Major Delays in Preparing for New Lease Accounting Standards Ahead of 2027 Deadline

Major Delays in Lease Accounting Preparations

As the deadline for implementing the new lease accounting standards approaches in April 2027, a concerning trend has emerged: a recent survey conducted by ProShip Inc. indicates that more than half of the companies surveyed are still in the initial stages of preparation. This raises significant concerns about the impending '2027 problem' that could affect their compliance and financial reporting.

ProShip Inc., a leader in global asset management solutions, including fixed asset and lease management, has been diligently tracking the progress of companies in their readiness for these new standards. Their recent survey targeted accounting personnel to gain insights into the current state of compliance and the practical challenges faced.

Survey Overview

Conducted from March 17 to March 19, 2026, the survey included responses from 1,014 accounting professionals employed at either publicly listed corporations or private firms with significant capital or debt. The findings revealed stark delays in the transition process, particularly regarding the identification of leases and the determination of lease duration—issues that many companies had underestimated.

Over half of the respondents reported that they were still engaged in the early phases of preparation, specifically contract review and impact analysis. With approximately one year remaining until compliance is mandatory, many firms have yet to enter into the system implementation phase, which is critically needed to transition successfully to the new standards.

Preparation Phases Revealed

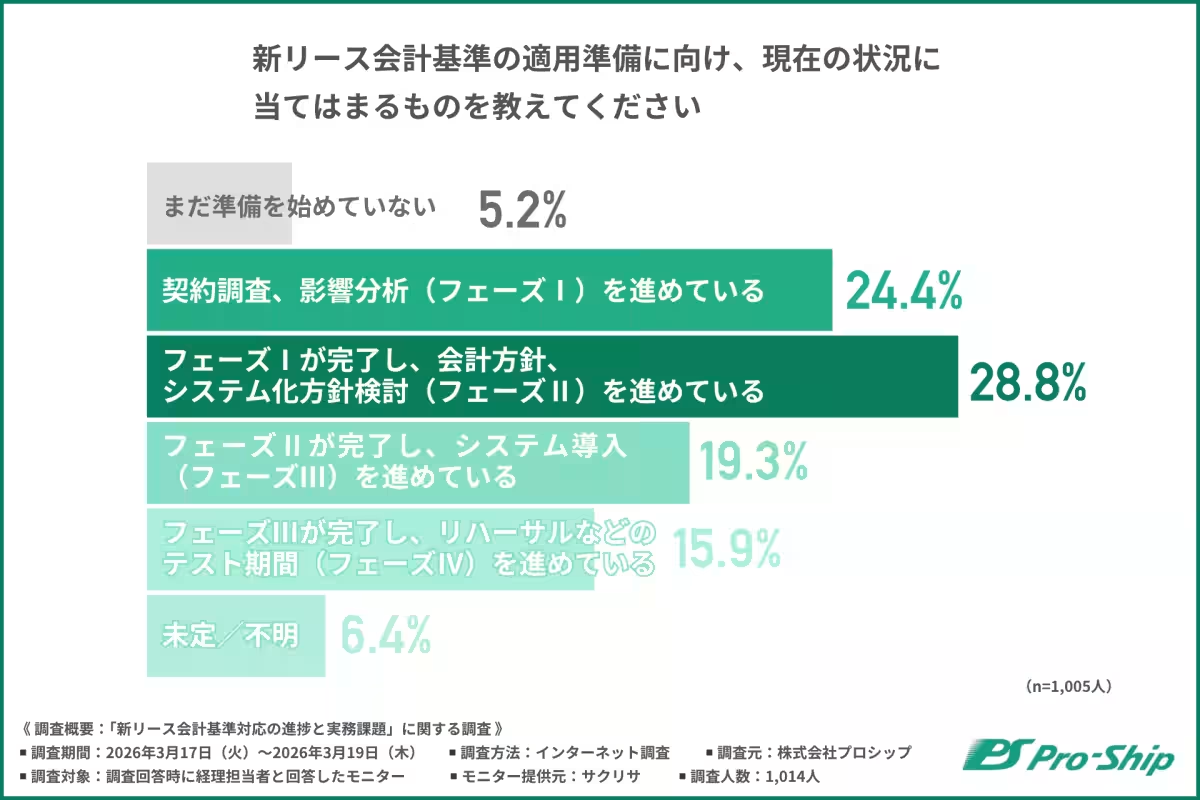

The survey categorizes the current status of preparation as follows:

- - Not started: 5.2%

- - Phase I (Contract review, impact analysis): 24.4%

- - Phase II (Policy review, system planning): 28.8%

- - Phase III (System implementation): 19.3%

- - Phase IV (Testing and rehearsal): 15.9%

- - Uncertain/Unknown: 6.4%

A significant takeaway from the survey is that over 50% of companies remain stuck in the first two phases of preparation, highlighting the complex nature of the requirements defined by the new lease accounting standards. Cross-departmental collaboration is essential for collecting comprehensive contract information, and many firms are grappling with these extensive demands.

Challenges in Identifying Commitments

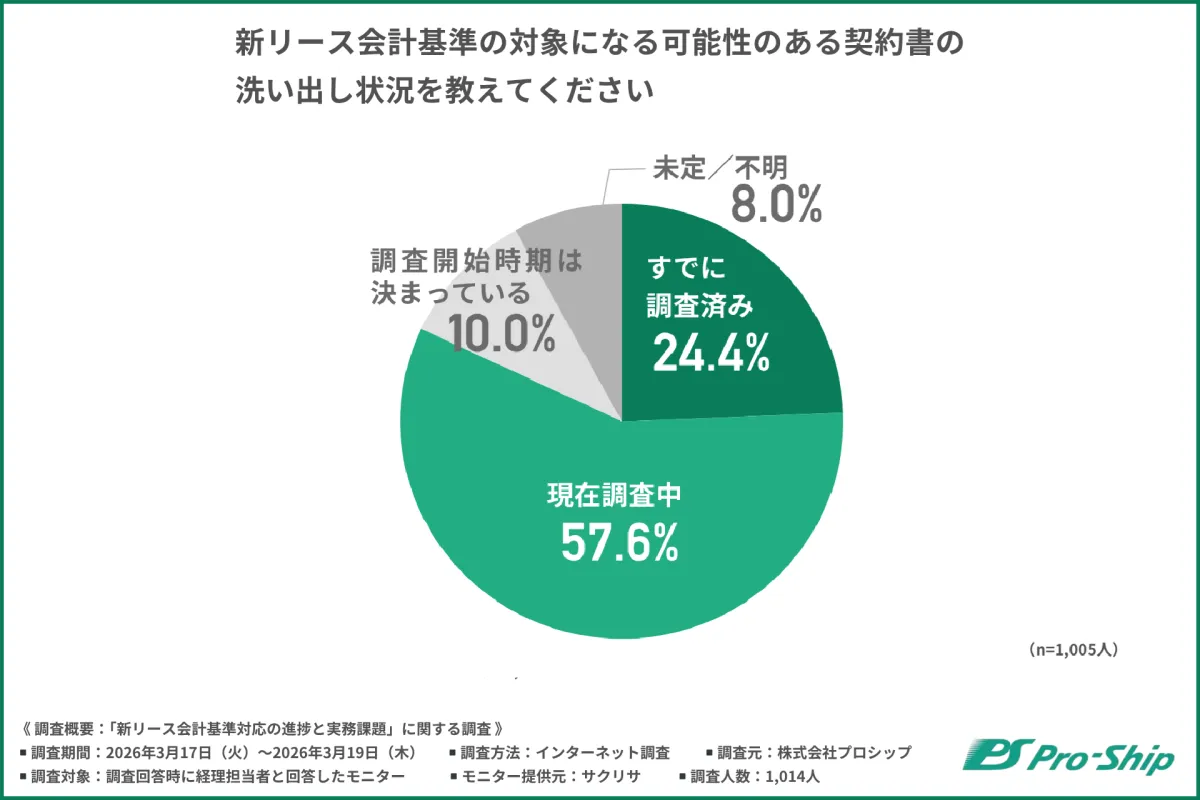

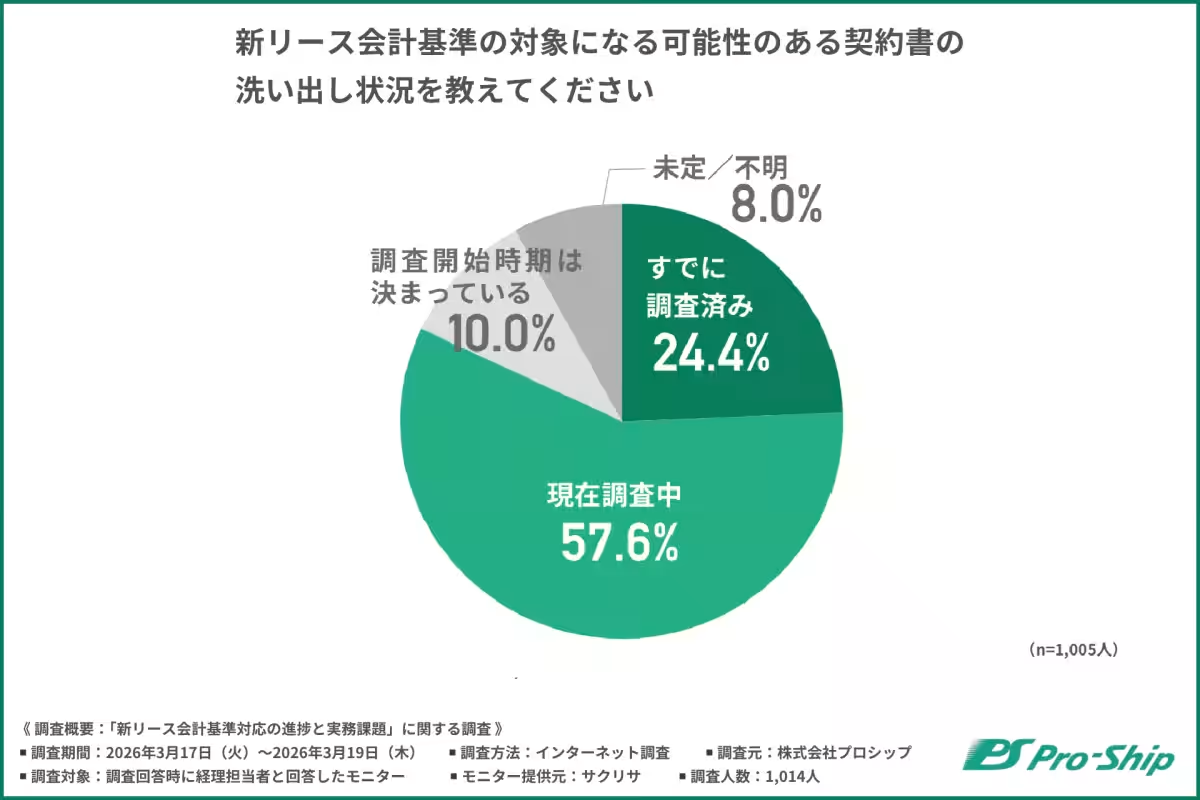

When asked about the progress in identifying contracts potentially subject to the new lease standards, the results indicated that while 24.4% of companies had completed their analysis, a staggering 57.6% were still in progress. This suggests that identifying contracts is taking longer than anticipated, contributing to the growing awareness of what experts refer to as the '2027 problem'.

