Understanding the Experiences of Debt: Voices from Ten Individuals Who Faced Financial Crisis

Understanding the Experiences of Debt

In recent years, the rise in individuals facing multiple debts has often made headlines. Amidst this troubling trend, the financial information media, Sustainable Finance Lab (operated by Elevista Inc.), conducted individual interviews with ten men and women who have experienced credit card delinquencies, consumer loans, and debt restructuring between May 6 and May 14, 2026. The results revealed a surprising consensus: nearly all interviewees initially felt unable to consult anyone about their debts.

The Weight of Secrecy

The sentiment shared among the participants was that confiding in someone about their financial troubles felt daunting. For many, the fear of judgment or the desire to spare loved ones from worry led them to shoulder the burden alone. C. Y., a 31-year-old IT professional, expressed a common worry: "Discussing money issues made me feel like I had to hide it until I died."

Y. H., a 30-year-old accountant, hesitated to seek help even online, fearing that acquaintances might discover his debt status through his social media posts. This demonstrates the strong stigma attached to financial hardship, making people reluctant to share their struggles even in discreet forums.

Conversely, those who eventually confided in family members often found unexpected support. Y. R., a 24-year-old housewife, recounted how she delayed sharing her debts with her husband, fearing his reaction. To her surprise, he was understanding, highlighting the misconception that revealing such issues would lead to disastrous consequences. Everyone expressed relief at finding that their worst fears concerning reactions did not materialize. Many found comfort in sharing their stories with friends, who provided a willing ear without delving too deeply into personal details.

The Pathway to Solutions

Some interviewees who sought advice from financial experts shared an enlightening perspective: consulting did not signal the end but rather the beginning of a solution. O. K., a 32-year-old from a pharmaceutical company, reflected on how misinformation regarding debt restructuring, such as fears of entering a 'blacklist,' delayed his consultation. He stated, "If I had known the benefits of seeking help, I would have acted sooner."

I. K., a 34-year-old manufacturing professional, saw a significant reduction in his monthly repayments after consulting a lawyer. "With their support, my payments dropped from about 50,000 yen to 40,000 yen a month," he explained, emphasizing the peace of mind that comes from expert intervention.

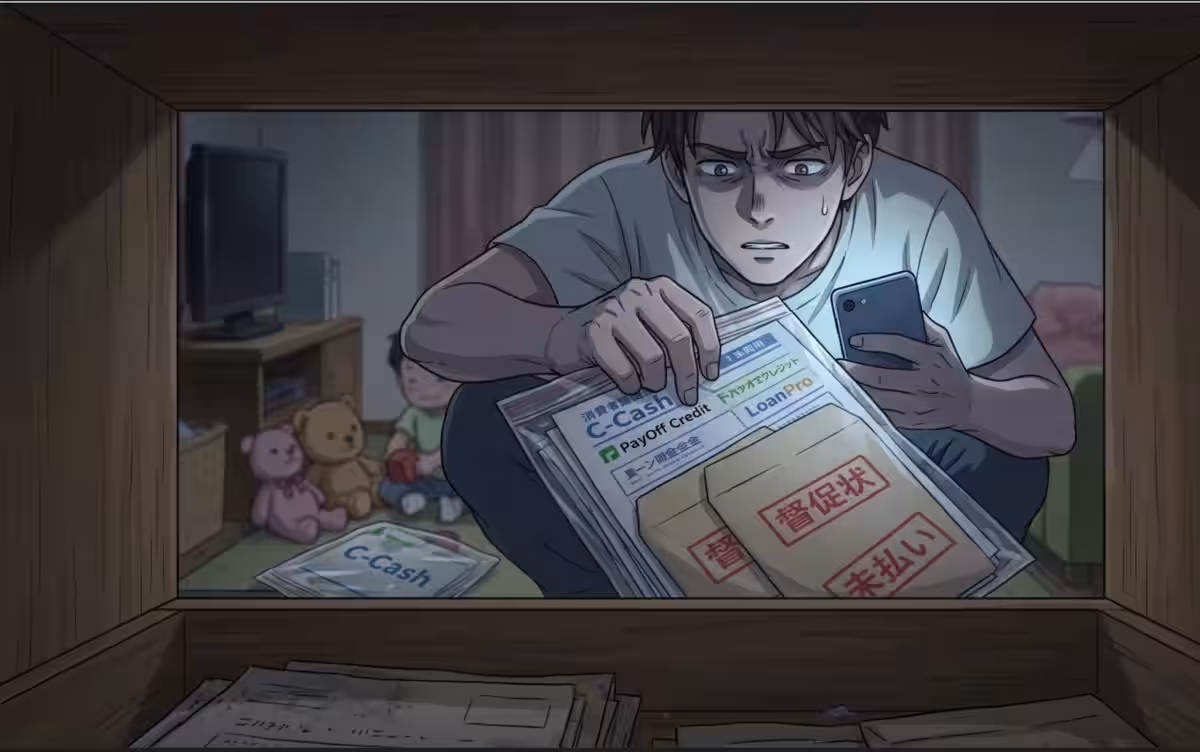

Common Missteps and Barriers

For most, the journey to tackling their debts began with searching online for terms such as "What happens if I default?" or "What does forced cancellation mean?" Unfortunately, discovering effective solutions like 'debt restructuring' or 'personal bankruptcy' requires knowledge that many lack. Many ended up overwhelmed by advertisements from law firms rather than accessing impartial information that could guide their decisions. Y. H. felt frustrated by how often he encountered promotional material instead of useful advice during his research.

