Is Choosing a Low Monthly Payment Car Loan Really Worth It? Understanding the Risks of Residual Value Loans

Understanding the Risks of Residual Value Loans in Car Purchases

In recent years, residual value loans, often touted for their low monthly payments, have gained popularity among car buyers. However, a new survey conducted by Yuichi Sugawara, a tax accountant with over 1.53 million YouTube subscribers, sheds light on a concerning reality. The survey, which targeted 180 individuals across Japan who purchased cars using residual value loans, reveals that a significant majority lack a comprehensive understanding of the loan's mechanisms and risks.

Survey Overview

- - Survey Period: February 16-17, 2026

- - Method: Online survey

- - Participants: 180 individuals aged between 18 and 69 who utilized residual value loans to purchase cars

- - Conducted by: Freeasy

- - Attribution: When utilizing this survey's results, please refer to "Yuichi Sugawara's Survey."

Key Findings

The survey uncovered several critical insights:

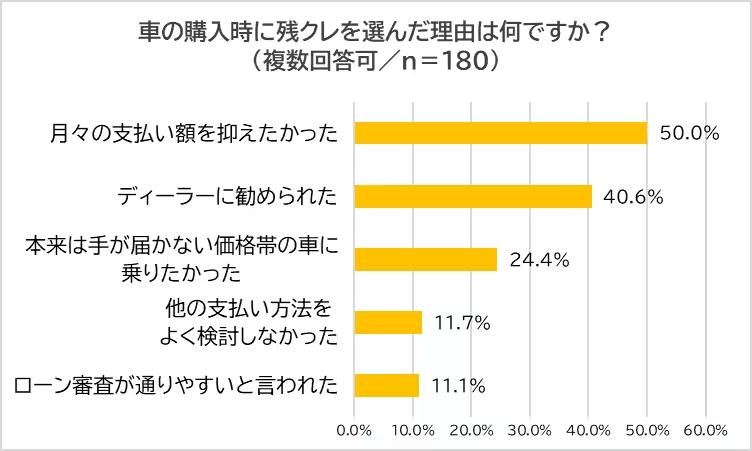

- - The primary reason for selecting residual value loans was the allure of low monthly payments (50% of respondents), followed by being encouraged by dealers (over 40%).

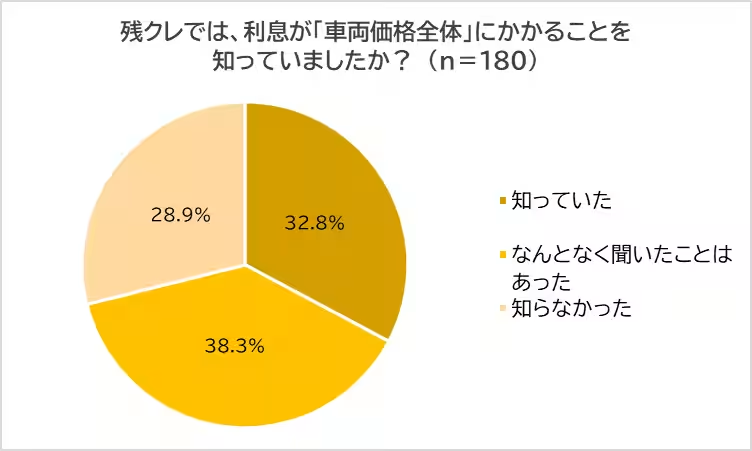

- - Only about 30% of participants fully grasped how interest applies to the entire vehicle price, indicating a significant lack of understanding among users.

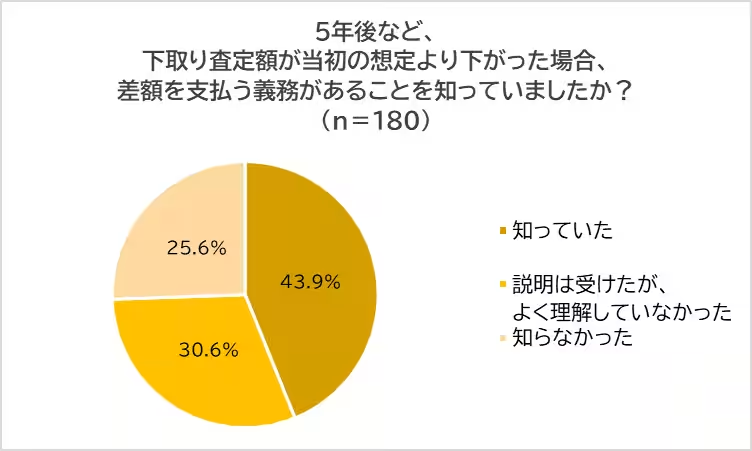

- - Over 50% of respondents were unaware of the risks associated with potential disparity in the buyback price at the loan's end.