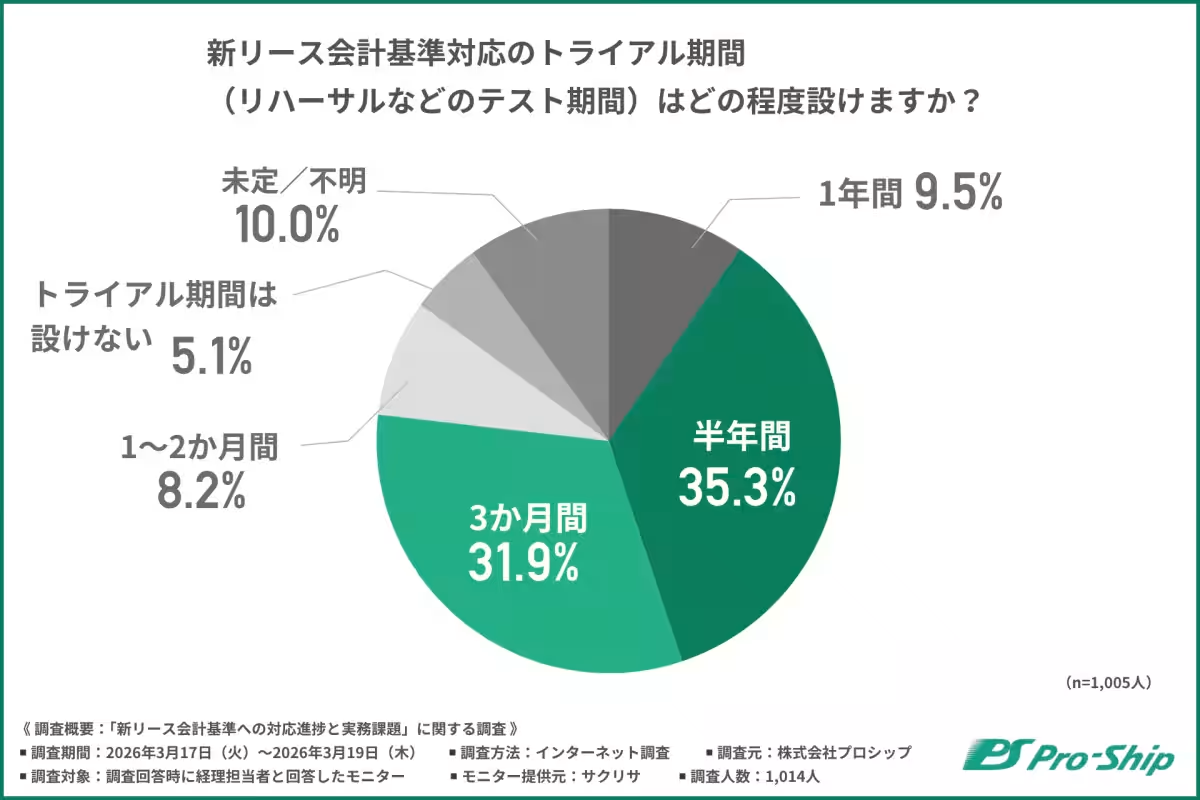

Given that ample time is needed for testing and rehearsal—estimated at three to six months prior to the rollout—companies are facing limited windows for a smooth transition. Firms are urged to accelerate their efforts to catch up with their peers who are successfully advancing in their compliance preparations.

