New Lease Accounting Standards Prompting Companies to Start Serious Consideration

Overview of the New Lease Accounting Standards

As the new lease accounting standards set to take effect in April 2027 gather momentum, a recent survey conducted by Proship Inc. sheds light on the preparedness and challenges that companies face in adopting these changes. With an increasing focus on lease and asset management solutions, Proship's study targeted accounting professionals, revealing critical gaps and inconsistencies in how businesses are preparing for these upcoming standards.

Key Findings of the Survey

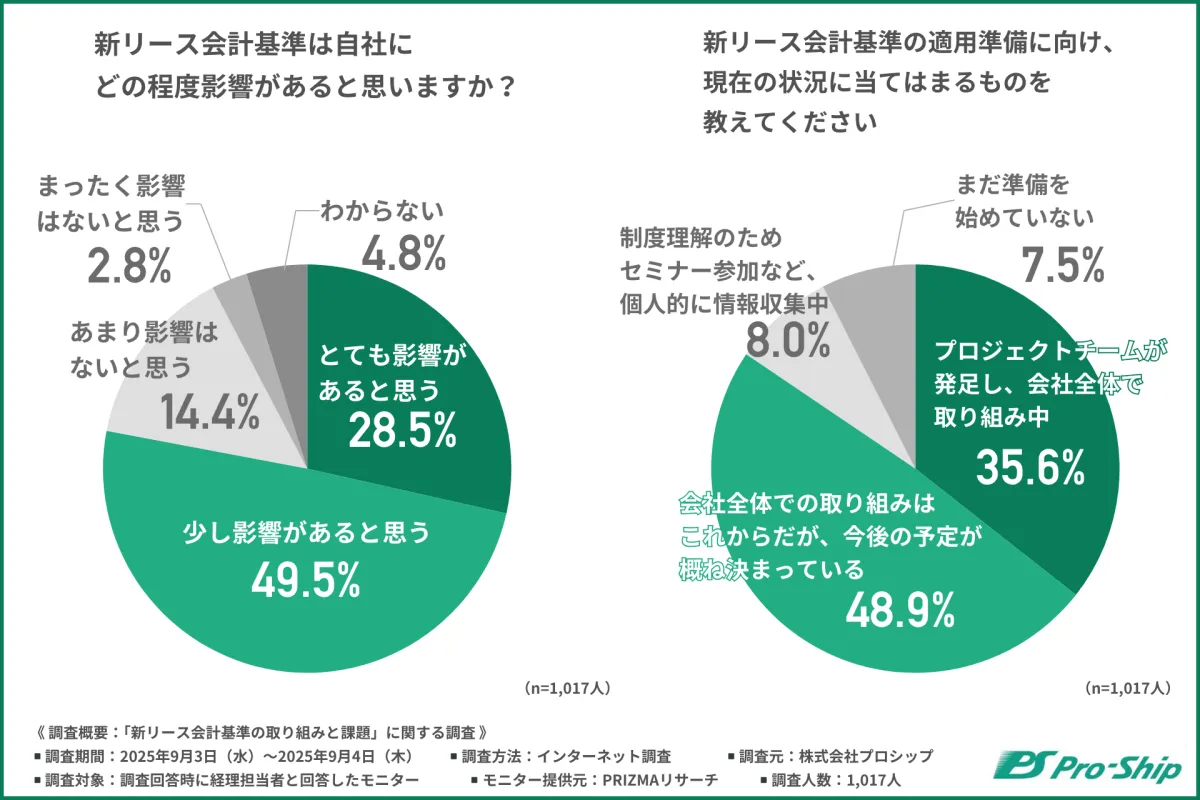

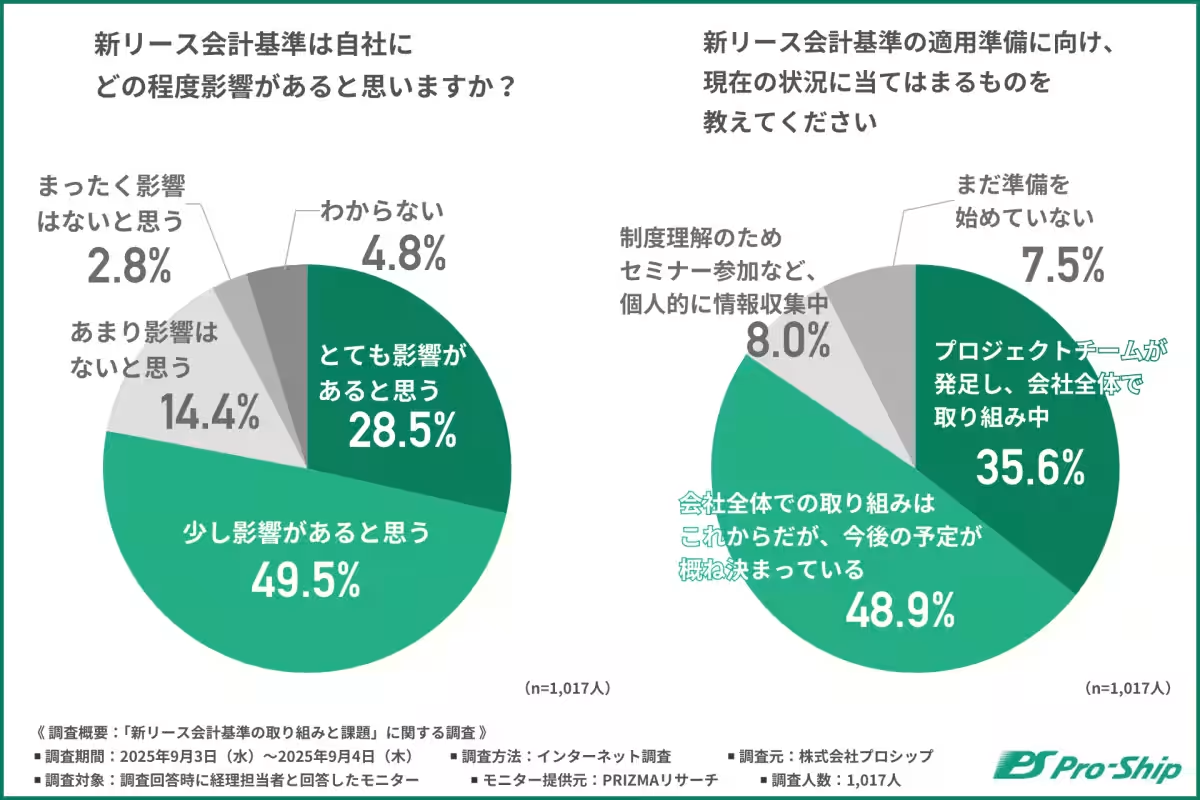

The survey revealed that while around 80% of companies acknowledge the significant impact of the new lease accounting standards, about 60% are still in the early stages of their preparations. The findings echo those from a previous survey conducted in May 2025, indicating that, although awareness is high, actual progress toward formal adoption varies widely across different organizations.

Project Teams and Initial Challenges

Among the 1,017 accounting professionals surveyed, 35.6% reported that their companies had formed project teams to address this issue, while 48.9% stated that they had plans in place but had yet to initiate comprehensive efforts. Notably, the proportion of companies not actively preparing has decreased, yet a significant number still struggle with the initial steps—such as estimating the financial impact of the new standards and organizing accounting issues. This indicates a broader hesitation to shift from understanding the regulations to translating that understanding into practical application.

