The Latest Insights on Pocket Money Trends Among Japanese Schoolchildren

Insights into Japanese Schoolchildren's Pocket Money

The financial habits of Japanese children have emerged as a topic of interest, particularly in light of a recent survey conducted by the Hakuhodo Educational Foundation's Children Research Institute. This survey targeted students from the fourth grade of elementary school through the third year of junior high school, aiming to explore various topics surrounding children's finances just before the new school year. It’s common for parents to ponder how much pocket money to allocate as their children advance in school. The survey results unveil some intriguing insights:

Average Monthly Allowance

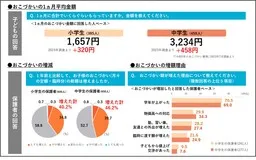

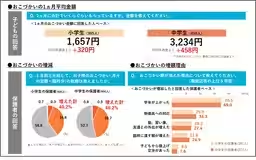

The average monthly pocket money reported was 1,657 yen for elementary students and 3,234 yen for junior high students. In comparison to last year's survey, elementary school students have seen an increase of 320 yen, while junior high students' allowance rose by 458 yen. This increase reveals how the financial needs of children indeed evolve as they progress in their educational journey.

When dissecting the figures further, it was found that 34.8% of elementary students fall into the category of receiving between 1,000 yen and 2,000 yen, while for junior high students, 29.5% receive between 3,000 yen and 4,000 yen. Sufficient allowances have led to a sense of financial satisfaction, with around 66% of elementary students and 67.7% of junior high students expressing contentment with their financial resources.

Reasons for Increased Pocket Money

About 40% of parents reported that their children's total allowances have increased over the past year. The primary reasons cited include moving up a grade, which accounted for nearly 70% of responses, and 30% attributing it to rising living costs. Additionally, factors such as increased extracurricular activities and outings with friends also contributed to this increase.

Spending Habits

Both elementary and junior high students primarily allocate their pocket money toward snacks and drinks and books or manga, with 60% designating their funds for the former and approximately 30% for the latter. However, notable differences arise when looking at spending on eating out or transportation for outings, with junior high students spending significantly more in these areas. For instance, 46.4% of junior high school girls indicated spending on eating out, showcasing a shift in social dynamics as they grow older.

Methods of Receiving Allowance

A significant majority of children, over 90%, still receive their pocket money in cash, reflecting traditional practices that persist. However, a growing trend is noted among junior high students, where 17.1% reported using QR code or barcode payment apps for receiving their allowances, highlighting a shift towards digital financial practices in younger generations.

Financial Awareness

Importantly, the survey highlighted a strong awareness and understanding among children regarding financial education. Around 90% agreed that learning about money management is crucial, and many expressed a desire to avoid wasteful spending. These sentiments indicate that younger generations are becoming more conscious of financial literacy and its implications for their futures.

Conclusion

The insights gathered from this survey by the Hakuhodo Educational Foundation not only shed light on how children manage their pocket money but also reflect broader economic influences and changing values among young people. As new school years begin and as children’s financial responsibilities evolve, it is clear that both parents and children are navigating this complex landscape with a keen understanding of financial aftereffects.

Methodology

The survey was conducted via the internet and included a nationwide sample of students from the fourth grade of elementary school to the third year of junior high school, obtaining necessary approvals from parents prior to participation.

Execution and Analysis

The analysis was collaboratively conducted by Hakuhodo Educational Foundation's Children Research Institute and QO Corporation, leveraging MacroMill's survey panel data. The results are part of an ongoing effort to understand the financial behaviors of children and their implications for future trends.

Topics Other)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.