Top 5 Financial Questions to Consider in End-of-Life Planning Revealed!

Understanding Financial Concerns in End-of-Life Planning

In recent years, end-of-life planning, or "shukatsu" in Japan, has gained increasing importance due to longer average lifespans and the rise of nuclear families. Notably, a survey conducted by 400F, a prominent financial consulting service operating 'Okane-Co', found that over half of the participants are uncertain about the financial aspects of end-of-life planning. This has brought to light several common financial questions that many individuals struggle to answer.

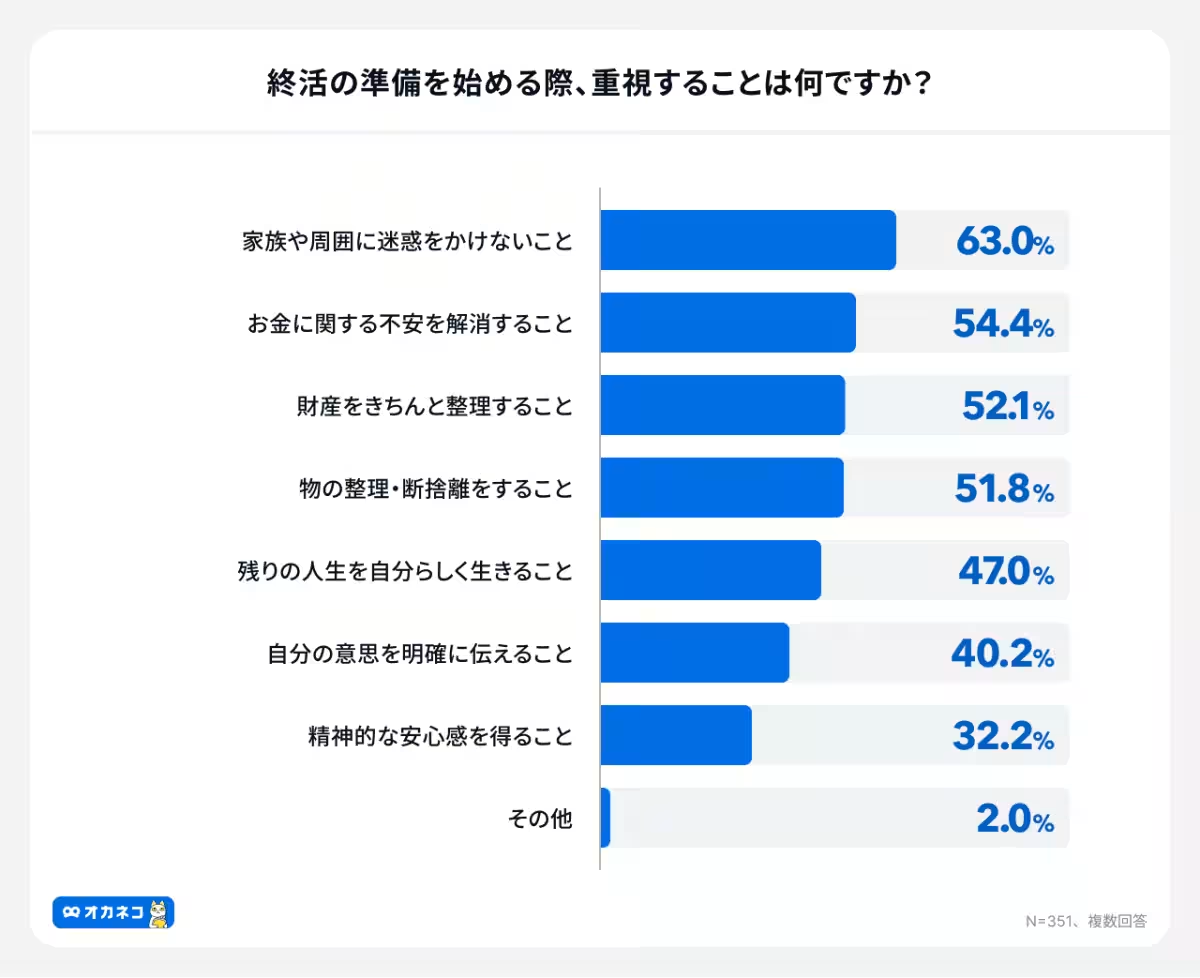

According to the survey, conducted among 351 users of 'Okane-Co', the top reasons for prioritizing end-of-life planning include avoiding burdening loved ones (63.0%) and alleviating financial concerns (54.4%). This indicates a strong desire among individuals to lessen both emotional and financial stress on their families as they contemplate the end of their lives.

