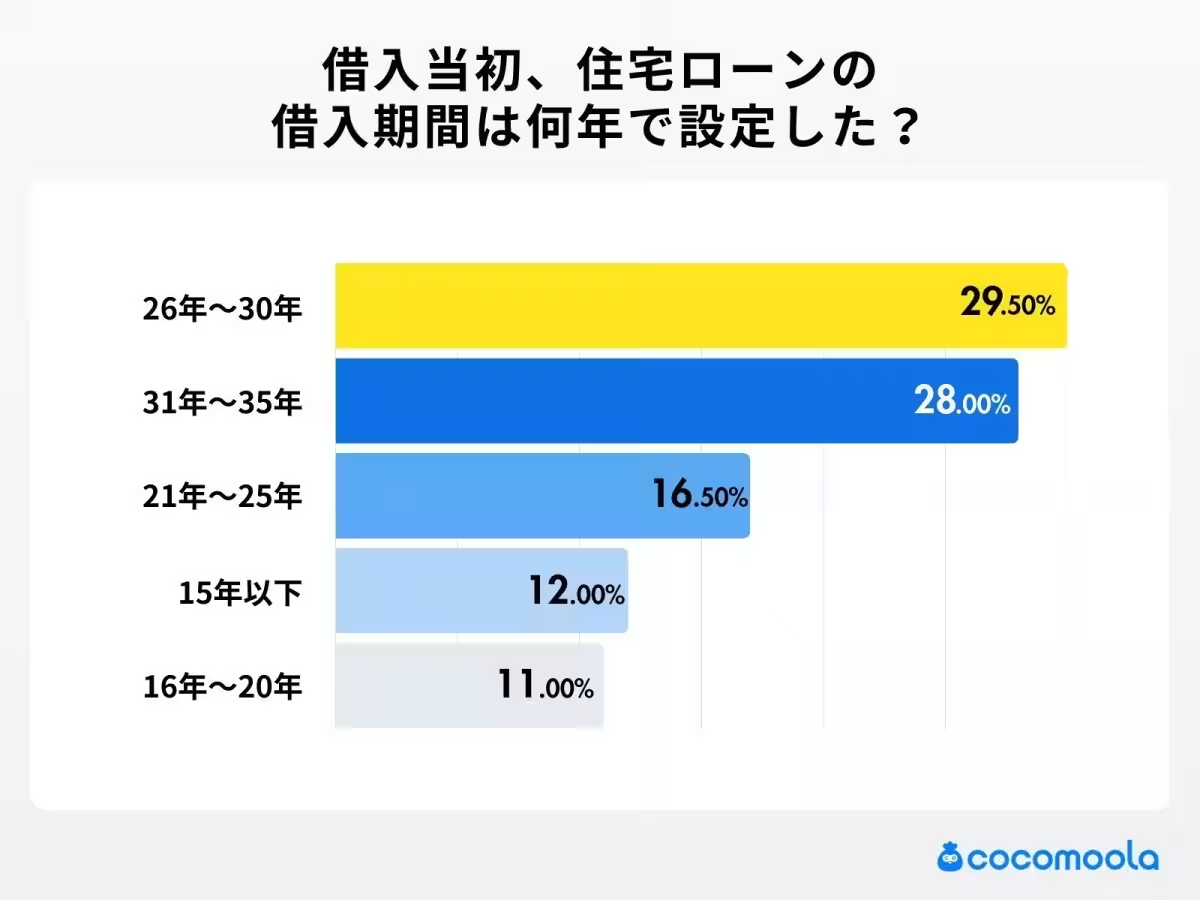

One of the standout findings from the survey indicated that a substantial majority of borrowers opt for loan terms between 26 and 35 years, accounting for an impressive 57.5% of respondents. This preference for longer loan durations suggests a trend towards manageable monthly payments, aligning with stable financial planning. A breakdown of the loan terms revealed:

