Record Number of Deals in Senior Housing and Care Mergers and Acquisitions Seen in Early 2025

Surge in Merger and Acquisition Activity in Senior Housing

In the first quarter of 2025, the landscape of senior housing and care has experienced a noteworthy surge in merger and acquisition (M&A) activity. According to new acquisition data from LevinPro LTC, an impressive total of 176 deals were publicly announced during this period. This figure, while reflecting a 7.4% decrease from the fourth quarter of 2024, marks a 13.6% increase from the 155 transactions reported in the same period last year.

Despite the decline in the overall number of deals, the total spending on acquisitions in Q1 2025 reached an astonishing $5.79 billion. This represents a staggering 74.9% increase compared to the $3.31 billion allocated in the previous quarter and a 192.4% increase from the $1.98 billion of the first quarter of 2024. The resilience in investment underscores a robust recovery in the sector after a brief slowdown.

Ben Swett, the Managing Editor of The SeniorCare Investor, emphasized that the revival of M&A activity throughout 2025 is being driven by favorable conditions in the capital market and an improved operational environment for facilities catering to seniors. Swett noted that the second quarter is already showing signs of unprecedented deal-making momentum, setting a potentially record-breaking pace.

Monthly Trends in M&A Activity

A closer examination of the monthly breakdown reveals January's deal count was plummeted to just 47 transactions, making it the slowest month since February 2024. This low performance could be attributed to seasonal fluctuations or market hesitation. However, the momentum picked up as February saw a resurgence to 60 deals, with March witnessing a further increase to 69 transactions. Such trends suggest that January's figures could be an outlier instead of a reflection of a sustained downturn.

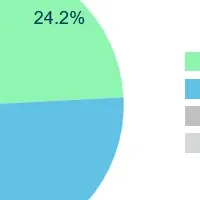

For the quarter, assisted living deals emerged as the most dominant category, accounting for 41.5% of total transactions. Skilled nursing closely followed, representing 37.5%, while independent living contributed approximately 16%. Continuing Care Retirement Communities (CCRCs) and other affordable senior apartments made up 2% and 1% of the deals, respectively.

The Future of M&A in the Senior Care Sector

Interestingly, the share of foreign deals appears limited as the property per deal ratio dropped to 2.09 in Q1 2025 compared to 2.55 in Q4 2024. It appears that while the volume of transactions surged, the size of individual deals saw a contraction. Swett mentioned a noticeable decrease in portfolio deals coming into the market during the early part of the year; however, expectations for the second quarter are positive, with indications that more portfolios are set to be marketed for sale.

The LevinPro database, which tracks long-term care M&A transactions since 1993, continues to serve as a crucial resource for stakeholders in this sector. With annual reports detailing trends in the seniors housing and care acquisition markets being published, industry players can gain in-depth insights into market developments.

In conclusion, despite a dip in total deals, Q1 2025 has heralded a new era of growth for the senior housing and care M&A landscape, with increased capital investment signaling a positive outlook for the future. As we move further into 2025, all eyes will be on the sectors' continued evolution amidst shifting market dynamics.

Topics Financial Services & Investing)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.