Identifying Lease Contracts

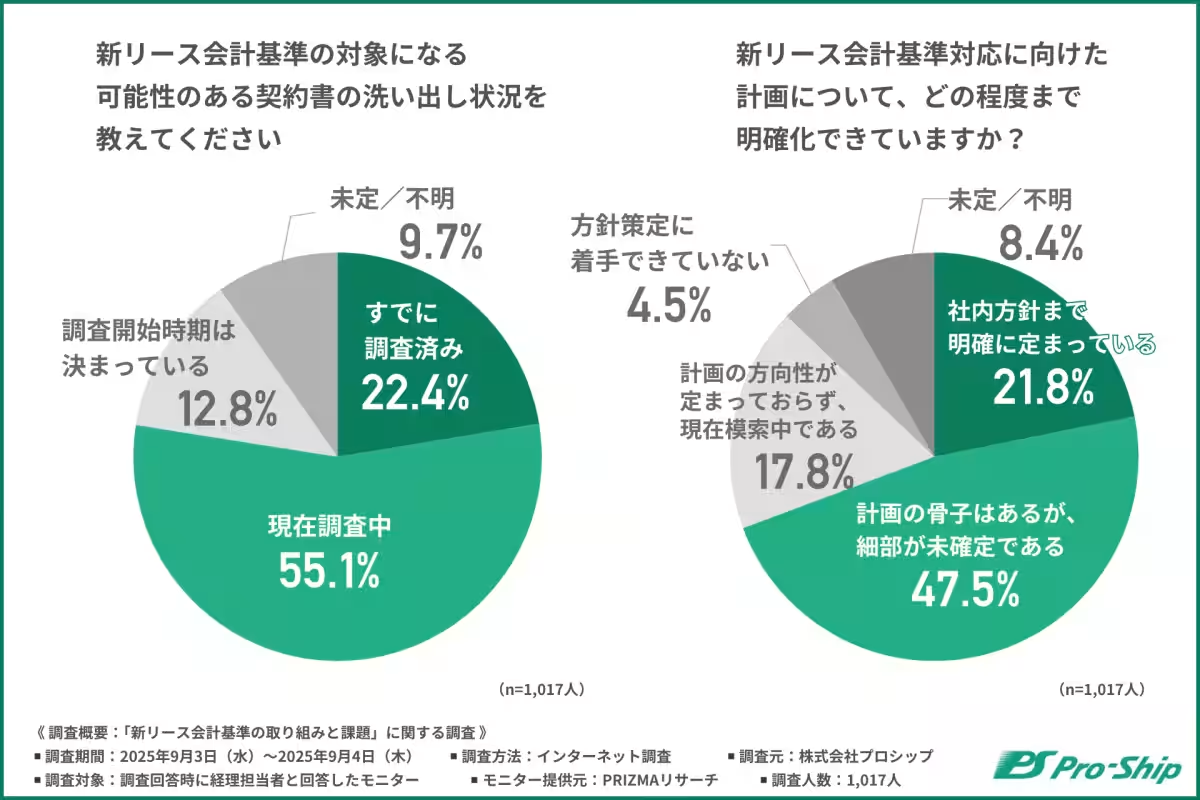

A crucial step in this process involves identifying which lease contracts will be affected under the new standards. Remarkably, around 80% of the businesses surveyed indicated that they are either currently conducting reviews of relevant lease contracts or have completed this process. However, only 22.4% confirmed that the process is fully complete, highlighting a concerning delay in essential preparatory work.

Current Status of Internal Strategies

When questioned about whether companies had clear internal strategies for compliance, only about 21.8% confirmed that their strategies were well-defined. The majority stated that while they had a basic plan, details remained uncertain, revealing a general sense of confusion that affects decision-making. Preparing for the new standards is an urgent task that demands extensive collaboration and clarity within organizations.