- - 26 - 30 years: 29.5%

- - 31 - 35 years: 28.0%

- - 21 - 25 years: 16.5%

- - 15 years and below: 12.0%

- - 16 - 20 years: 11.0%

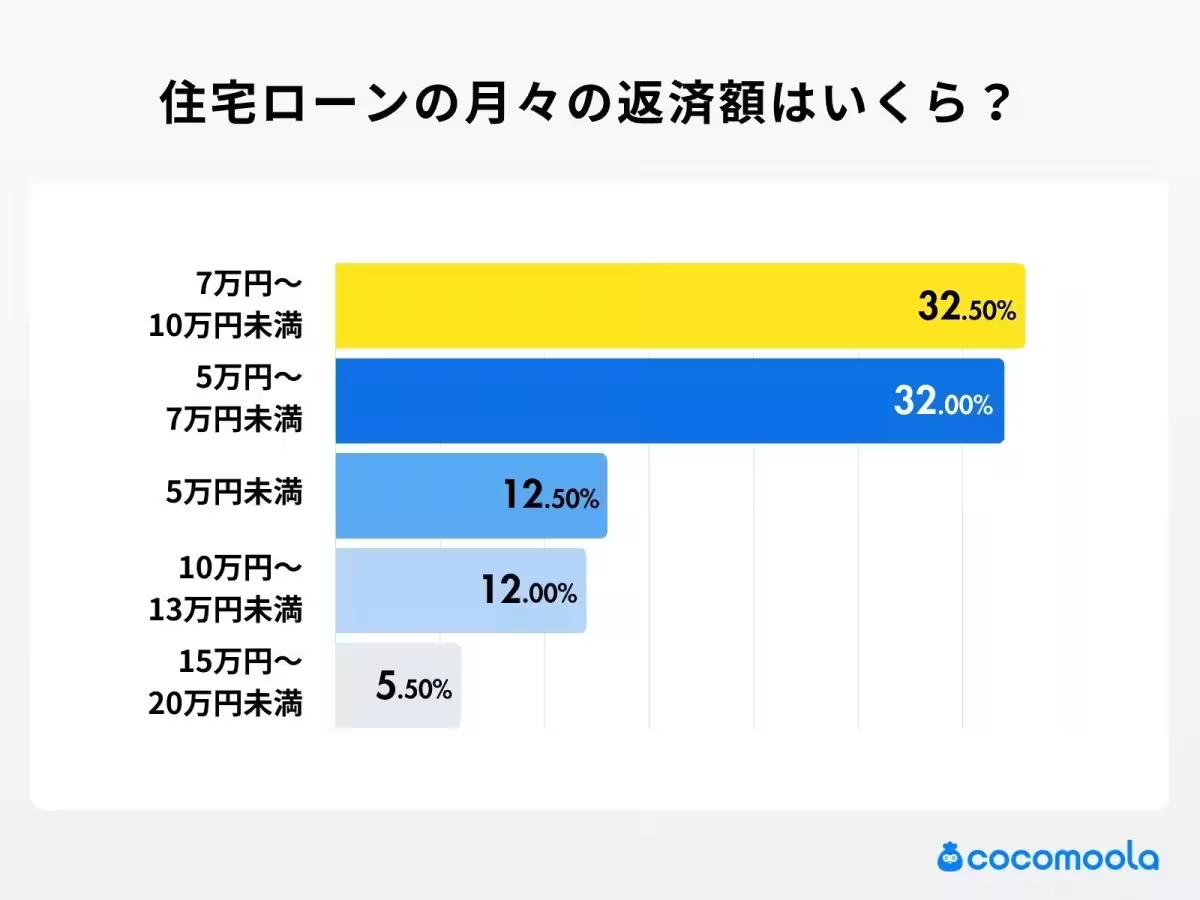

The indication that many borrowers prefer longer repayment periods aligns with the findings around monthly repayment amounts. Over 64.5% of participants reported monthly repayments between 50,000 and 100,000 yen, demonstrating a common strategy to afford payments without financial strain.