Key Roadblocks Identified

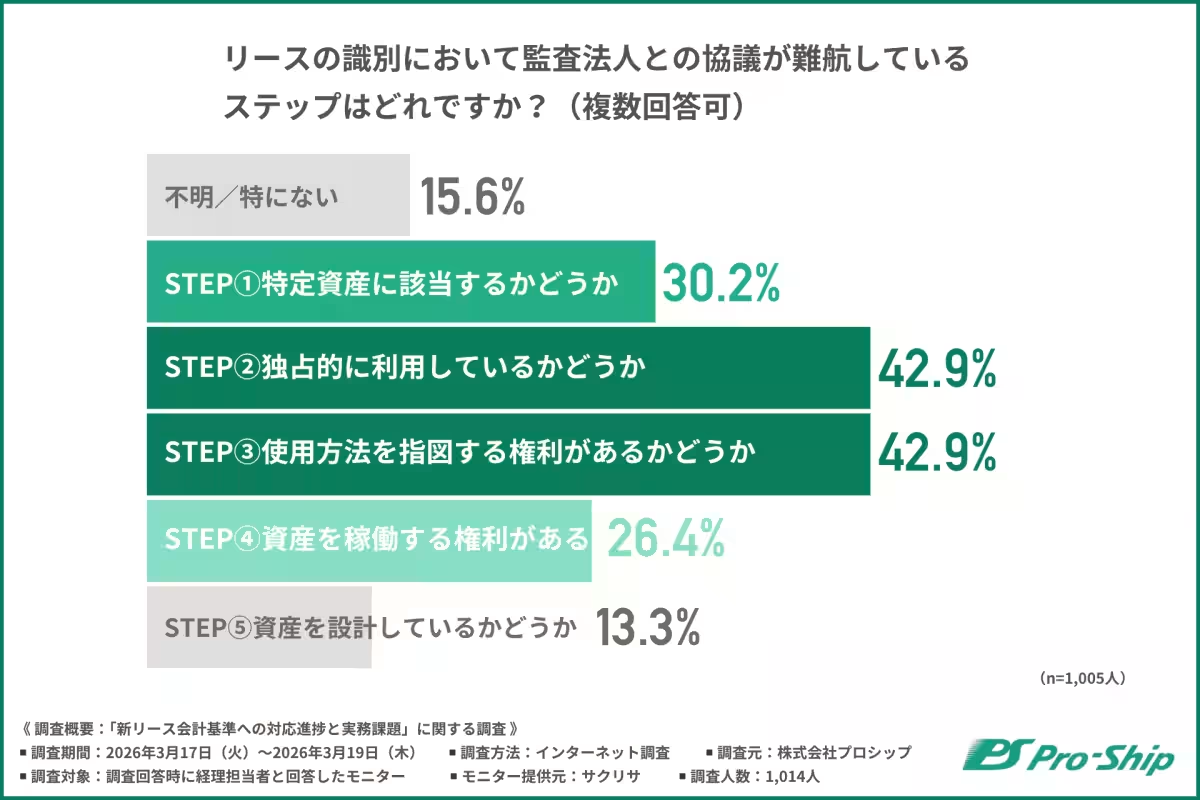

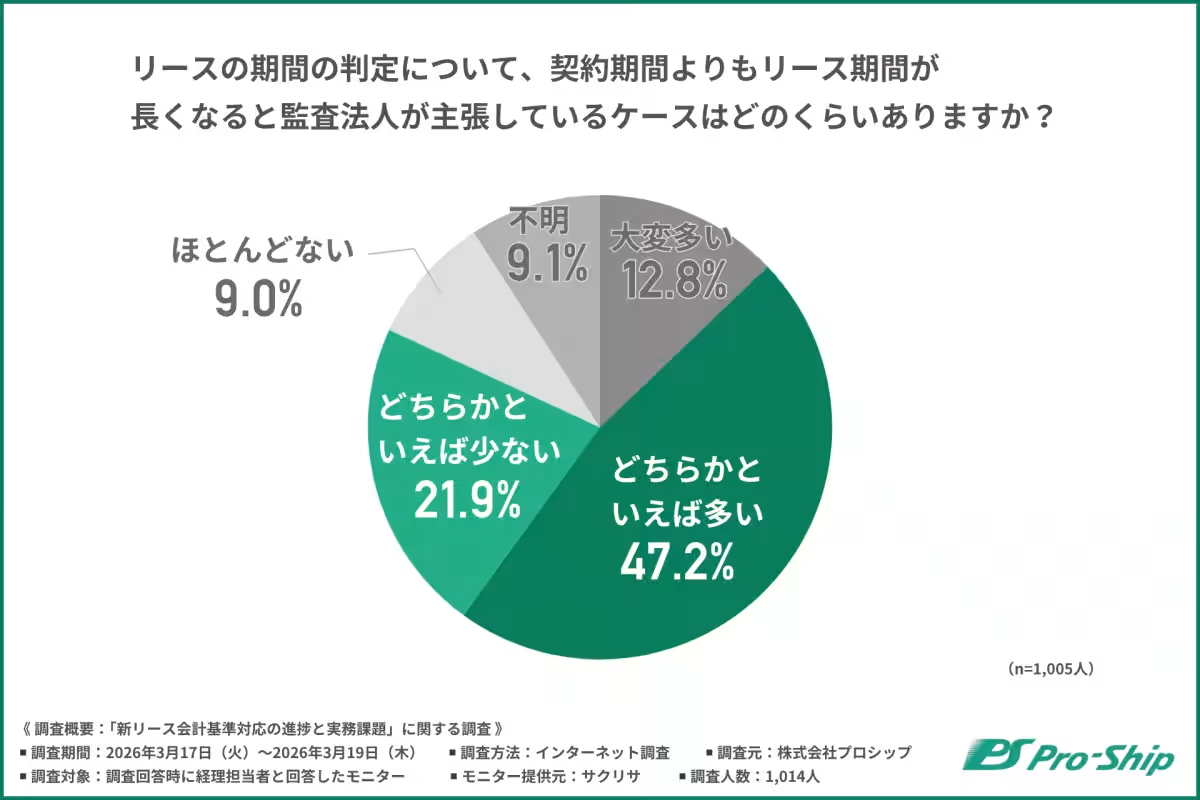

Major roadblocks include discussions with auditors regarding the interpretation of lease terms, including 'exclusive use' and 'control over how an asset is used.' The ambiguity surrounding these criteria often leads to prolonged negotiations, delaying essential decisions. As these interpretations become increasingly critical under the new standards, companies must proactively engage with their auditors to align on their contract interpretations.

On another front, many firms have also voiced concerns about the rising estimates for what constitutes 'lease liabilities' and 'right-of-use assets'. Approximately 60% of survey respondents expressed that auditors have cited instances of extending lease periods due to options to renew, which many companies currently overlook.

