Understanding the First Salary: Insights from New Graduates in Japan

Understanding the First Salary: Insights from New Graduates in Japan

On April 24th, many new graduates eagerly awaited their first salary payment, a significant milestone in starting their professional journey. However, how well do these fresh entrants understand their pay slips? To shed light on this question, Yuichi Sugawara, a tax accountant and the creator of the popular YouTube channel "脱・税理士スガワラくん" with over 1.65 million subscribers, conducted a survey involving 160 new Japanese graduates this year. This article presents the findings from the survey and provides an easy-to-understand breakdown of pay slips.

Survey Overview

- - Survey Period: April 30 to May 6, 2026

- - Method: Online survey

- - Demographic: New graduates aged 18-25

- - Sample Size: 160 respondents

- - Conducted By: Freeasy

Note: Please cite "脱・税理士スガワラくん 調べ" when using the survey results.

Key Findings

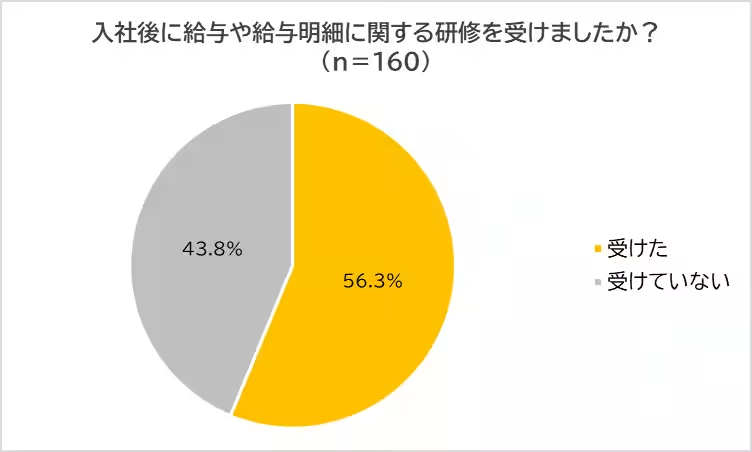

The survey began by asking, "Did you receive any training regarding salary and pay slips after joining?" Over half, 56.3%, reported that they did receive training, while 43.8% said they did not. This suggests that more than 40% of new employees may not fully understand the breakdown and mechanics of their salaries.

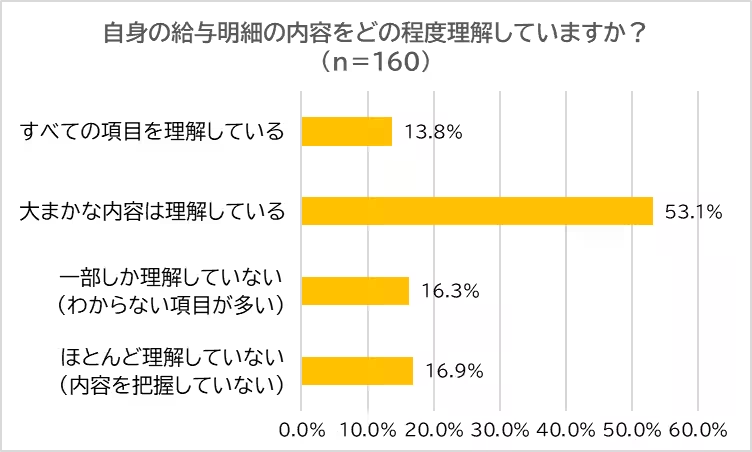

Next, when asked about their comprehension of their pay slips, only 13.8% claimed to understand all the components. A significant portion, 53.1%, felt they had a general idea, while over 33% reported only partial understanding, highlighting a concerning gap in financial literacy among new employees. Despite receiving pay slips monthly, many are oblivious to their content's importance.