Attitudes Towards Bonuses and Stable Payments

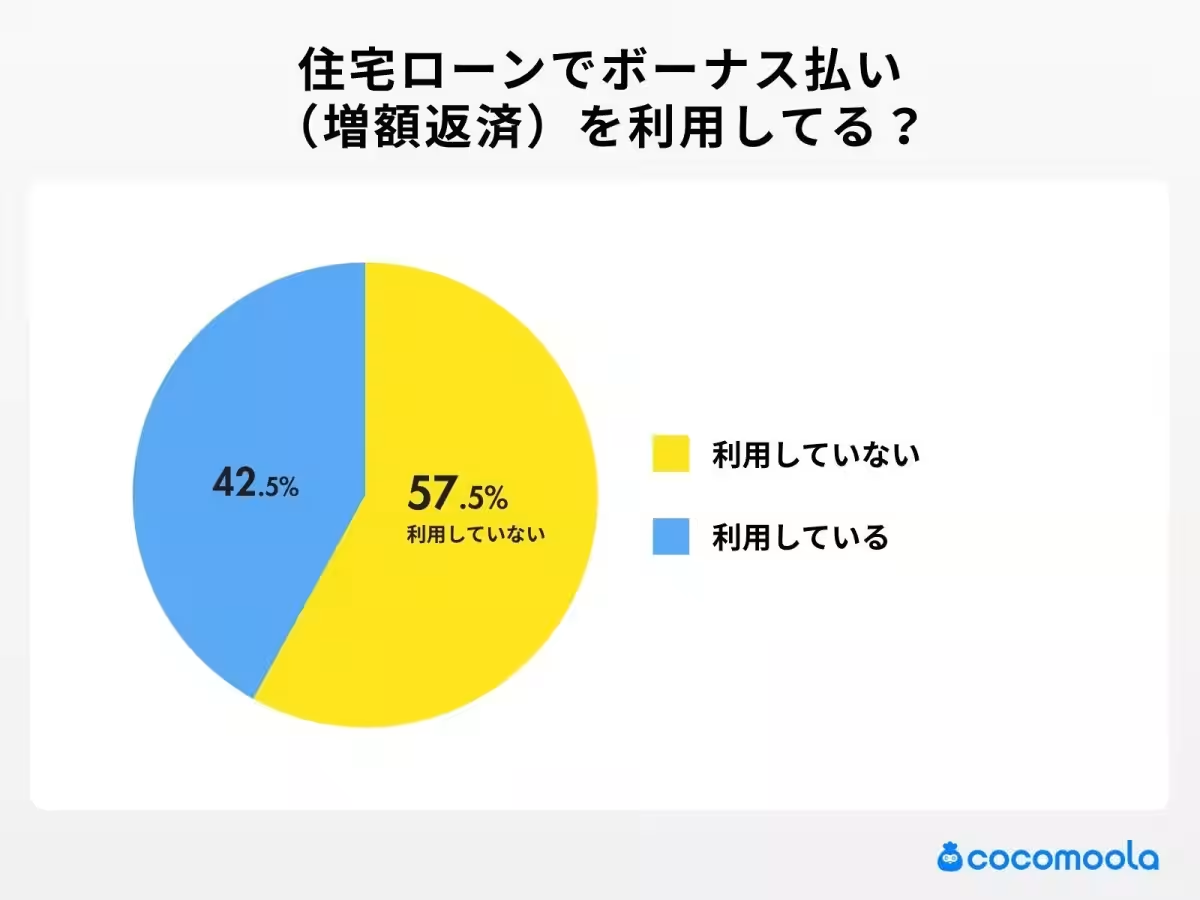

Interestingly, a significant 57.5% of the respondents indicated they do not utilize bonus payments for loan repayments. This indicates a growing emphasis on regular, predictable payment schedules rather than depending on variable bonuses, which can be subjected to uncertainty. This tendency reflects a broader desire for financial stability among borrowers.