Some participants even mentioned the support they found on platforms like Yahoo Chiebukuro, where the shared experiences of others in similar circumstances provided them with the comfort of knowing they were not alone.

The Impact of Life Events

Throughout the interviews, several participants described how milestones such as marriage, childbirth, or career transitions precipitated their financial challenges. C. Y. found himself depleting savings during a transition period while paying for childcare costs, which resulted in reaching credit limits. As he recounted, "Even though I wasn't frivolously spending, increased costs from housing, cars, and children left me feeling overwhelmed."

Similarly, others highlighted how unexpected changes in income during maternity leave led them to unwittingly accumulate debt. Awareness of spending can prevent individuals from reaching their breaking points.

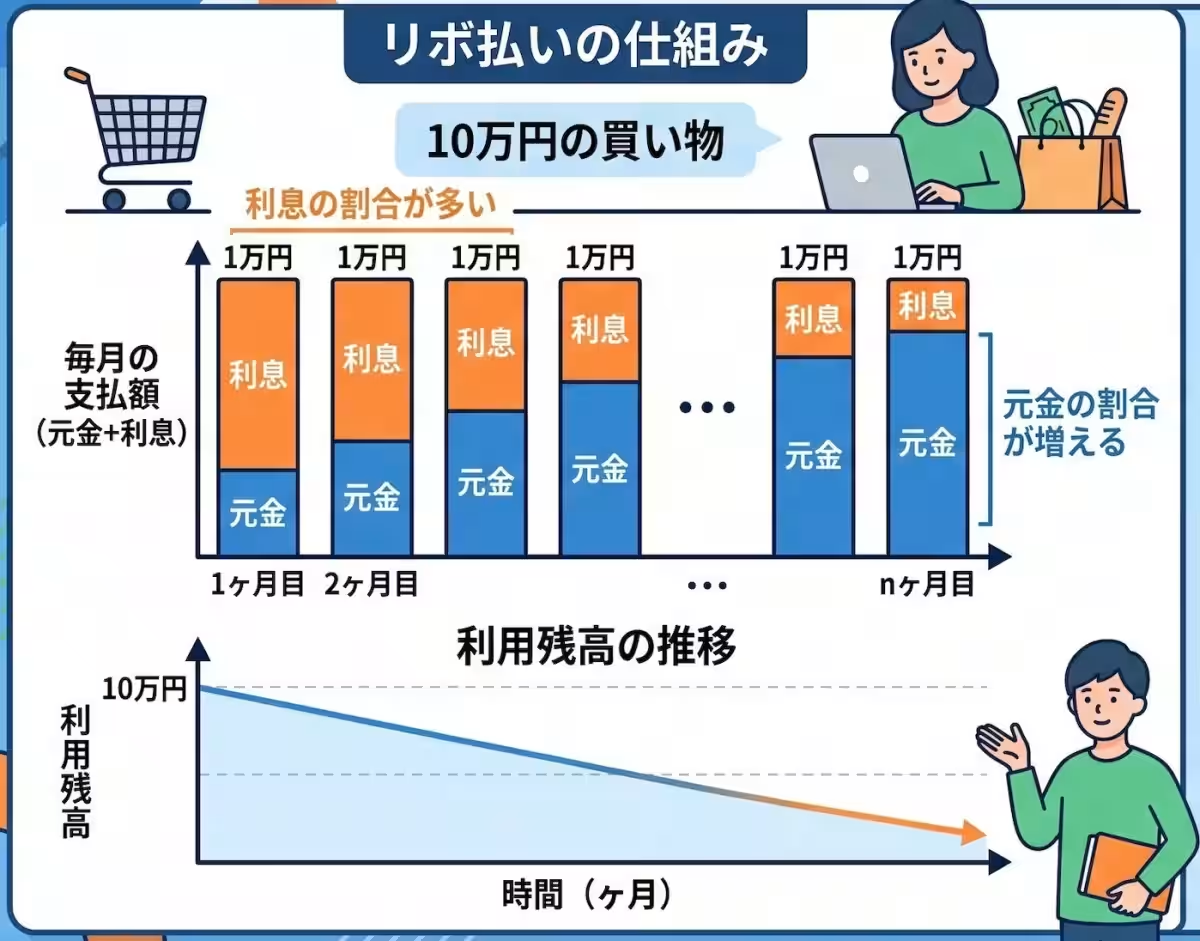

The Illusion of Revolving Credit

Participants were also wary of revolving credit payments, which they initially viewed as a lifeline. Many expressed regret over opting for this method due to misconceptions regarding low monthly payments, only to find themselves trapped in a cycle of increasing debt. Y. R. firmly stated, "Revolving payments made me feel like I was handling my debts, but they only worsened my situation."

