Tokyo Office Market Trends as of February 2026: Vacancy Rates and Average Rents

Tokyo Office Market Overview - February 2026

In February 2026, the Tokyo office market has exhibited notable trends in both vacancy rates and average rental prices. According to a survey conducted by Mitsubishi Estate Real Estate Services, the office vacancy rate stands at 2.47%, reflecting a 0.07 percentage point increase from the previous month. Meanwhile, the average asking rent has risen to 29,331 yen per tsubo, marking an increase of 1,329 yen per tsubo compared to the previous month.

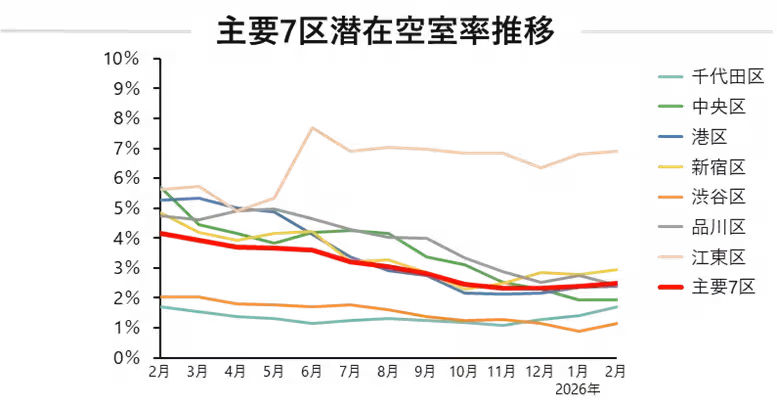

Vacancy Rates Explained

The survey highlighted the potential vacancy rate in major districts, which currently rests at 2.08% for the top five areas, and 2.47% for the top seven, both showing slight month-over-month increases. This data presents a clearer picture of the availability and demand within the important commercial zones of Tokyo.

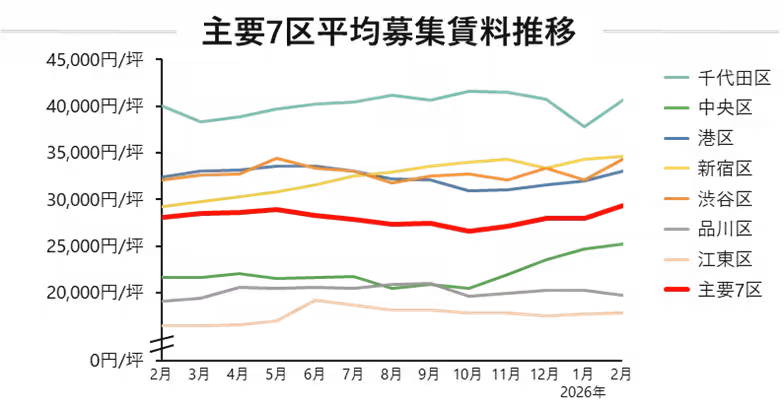

Average Rental Prices

The average rental pricing in the major five districts has climbed to 34,125 yen per tsubo, with a month-on-month uptick of 1,613 yen per tsubo. In the broader scope of the major seven areas, as mentioned earlier, the average price is 29,331 yen per tsubo. Notably, specific districts such as Marunouchi, Otemachi, and Yurakucho have seen significant activity, bolstered by substantial new listings exceeding 3,000 tsubo in this price range, leading to a remarkable price increase of 2,469 yen per tsubo.

Conversely, the Roppongi and Akasaka areas have experienced strong demand, reflected in average rent surges of 2,726 yen per tsubo, primarily due to new listings priced above 50,000 yen.

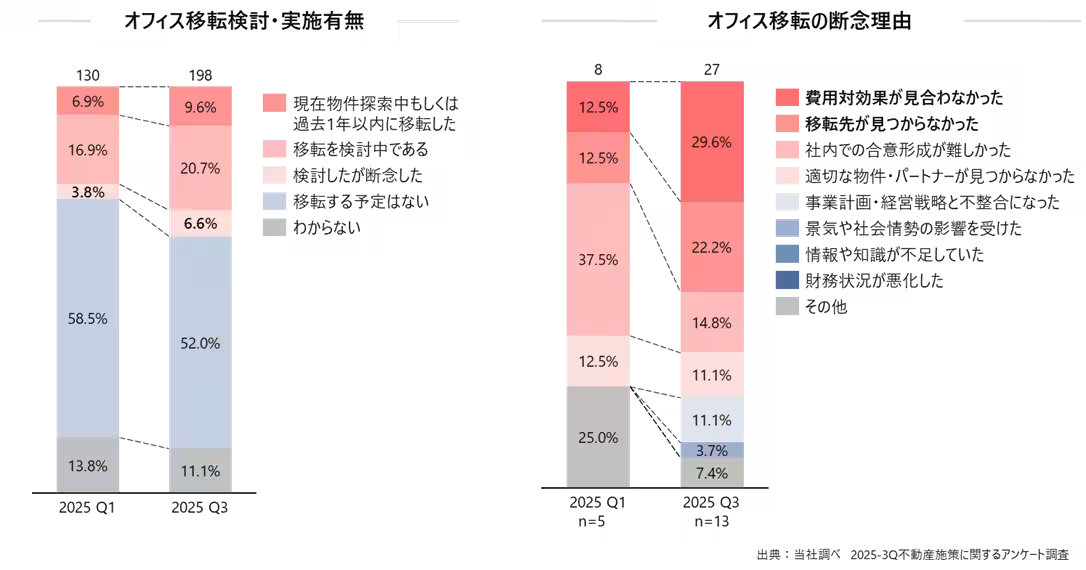

Trends in Office Relocation

A key focus of the survey reveals a growing trend in office relocations. The percentage of firms considering or actively relocating their offices has risen by 6.5 percentage points, signaling a robust interest in workspace optimization. However, the data also shows that the number of firms that have considered relocation but ultimately decided against it increased by 2.8 percentage points. The reasons cited include a lack of cost-effectiveness—up 17.1 points since the previous measurement—and difficulty in finding suitable new spaces—up 9.7 points. These trends emphasize the market's increasing pressures regarding rental costs and office availability.

Survey Methodology and Data

This report is based on data from 992 buildings, a slight increase of one from the preceding month, as of the end of February 2026. The buildings surveyed include those with a minimum of 3,000 tsubo located in the central wards of Tokyo: Chiyoda, Chuo, Minato, Shinjuku, Shibuya, Shinagawa, and Koto. Special considerations were made for buildings affected by unique circumstances which led to their exclusion from the regular rental market analysis.

The newly refined measure of potential vacancy rate provides a more accurate long-term perspective on supply by focusing solely on immediately available spaces, rather than traditional metrics which encompass all vacant floors. This new metric highlights the critical need for immediate occupancy within the Tokyo office space market.

Conclusion

In summary, Tokyo's office real estate market is navigating fluctuating vacancy rates and rising rental prices as of February 2026. The dynamics of demand and the pressures of limited supply indicate that this sector remains under significant stress, shaping the long-term strategies of businesses as they consider their office space needs. Mitsubishi Estate Real Estate Services will continue to monitor these trends closely and provide insights for navigating this ever-evolving market landscape.

Topics Consumer Products & Retail)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.