Key Factors in Loan Selection

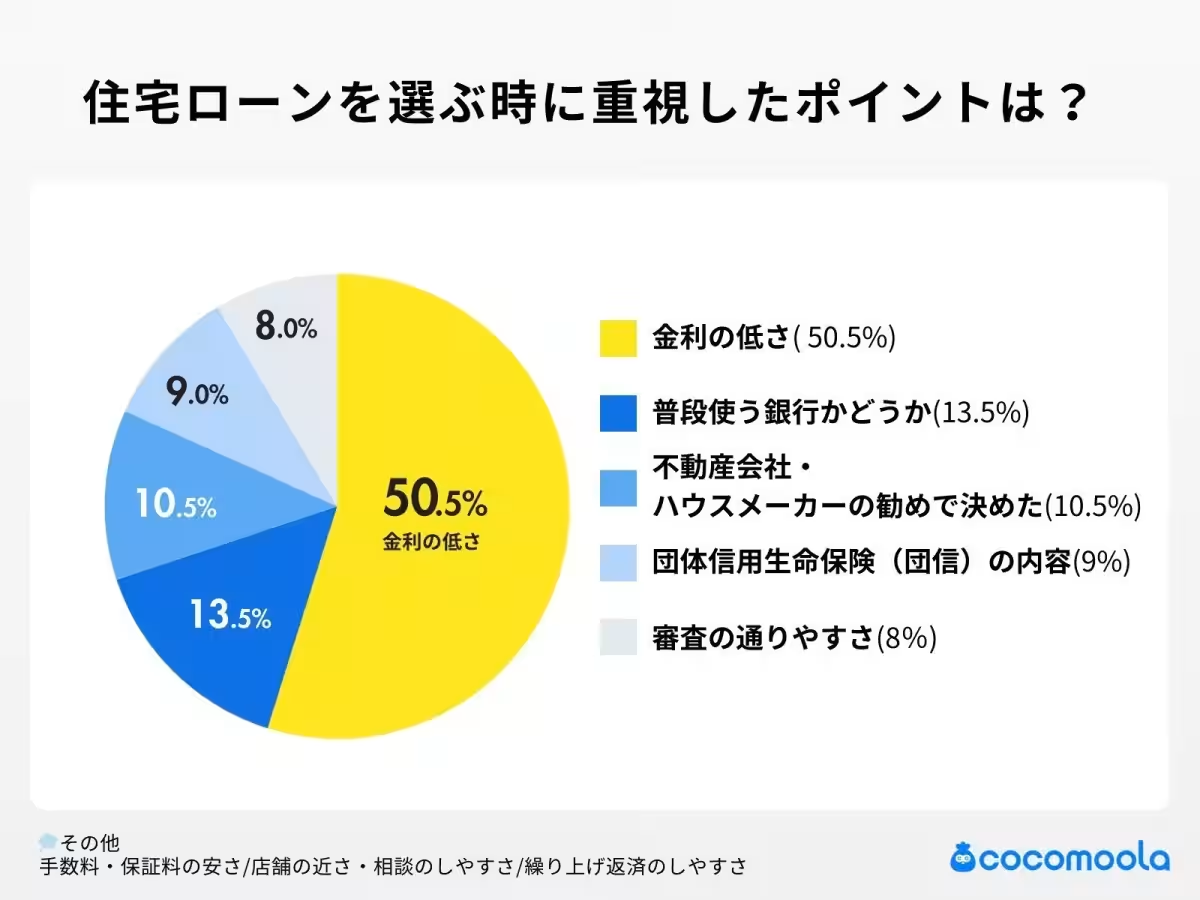

When selecting a housing loan, the most critical factor influencing decisions was the interest rate, with 50.5% of respondents prioritizing low rates over other considerations. Following interest rates, the main bank being familiar was important for 13.5%, with recommendations from real estate agents or construction firms following at 10.5%. This highlights that while some borrowers are looking for the best deals, others prefer the comfort of familiarity in their financial partnerships.