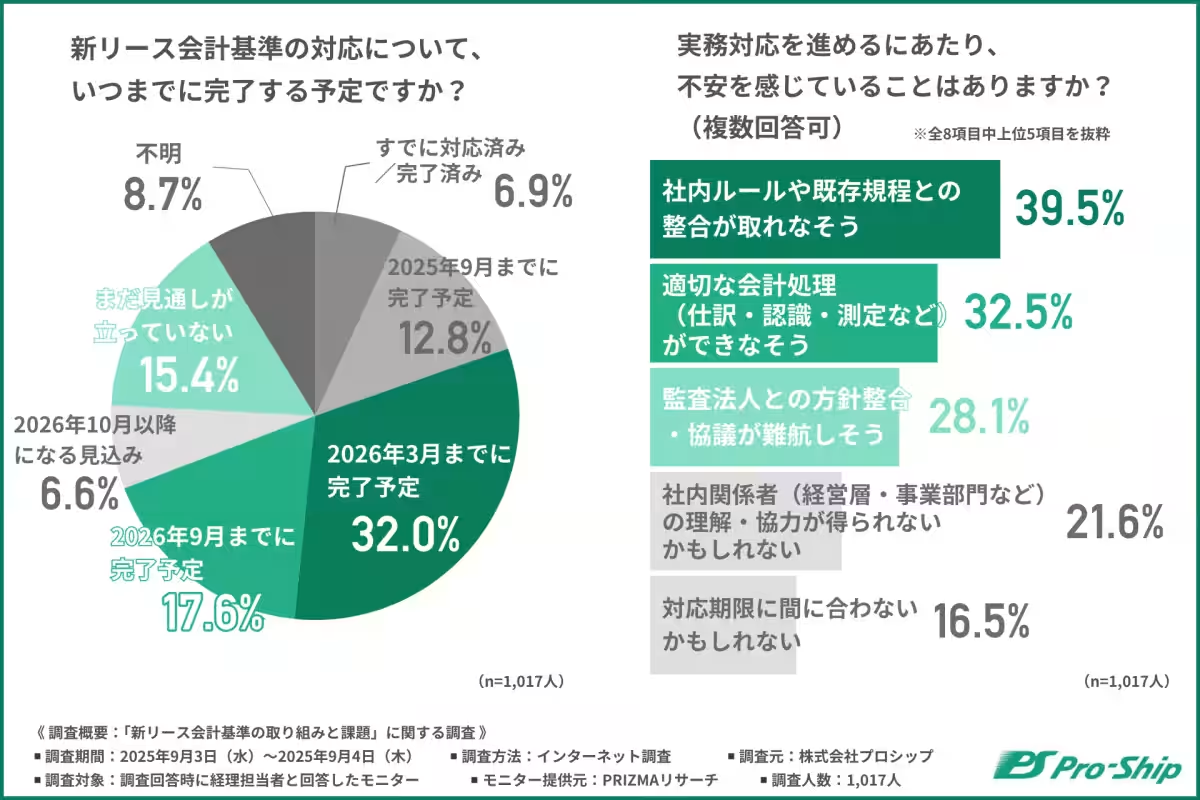

The Roadblocks Ahead

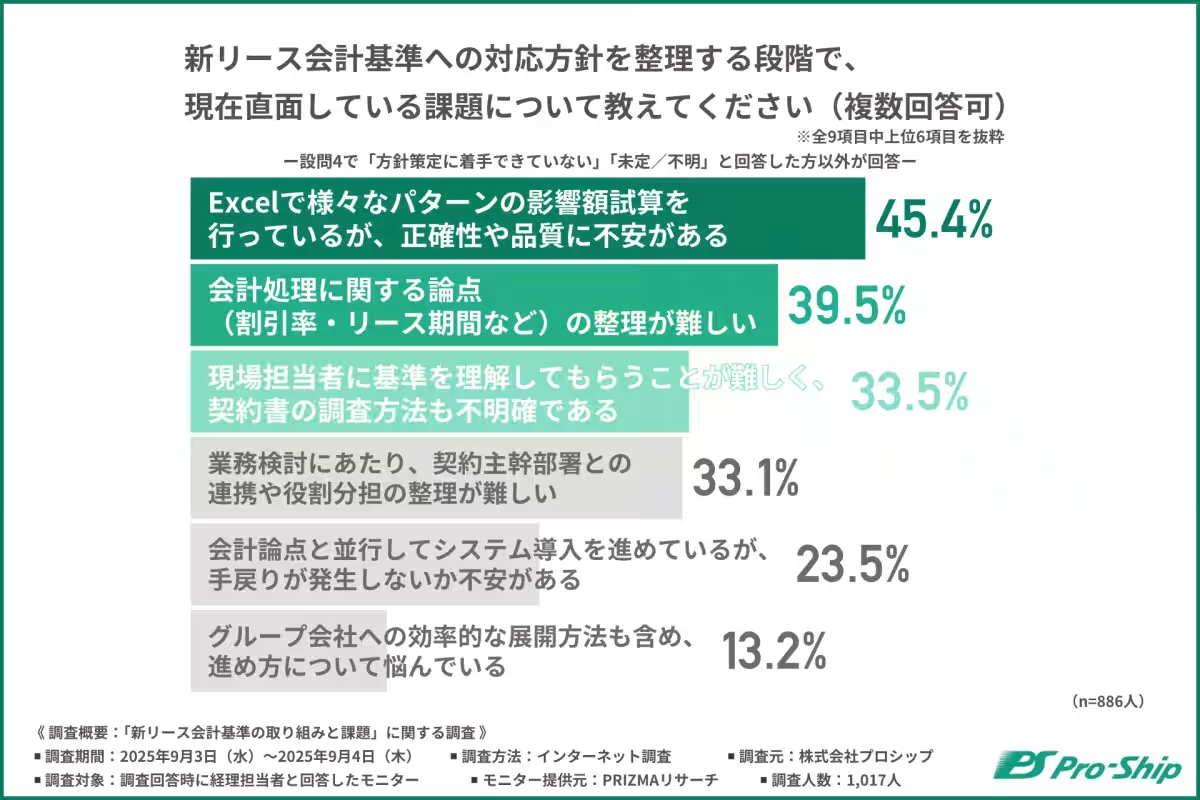

Several organizations expressed concern about their readiness to implement the new lease accounting standards. Common issues include uncertainty regarding how to accurately calculate financial impacts using tools like Excel, difficulties in understanding accounting treatment aspects (such as determining the discount rate and lease term), and lack of clarity regarding how to train onsite personnel about these new standards. These obstacles have prompted many companies to seek external guidance to streamline their internal processes and clarify their compliance strategies.

