Stabilization of Asia-Pacific Real Estate Market: New Investment Opportunities

Stabilization of Asia-Pacific Real Estate Market

Recent insights from the third quarter 2025 APAC Investment Atlas by Cushman & Wakefield, a leading global real estate services firm, indicate that the Asia-Pacific commercial real estate sector is shifting into a phase of stabilization. After navigating through economic challenges and worldwide uncertainties, the region is witnessing remarkable resilience and a restoration of momentum, creating appealing entry points for investors across various sectors.

Key Findings

- - Australia and Singapore are recognized as key entry points into the market, with Japan also maintaining its attractiveness.

- - Logistics and industrial real estate are leading the recovery, while retail and office sectors continue to attract high levels of investment interest.

- - The residential sector is particularly gaining attention in markets such as Australia, Japan, and South Korea.

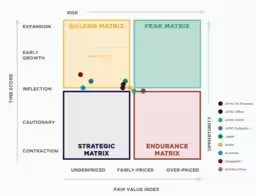

Informed by proprietary analytical models, Cushman & Wakefield's report combines the TIME (Timing Investment Market Entry/Exit) Score and the Fair Value Index (FVI) to provide a comprehensive evaluation of market dynamics. The TIME Score identifies optimal entry and exit points for real estate investments based on various sub-indicators across four primary aspects: cyclicality, momentum, growth, and risk. The scores range from 1, indicating contraction, to 5, denoting expansion.

The FVI assesses the current pricing attractiveness for investors, evaluating the likelihood of achieving risk-adjusted returns above, equal to, or below the anticipated returns from commercial real estate investments over a five-year holding period. The overall index is scored on a scale from 0 to 100, where 0 signifies all markets are fairly priced, and 100 reflects widespread undervaluation.

Dominic Brown, International Head of Research at Cushman & Wakefield, remarks, "The overall TIME Score for the Asia-Pacific region stands at 3.1, indicating a trend of early-stage growth in the real estate market. With lower interest rates and a liquid debt market fueling competition for prime assets, investor confidence is regaining, driving an upward trend in transaction activity and scale. We believe now is the perfect opportunity for investors to focus their efforts and capitalize on the region's long-term growth potential."

Across the region, strong rent growth and yield compression underscore the recovery led by logistics and industrial assets. The office sector is stabilizing after significant price adjustments, while the retail sector is approaching a pivotal point, particularly outside the Greater China area.

The Asia-Pacific FVI has surged from 22.7 in Q3 2022 to 62.5 by Q3 2025, suggesting that 46% of the market is currently undervalued—a considerable increase from the 18% two years ago. For value-oriented investors, Australia and Singapore emerge as particularly attractive markets, while Japan continues to be appealing due to low vacancy rates and a stable macroeconomic environment for industrial and office properties. Emerging markets like India and Southeast Asia remain enticing for cross-border capital, especially for industrial assets.

James Young, President of Markets for Asia-Pacific, Europe, the Middle East, and Africa, adds, "Financing is picking up, and core and core-plus strategies are making a comeback, accompanied by an uptick in value-add investments in high-growth areas such as data centers, residential facilities, and self-storage. These alternative assets have become major investment targets over recent years, and we expect continued interest in residential facilities across key markets like Australia, Japan, and South Korea."

Moreover, Young points out, "2025 started cautiously, with investor wariness lingering following market fluctuations and uncertainties. However, significant transactions, such as the $925 million prime office deal in Causeway Bay, Hong Kong, and the $1.47 billion sale of Pangyo Techno Valley Tower in South Korea, indicate that several significant deals have materialized in the region. This newfound momentum is expected to continue into 2026, driven by an accumulation of capital (dry powder) generated by investors."

In addition, Cushman & Wakefield has released its latest EMEA Investment Atlas, emphasizing that debt capital is propelling the recovery in the European real estate market. The EMEA region's TIME Score has risen to 3.2, affirming that the market is at a turning point, with recovery spreading across sectors. Logistics, retail, and hospitality are firmly positioned as investment sweet spots, supported by strong operational benchmarks and increasing demand. According to the FVI for EMEA, 78% of tracked markets are deemed undervalued, with logistics leading the way in opportunities due to solid fundamentals, while Germany exhibits ongoing undervaluation across all markets and sectors.

For a comprehensive analysis, the full report is available for download in PDF format. Detailed assessments of APAC and EMEA regions and specific sector investment opportunities are also accessible via respective regional reports on our website: APAC Investment Atlas and EMEA Investment Atlas.

About Cushman & Wakefield

Cushman & Wakefield (NYSE: CWK) is among the world's leading commercial real estate service firms, publicly traded on the New York Stock Exchange. With a workforce of approximately 52,000 across 400 offices in nearly 60 countries, the firm supports various services, including facility management, leasing, investment sales, tenant representation, appraisal, and project management. Anticipated to achieve revenues of $9.4 billion in 2024, Cushman & Wakefield operates under the philosophy of 'Better never settles' and is lauded for its award-winning corporate culture. For more information, visit www.cushmanwakefield.com.

Topics Consumer Products & Retail)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.