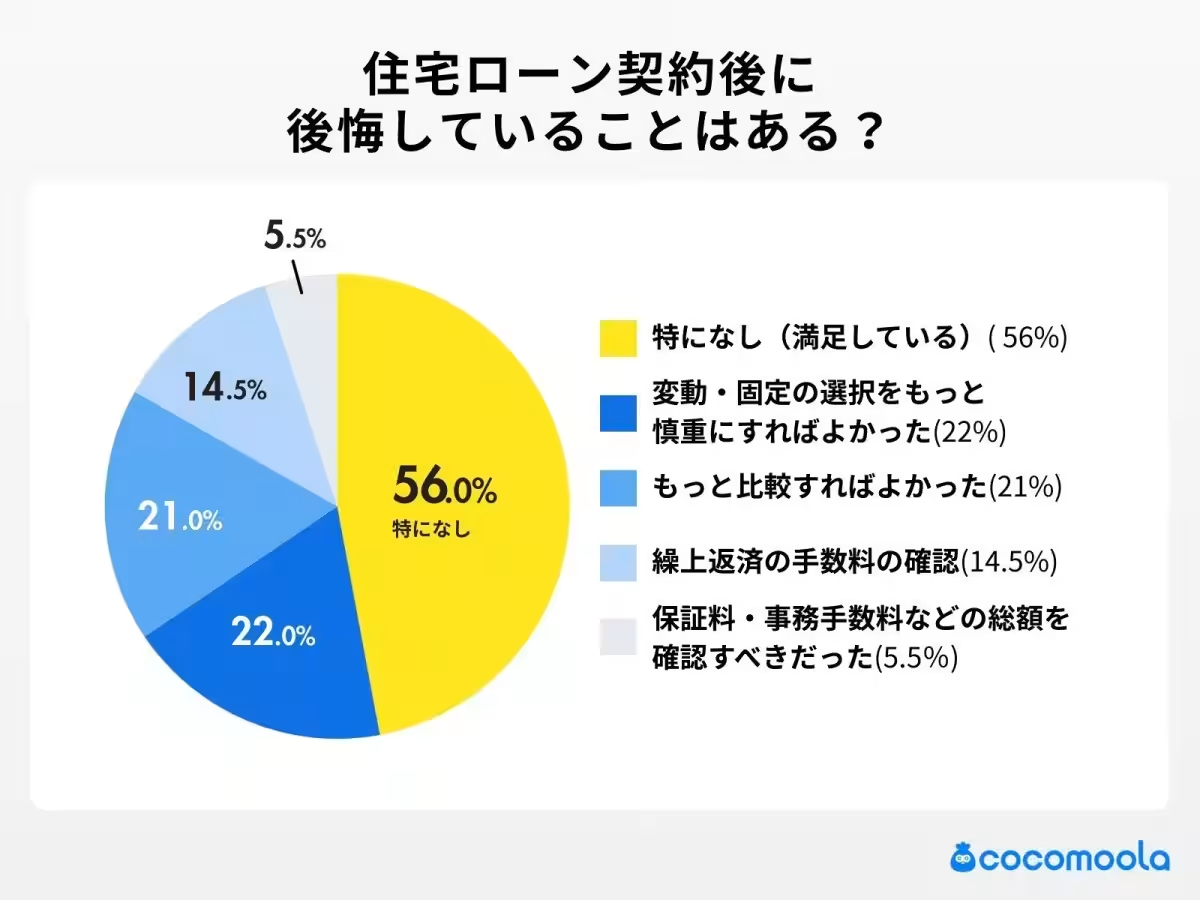

After securing their loans, a commendable 56% of participants reported satisfaction, stating they had no regrets about their decisions. However, for those who did express regret, the leading concerns included:

- - Choosing the type of interest rate (fixed or variable): 22%

- - Insufficient comparisons with other lenders: 21%

These regrets suggest that while many consumers felt content with their choices, a significant minority felt they could have made better informed decisions.