Ideal versus Reality

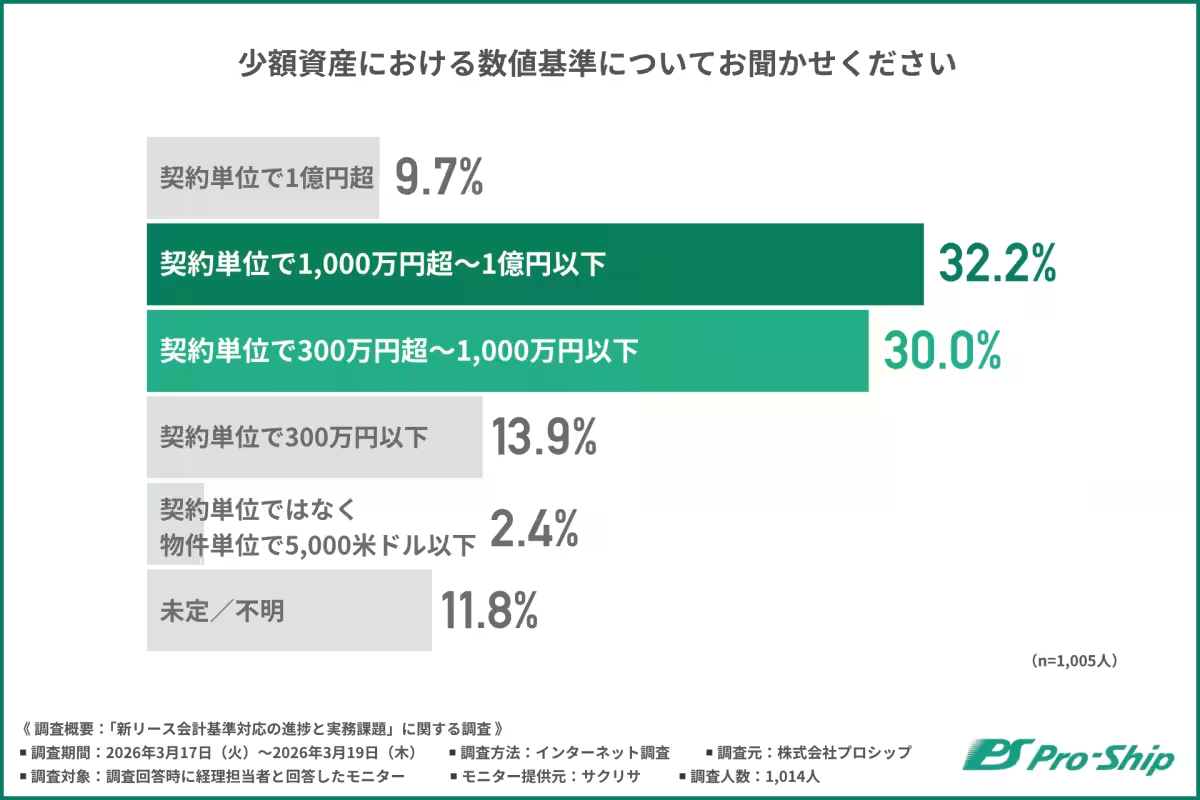

As part of the evaluation of small asset criteria under the new regulations, around 60% of respondents indicated a preference for thresholds that significantly surpass existing standards. This disconnect illustrates the tension between a desire for reduced recording burdens and the requirements of compliance under transparency mandates.