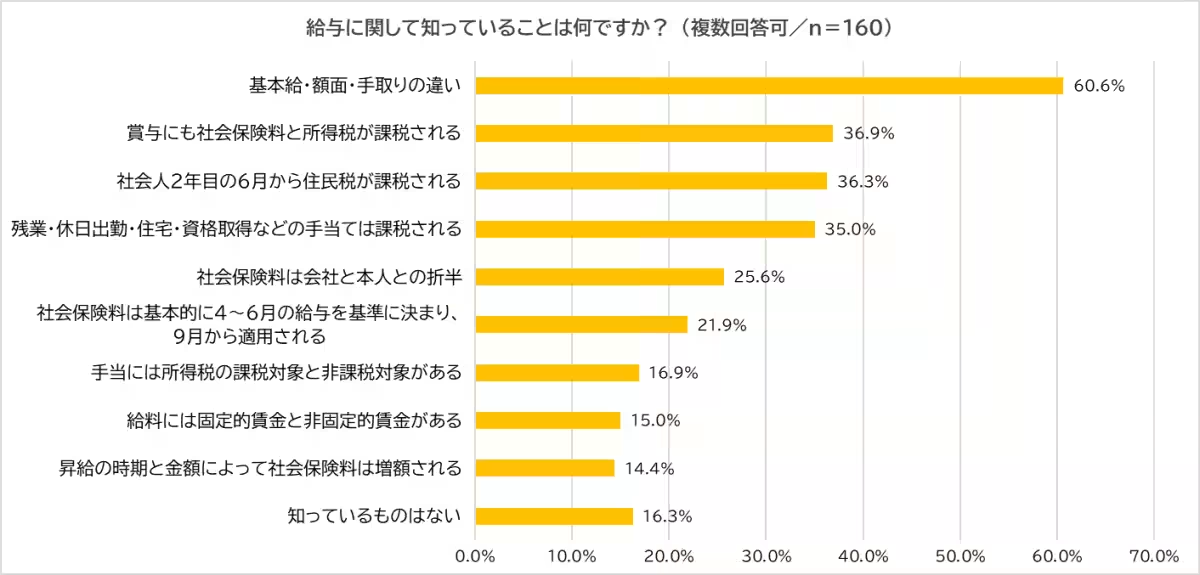

When probed about what they knew regarding salaries, the leading answer was the difference between basic salary, gross income, and net income (60.6%). However, knowledge about social insurance premiums and various deductions was less robust; only about 20% knew that social insurance is calculated based on salaries from April to June and that premiums are shared between employer and employee. Furthermore, insights into taxable and non-taxable allowances were significantly lower, with almost 16.3% admitting they knew nothing about the payment system—underscoring the necessity for improved financial education for new graduates.