Diverse System Solutions

Interestingly, the approach to system capabilities is inconsistent among companies. Approximately 40% of respondents are exploring new system implementations or modifying existing systems to accommodate the changes prompted by the new standards. However, the remaining 60% of companies are either not planning any system upgrades or are still in the consideration stage, relying on manual processes and Excel spreadsheets.

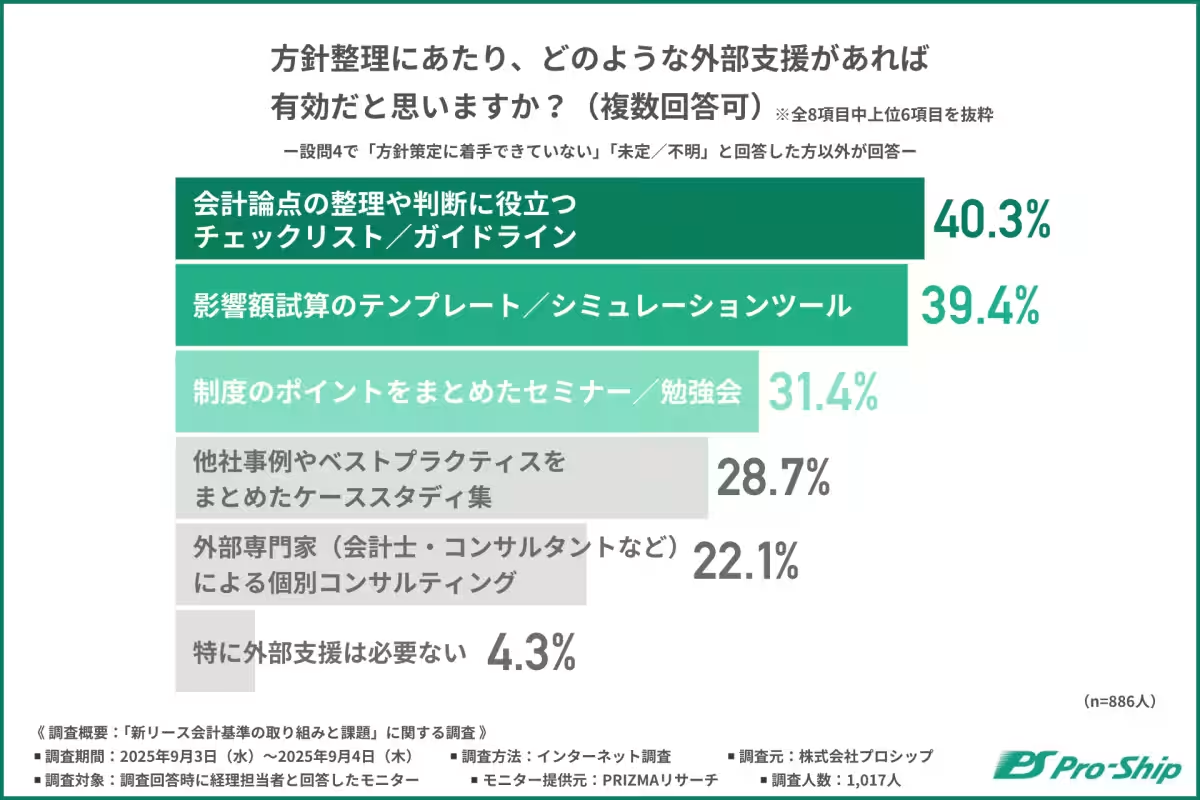

Need for External Support Grows

The findings also highlight a growing need for external support in navigating the complexities of the new lease accounting standards. Many companies identified the value of checklists and template tools designed to assist with estimating financial outcomes and organizing accounting issues effectively. While there is a lower demand for individual consulting services, a significant number of companies still express a desire to advance in compliance with accessible resources and practical support tools.

Timeline for Completion

As companies assess their compliance timelines, many aim to complete the necessary preparations by March 2026, with approximately 32% expecting to finalize their strategies by then. However, there remains a concerning percentage of respondents who either have not completed preparations or lack a clear timeline for when they will be finished. This raises potential risks of non-compliance as the deadline approaches.

Concluding Thoughts

The survey underscores the urgent need for organizations to not only understand the new lease accounting standards but also to act swiftly to integrate these changes into their operational frameworks. Prioritizing the development of internal processes and leveraging available resources will be essential for businesses as they navigate this transitional phase. Proship is committed to providing comprehensive support tailored to help organizations effectively manage their compliance strategies for the upcoming lease accounting standards.

For more information and assistance regarding the new lease accounting standards, please visit Proship's official website.

Topics Financial Services & Investing)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.