Conclusion

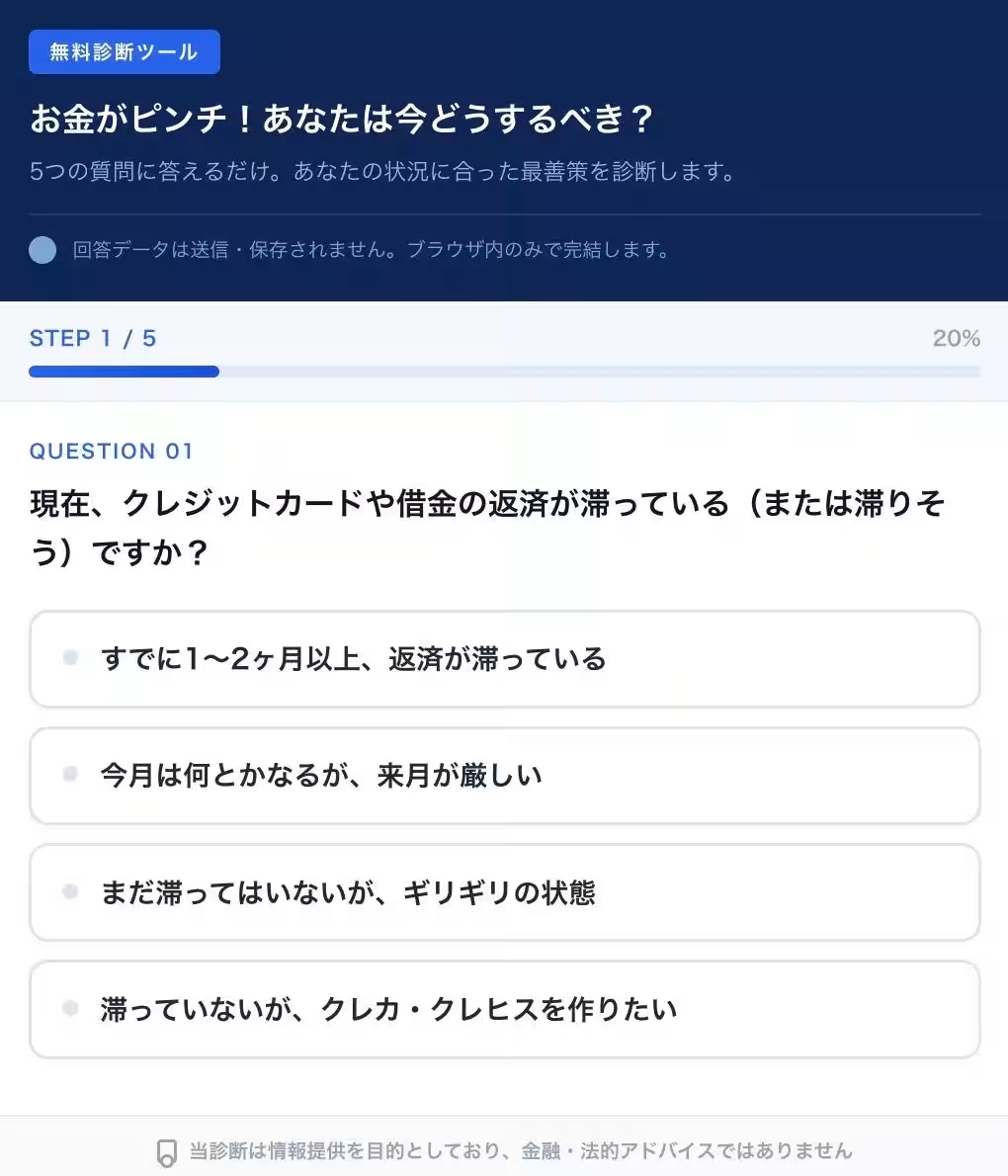

The findings from this survey illustrate a critical need for awareness about debt management solutions and the importance of open discussions regarding financial struggles. The stigma of debt often hinders individuals from seeking help, and misinformation can prolong financial distress. By acknowledging these barriers, sustainable solutions can be developed, allowing more individuals to confidently navigate their financial difficulties. The Sustainable Finance Lab aims to address these issues and provide a free diagnostic tool for those facing similar challenges, helping them identify appropriate options and resources. Visit the diagnostic tool here to make a step towards overcoming financial hardships.

Topics Financial Services & Investing)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.