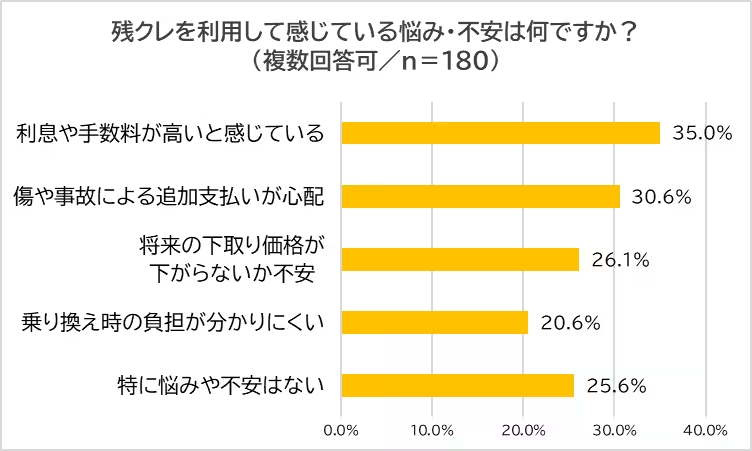

- - Many users later reported feelings of anxiety related to future financial burdens, including high interest and potential additional costs from wear and tear.

Understanding the Attraction

Why do consumers gravitate towards residual value loans? The appeal often lies in the lower immediate financial burden presented by monthly payments. This method allows buyers to access higher-priced vehicles than they might otherwise afford. However, as the data reveal, this decision is often made without adequate understanding of the underlying risks.

The Mechanics of Residual Value Loans

Residual value loans function by predicting the vehicle’s future buyback price, allowing borrowers to finance only the amount exceeding that estimate. For example, purchasing a vehicle priced at 8 million yen with a predicted residual value of 5 million yen leads to financing only the remaining 3 million yen. This arrangement reduces monthly payments to around 50,000 yen compared to traditional loans.

Hidden Costs of Residual Value Loans

1. Interest Calculations: One major misconception is that interest is calculated solely on the financed amount. In reality, borrowers pay interest on the total vehicle price, which can lead to significant long-term costs, especially when projected values fall short.

2. Fluctuating Resale Values: There's an inherent risk that the actual resale value of the vehicle at the end of the loan term might decline significantly, resulting in unforeseen payment obligations. Such scenarios can lead to additional financial strain, creating a cycle of refinancing at higher rates.

3. Pressure on Switching Vehicles: With many buyers eager to upgrade, the end of a loan term can lead to stress if the vehicle's value depreciates more than anticipated. Issues like minor damage or a previously unrepaired accident can also trigger additional costs, compounding the financial burden.

4. Dealer Incentives: The profitability of residual value loans for dealerships often leads to one-sided sales practices. Customers may find themselves pushed towards these loans without a thorough disclosure of potential downsides.

Looking Ahead: A Cautious Approach

While residual value loans can provide lower monthly payments, the drawbacks—including high interest rates and unpredictable resale values—mean that they may not be the best option for all buyers. Moreover, a new trend in residential property purchases has emerged where similar loans are being promoted, though the stakes involved are typically higher. Family-oriented individuals may need to exercise even greater caution with such financial commitments.

Conclusion

In sum, while residual value loans appear attractive due to their low monthly payments, they carry hidden risks that can result in significant financial burdens in the future. Buyers are urged to consider not just the short-term savings but the long-term implications of their financial decisions. The best approach is to fully understand the total costs and potential risks involved, rather than being lured in by seemingly manageable monthly payments. Taking the time to explore all options and acknowledging the complexities of financing can ultimately lead to better, more informed purchasing decisions.

About Yuichi Sugawara

Born in 1975 in Mie Prefecture and now residing in Tokyo, Yuichi Sugawara is a specialist in tax savings and funding strategies. His YouTube channel, launched in December 2022, has surpassed 1.53 million subscribers, becoming highly influential in the finance sector. He is also a top-ranking blogger and speaker, having conducted over 1,000 seminars for leading companies. Sugawara's publications have achieved bestseller status, reflecting his expertise in financial education.

Topics Consumer Products & Retail)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.