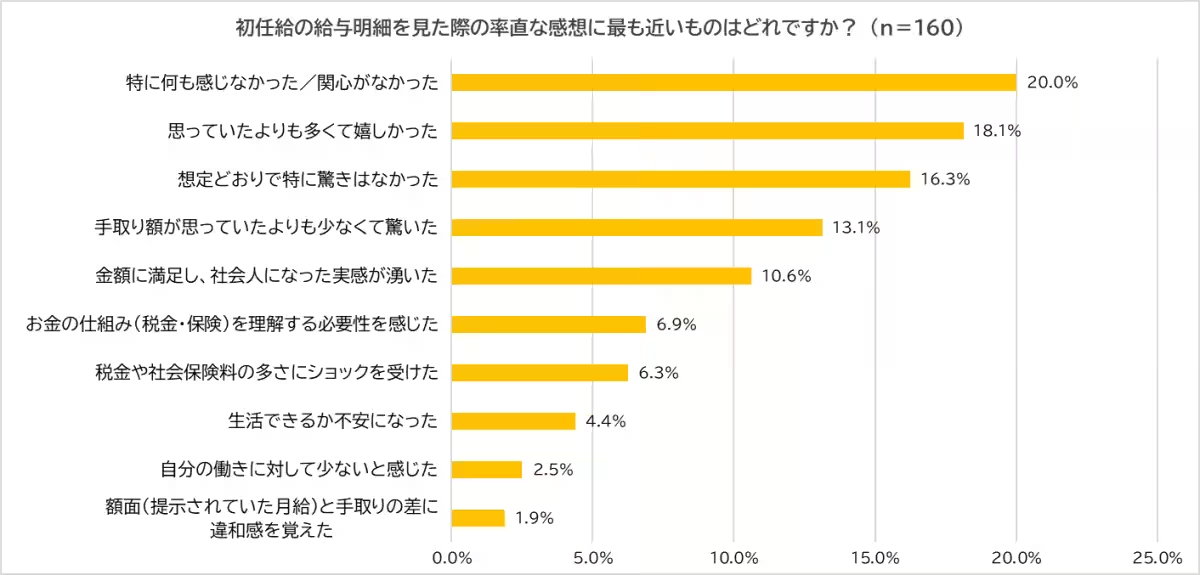

Lastly, respondents were asked for their candid impressions upon reviewing their initial pay slips. The most common response was, "Did not feel anything in particular/wasn't interested" (20.0%). While the first salary represents a significant moment in one’s life, a surprising number of young professionals seem uninterested in understanding the financial implication. Nonetheless, there were also positive comments, with some reporting surprise and satisfaction at receiving more than they anticipated. In contrast, others expressed shock at lower take-home pay than expected or the hefty deductions for taxes and social insurances, leading to worries about their livelihood. Some expressed the desire to better understand financial systems affecting their income.

A Comprehensive Guide to Understanding Your Pay Slip

This survey highlights that many new professionals glance at their pay slips without truly understanding the deductions for taxes, social insurance, and the concept of take-home pay. In an era where living costs are rising and the focus on disposable income is more prominent, the first salary is not merely a paycheck but an opportunity for financial education. Here are essential fundamentals regarding pay slips and take-home pay:

Key Differences

- - Basic Salary: The fixed monthly wage.

- - Gross Salary (Total Compensation): Basic salary plus various allowances and bonuses.

- - Net Salary: The amount you actually receive after tax and social insurance deductions. So, the equation is: Gross Salary - Deductions = Net Salary.

Three Key Points to Check on Your Pay Slip

1. Deductions: Verify that health insurance, employee pension, employment insurance, and taxes are accurately deducted.

2. Take-Home Pay: Ensure the net amount matches what is deposited to your account.

3. Pay Date and Cut-Off Date: Understand which month your salary covers.

How are Social Insurance Premiums Determined?

Social insurance consists of five types: Health Insurance, Employee Pension, Employment Insurance, Long-term Care Insurance (for applicable individuals), and Workers' Accident Compensation Insurance. It is calculated based on monthly salary averages for certain periods.

- - Health Insurance Premium: Covers medical expenses; rates vary based on the health insurance association.

- - Employee Pension Premium: Provides benefits during retirement, disability, and death; rates are similarly based on salary averages.

- - Employment Insurance: Supports individuals in case of unemployment; calculated based on the rate specific to one's industry.

The monthly salary also includes additional compensation, such as commuting assistance, housing benefits, overtime pay, etc. Notably, temporary payments like bonuses and certain allowances are not included when calculating this average.

The Importance of the Seasonal Earnings

It’s essential to be cautious about the working hours during April to June as they affect your social insurance premiums for the entire year. The more hours worked and the higher the salary, the higher the premiums, thus reducing take-home pay for the future months. Therefore, working excessively during this term could ultimately be disadvantageous.

Don't Forget About Resident Tax

Resident taxes commence from the second year. New employees might find their net salary unexpectedly decreased during their second year as they start incurring this tax.

Keep Your Pay Slips

Pay slips serve vital purposes beyond just a document of verification. They act as proof of income, assist during disputes, and are essential for future financial applications like home purchases or career advancements. Ensure you preserve these documents, either digitally or physical copies.

Conclusion

Take-home pay is determined after accounting for deductions, with social insurance premiums significantly influencing this amount. Furthermore, being mindful of how the salary from April to June impacts the annual premiums is crucial, as is being aware of the additional burden of resident tax that begins in the second year. Understanding these variations can ensure new professionals are better prepared. Regularly reviewing your pay slip and keeping them secured is imperative.

About Yuichi Sugawara

Born in 1975 in Mie Prefecture and currently residing in Tokyo, Yuichi Sugawara is a financial expert specializing in tax savings and financial management. His YouTube channel "脱・税理士スガワラくん" was launched in December 2022, surpassing 1.65 million subscribers and earning a reputation as a leading tax blog in Japan. He has provided over 1,000 lectures for various corporations and is a sought-after media expert. He has authored several bestselling books on finance and business.

YouTube Channel

Blog

Topics People & Culture)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.