Recommendations for Future Borrowers

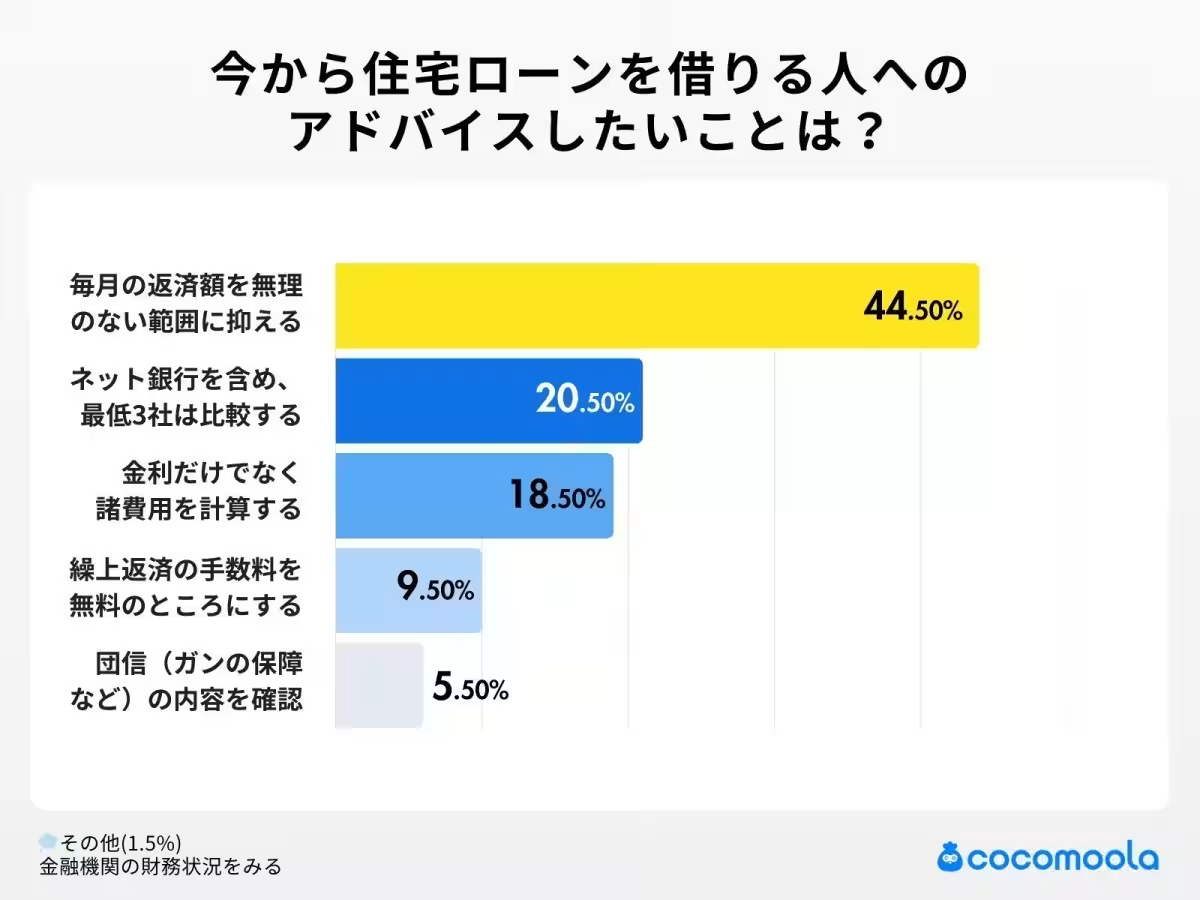

In light of the survey's findings, several recommendations emerged for prospective borrowers. Notably, 44.5% emphasized keeping monthly payments within a manageable range. Other recommendations included:

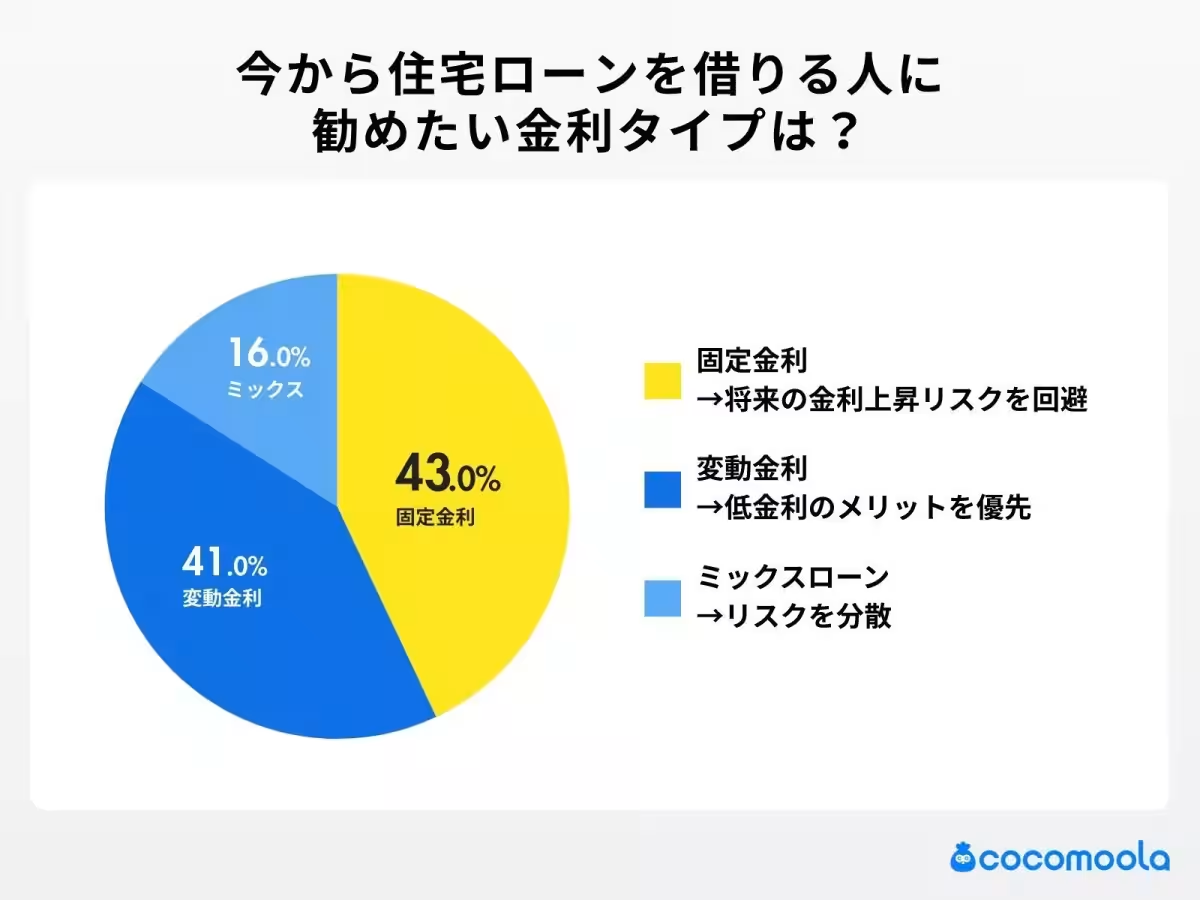

- - Opting for fixed rates (43%) vs. variable rates (41%),

- - Ensuring to compare at least three lenders, including online options.

These insights reflect the current economic climate and suggest cautious approaches to borrowing—a smart move in uncertain times.

Conclusion

Kokomora's survey presents a comprehensive overview of the current attitudes and preferences around housing loans in Japan. As the market continues to evolve, borrowers are encouraged to leverage data and insights like these to enhance their decision-making, ensuring financial choices align with their long-term goals. With the emphasis on fixed rates and manageable repayments, this survey provides both valuable insights for consumers and significant data for lenders looking to better meet the needs of their customers.

Kokomora aims to help users navigate housing loans and other financial products, ensuring they make informed decisions that best suit their lifestyles and financial situations.

Topics Consumer Products & Retail)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.