Heavy Administrative Burdens Ahead

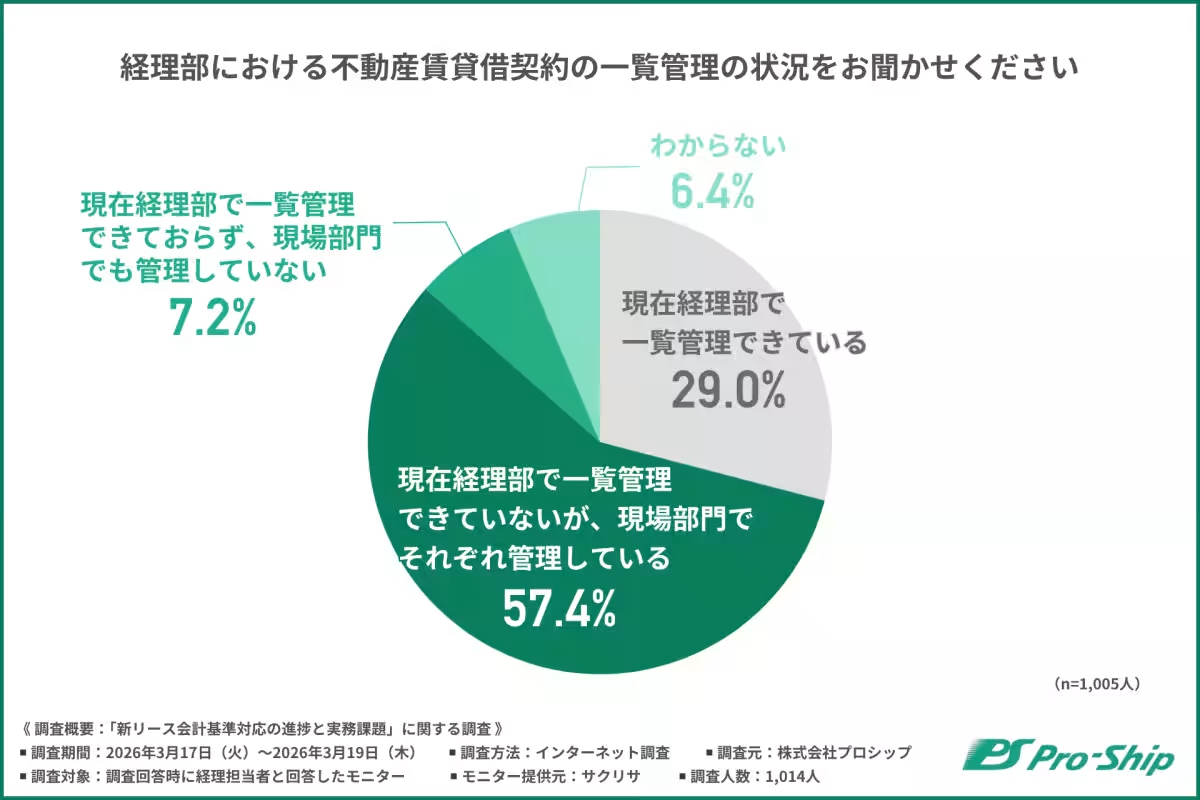

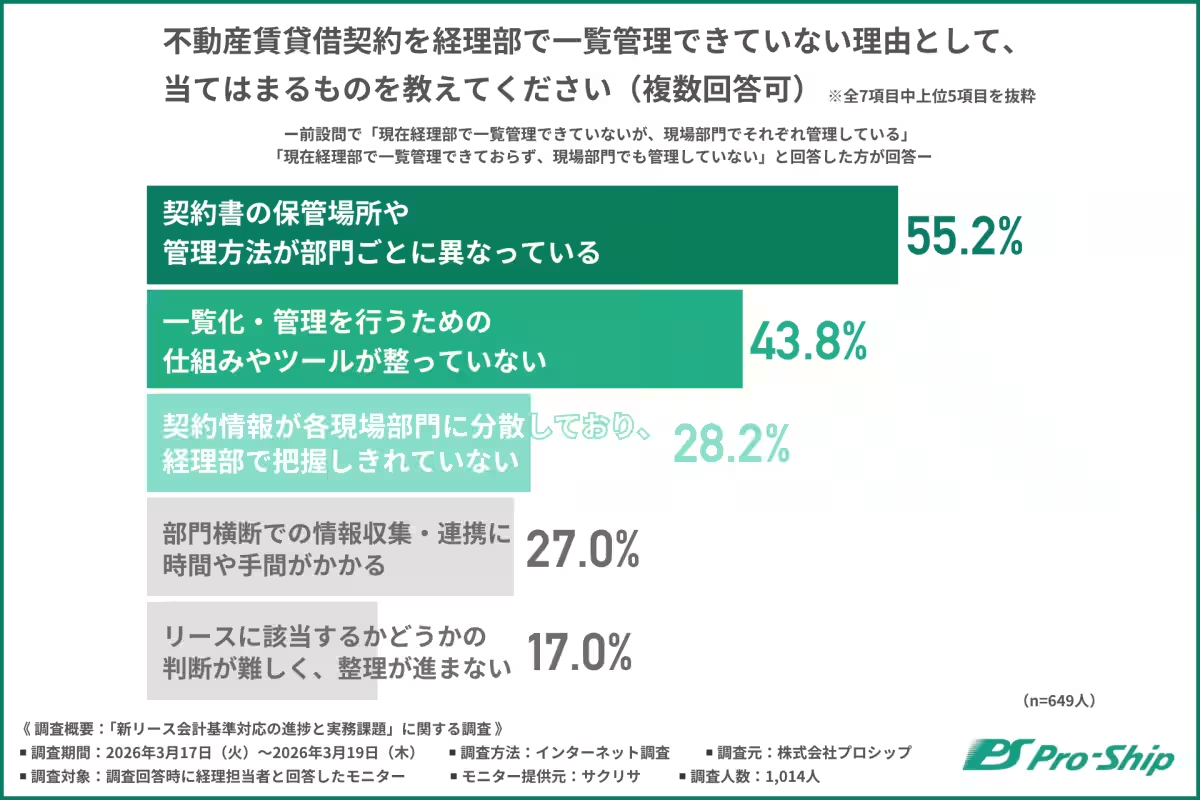

As companies prepare for the new standards, they will face an increase in the volume of asset management tasks due to the inclusion of real estate leases. Many accounting departments struggle to manage contract data effectively, leading to potential bottlenecks as the lease accounting shift progresses. In fact, less than 30% of companies reported centralized management of their real estate contracts.

Conclusion

In summary, companies are urged to act swiftly as the countdown to the new lease accounting standards begins. The survey results lay bare the urgency for organizations to refine their processes, establish clear timelines, and ensure comprehensive management of lease contracts. Initiating collaboration with service providers like ProShip, who specialize in this area, could provide crucial support in alleviating the burdens associated with these transformations. Preparation for the new standards isn't just about compliance; it's about strategic planning to mitigate risks and streamline accounting practices moving forward.

Topics Business Technology)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.