Trends in Rental Spaces Under 50 Tsubo for Early 2025: Analysis and Insights

Overview of Rental Trends for Small Commercial Spaces in Japan

A recent study conducted by At Home, Inc., based in Ota, Tokyo, analyzes the rental market for commercial spaces below 50 tsubo (approximately 165 square meters) across key urban centers: Tokyo, Nagoya, and Osaka. Commissioned to At Home Lab, Inc., this investigation focuses on the period from April to September 2025, offering essential insights for potential lessees and investors.

Key Findings in Tokyo Rental Market

In the Tokyo metropolitan area, the average rental prices for small commercial spaces have shown notable trends:

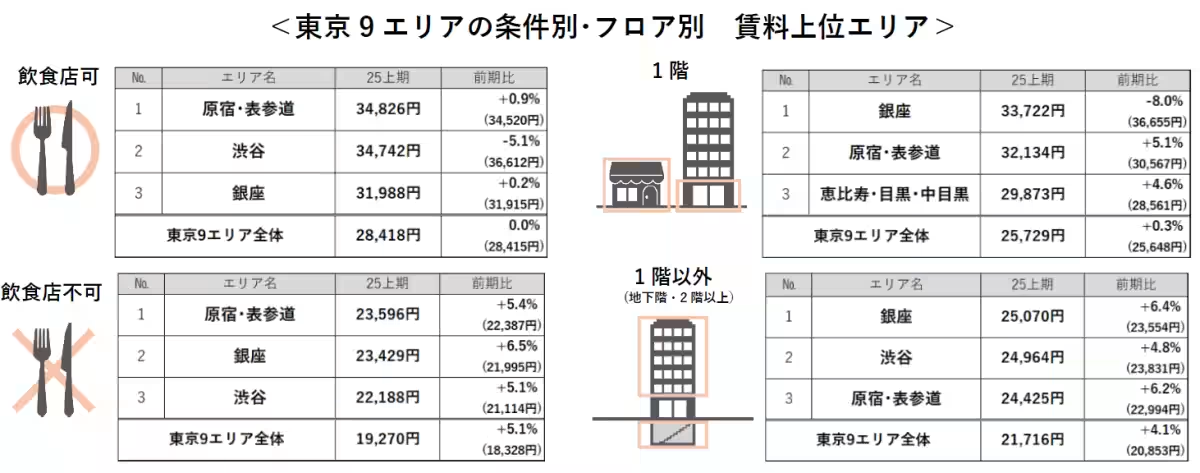

- - For properties allowed for restaurants, average rental rates stand at 28,418 yen per tsubo, showing no change from the previous term. In contrast, properties not suitable for restaurants have experienced an increase to 19,270 yen per tsubo, marking a 5.1% rise.

- - A significant difference is noted between the two categories, with restaurant-friendly spaces outpricing their counterparts by 9,148 yen, a difference of 47.5%.

In terms of floor location:

- - First-floor properties command an average rent of 25,729 yen per tsubo, slightly increasing by 0.3% from the last term. Conversely, spaces located on floors other than the first run at 21,716 yen per tsubo, indicating a 4.1% increment.

- - First-floor spaces, therefore, are more expensive by 4,013 yen, or 18.5% higher, illustrating the enhanced demand for visibility and accessibility in prime business locations.

Despite the rising prices, the overall availability of rental properties has decreased by 0.6%, indicating a continuous decline for six consecutive terms in the number of openings.

Developments in Nagoya and Osaka Markets

- - In Nagoya, specifically around the station, recent data highlights a surge in rents for properties not suitable for restaurants and for non-first-floor spaces, reaching record highs since the first half of 2018.

- - Similarly, in Osaka, areas like Namba and Shinsaibashi have seen rental rates for all types—both conditional and by floor—continue to rise, marking the third consecutive increase since 2018, which speaks to the recovering demand for retail and service spaces post-pandemic.

Area-specific Insights

The research targeted several bustling districts:

- - Tokyo: Key locations include Ginza, Shimbashi, Roppongi, Shibuya, Harajuku, Ebisu, and Ikebukuro, among others.

- - Nagoya: Focused on areas around Nagoya Station and Sakae.

- - Osaka: Emphasis was placed on Umeda, Namba, and Shinsaibashi, which are known for vibrant commercial activity.

Research Methodology

The study was based on data from properties listed in At Home's real estate network:

- - The properties analyzed were exclusively leased spaces or those combining leasing with office functions, all located within a 10-minute walk from train stations.

- - The average rental prices are derived from the median per tsubo, inclusive of common fees excluding taxes.

- - In cases where multiple units were available from the same building during the six-month period, only the latest available listings were considered.

- - Properties were categorized based on accessibility for restaurants and their respective floor locations to provide a detailed analytic outlook.

For in-depth insights, readers can download the comprehensive report from At Home.

As the rental landscape continues to evolve, this analysis serves as a crucial resource for businesses looking to navigate the competitive market for small commercial spaces in major urban areas.

Topics Consumer Products & Retail)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.