Japan's Audit on Social Welfare Facilities Reveals Structural Challenges and Urgent Needs

Japan's Audit on Social Welfare Facilities: A Call to Action

In a recent study conducted by Japan System Co., Ltd., the stark realities surrounding the supervision and auditing of social welfare facilities across 15 municipalities have been unveiled. This investigation highlights that the increasing demand for audits is not merely a temporary issue but a symptom of deeper, systemic challenges that continue to escalate.

Background of the Investigation

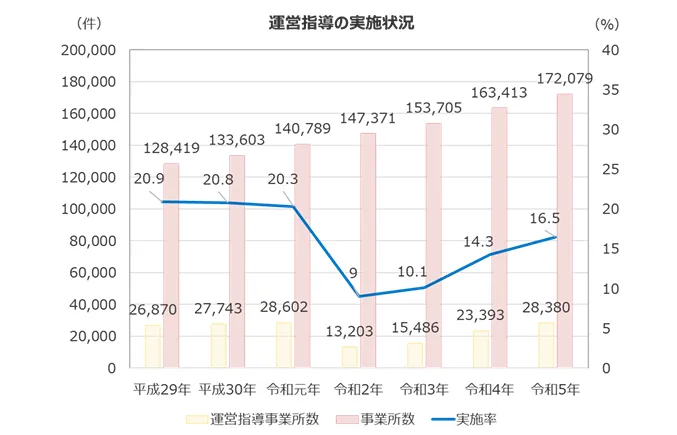

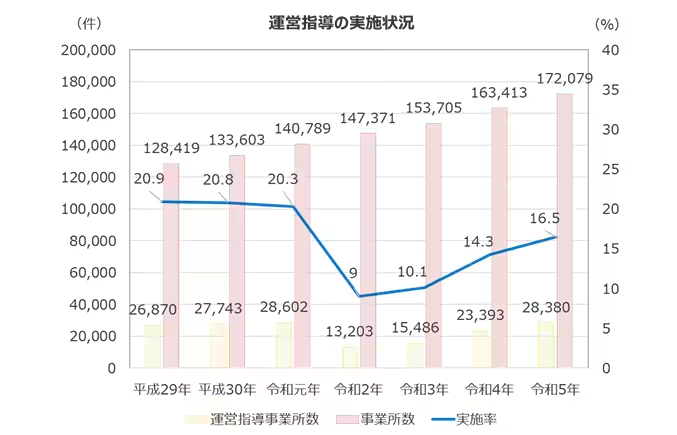

The urgency of this audit stems from significant past incidents, particularly a fraudulent benefit claim amounting to approximately 11 billion yen linked to "Kizuna Holdings" in Osaka City in March 2026. This incident prompted the national authorities to tighten regulations and enhance auditing processes. However, on the ground, municipalities face a growing number of facilities to monitor, outdated operational methods, and staffing shortages, making proper audits increasingly difficult. Currently, the auditing rate in the field of disability welfare stands at a mere 16.5%, which starkly contrasts with the national government’s expectations for operational improvements. Therefore, a pressing concern remains: how can the efficacy of audits be bolstered to prevent future fraudulent activities?

Japan System leverages insights gained from a trial project in collaboration with Miyazaki Prefecture in 2025, which focused on the unification of planning and management in supervising welfare facilities. Recognizing that similar challenges are faced by other municipalities, they undertook this comprehensive study.

Study Overview

Objectives:

- - To gather insights from frontline personnel involved in auditing welfare facilities, grasping both the current operational reality and expectations or concerns about standardization.

- - To delineate the different circumstances across municipalities, identifying common aspects that can be standardized versus those requiring tailored approaches.

Target Municipalities:

The study encompasses a diverse range of municipalities, including:

- - 6 Prefectures

- - 7 Designated Cities

- - 1 Core City

- - 1 Other Municipality

Methodology:

- - Direct interviews with departments responsible for auditing, conducted on-site.

- - Each session lasting between 1.5 and 2 hours.

Summary of Findings

Through interviews with the 15 municipalities, several multifaceted and structural challenges were identified across various audit processes:

1. Preparation:

- The burden of gathering and reconciling facility and audit data is exceedingly high.

2. On-Site Audits:

- While there's a demand to reduce the burden on providers, the number of audit items has increased annually, heightening the workload for both auditors and facilities.

3. Report Creation and Record Keeping:

- Auditors face inefficiencies caused by excessive data entry and potential errors due to the large volume of information.

4. Inter-Departmental Coordination:

- Information is scattered across different platforms, complicating progress tracking and understanding among staff involved.

5. Knowledge Accumulation and Sharing:

- The absence of a system to accumulate and disseminate knowledge forces reliance on the experience of individual staff, affecting the overall quality of guidance.

6. Organization and Resources:

- Only larger municipalities with higher budgets can utilize external entities effectively, limiting operational guidance elsewhere.

7. Constraints on System Implementation:

- Budget limitations hinder the ability to adopt systems designed to enhance operational efficiency.

Perspectives from the Field:

- - Preparation: Many municipalities struggle with varying formats of data collected by different departments, complicating the creation of comprehensive facility audit lists.

- - On-Site Audits: Small businesses, especially family-run operations, often lack familiarity with digital communication methods, complicating the audit process.

- - Knowledge Sharing: The absence of a systematic manual means reliance on anecdotal knowledge and prior memos without documentation of the reasoning behind decisions.

The comprehensive report detailing these findings is available on Japan System's official website. It provides a critical analysis of the challenges, alongside potential pathways for improvement based on the operational efficiencies noted in previous projects.

Looking Ahead

The enhancement of audit implementation rates remains a pivotal goal, necessitating a balance between meeting regulatory requirements and ensuring the effective use of resources towards genuine improvements in facility operations. As Japan System profoundly understands these dynamics, they strive to transition towards a more integrated and efficient auditing framework that prioritizes both compliance and effectiveness.

For further insights into Japan System’s initiatives and their advocacy for structured improvements in the social welfare audit system, visit their official site.

Topics General Business)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.