The Top 5 Financial Questions in End-of-Life Planning

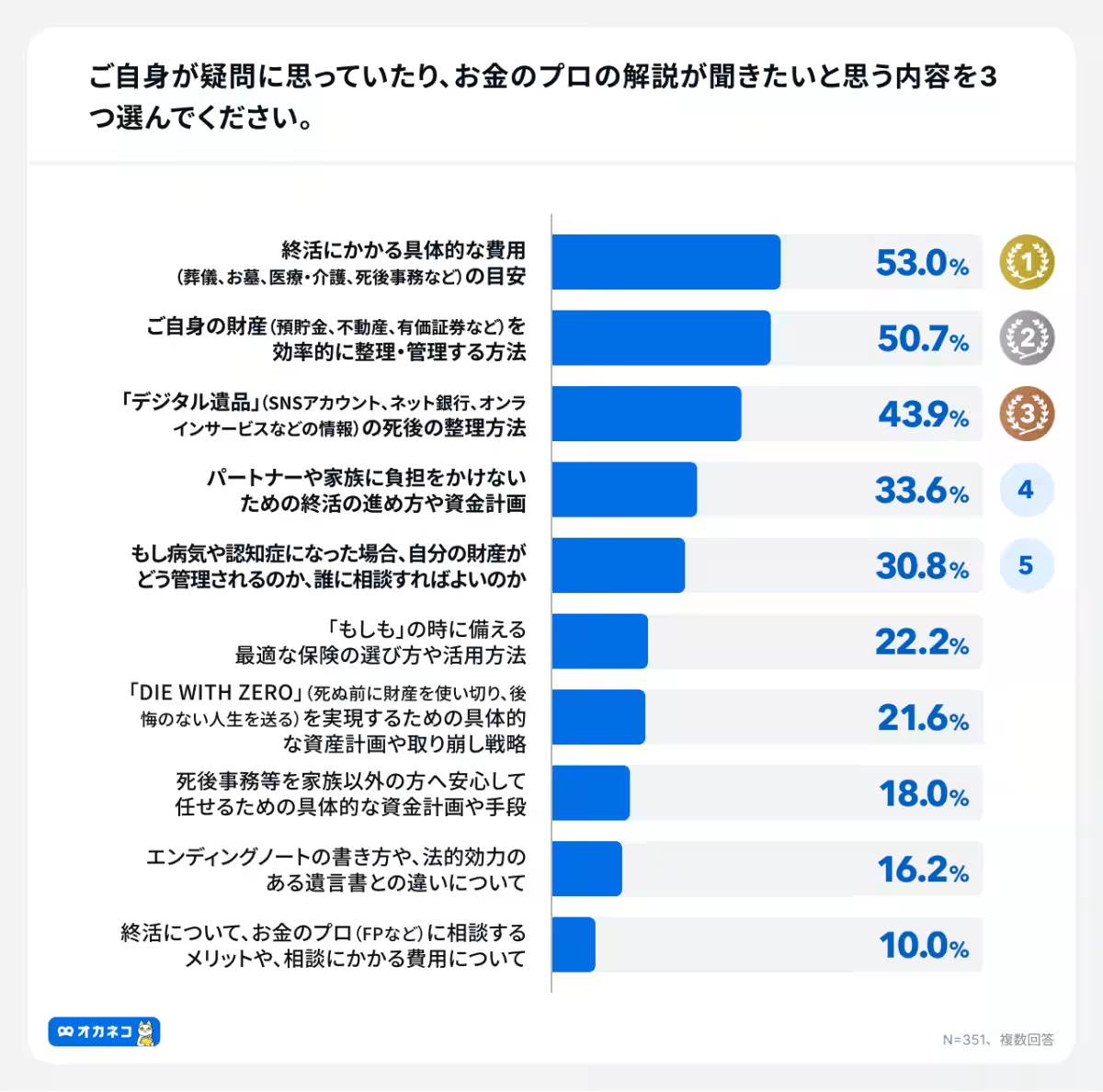

End-of-life planning encompasses a plethora of financial knowledge and legal procedures that can often feel overwhelming. Recognizing this complexity, the survey aimed to uncover the pressing financial questions users have about this phase of life. Participants were invited to rank their financial concerns, leading to the identification of the top five financial uncertainties:

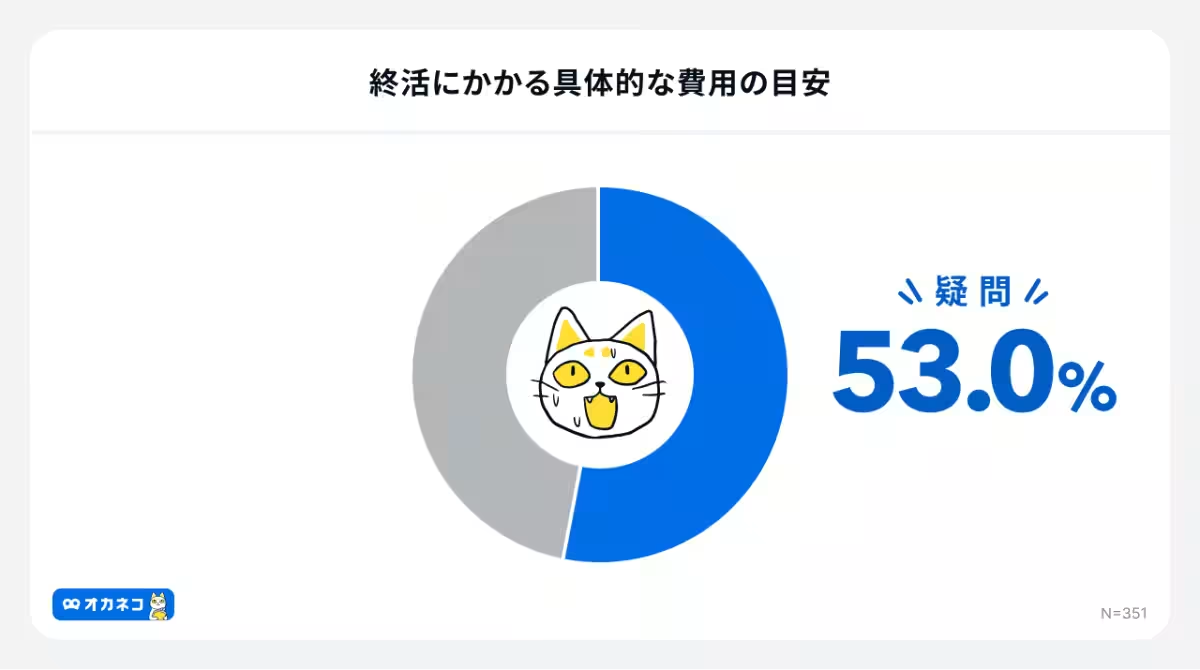

1. Estimation of Costs Related to End-of-Life Matters (53.0%) - The most common inquiry revolved around the specific costs associated with end-of-life planning, such as funeral expenses, burial costs, healthcare, caregiving, and post-death procedures. A realistic estimate for funeral expenses is approximately 1 to 2 million yen, while burial and memorial services could range from 1 to 3 million yen. Healthcare and caregiving costs can vary greatly, with home care averaging around 50,000 yen per month and institutional care potentially costing between 100,000 to 150,000 yen monthly. Such financial burdens necessitate thoughtful planning and estimation of individual needs.

2. Efficient Ways to Organize and Manage One’s Assets (50.7%) - Many individuals expressed confusion regarding how to start organizing their assets. A sensible first step is creating an asset inventory, listing all bank accounts, securities, real estate, and debts. This process can aid in visualizing one’s financial situation and help manage resources effectively. Additionally, eliminating dormant accounts and reviewing insurance policies can optimize financial assets.

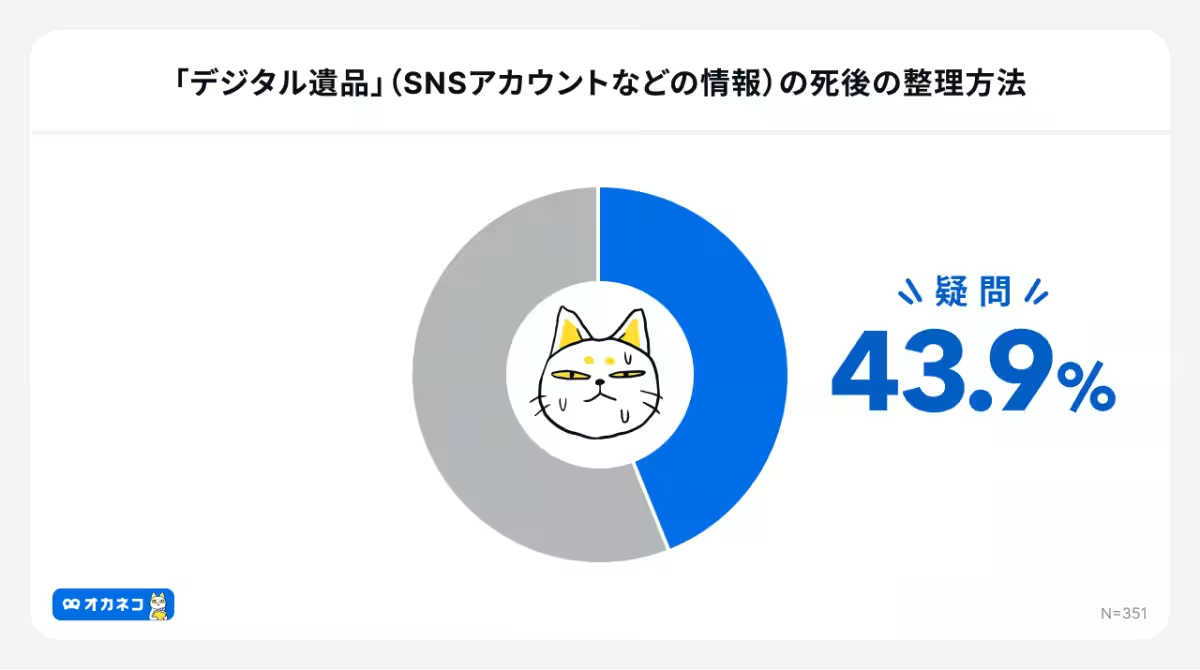

3. Organization of Digital Legacy (43.9%) - In today's digital age, managing digital legacies has become crucial in end-of-life planning. Individuals should compile a list of all online accounts along with their access information, including social media, online banking, and subscriptions. Utilizing a digital asset management service or an end-of-life planning notebook can support the organization of these digital assets, allowing trusted individuals to manage them in the event of one's passing.

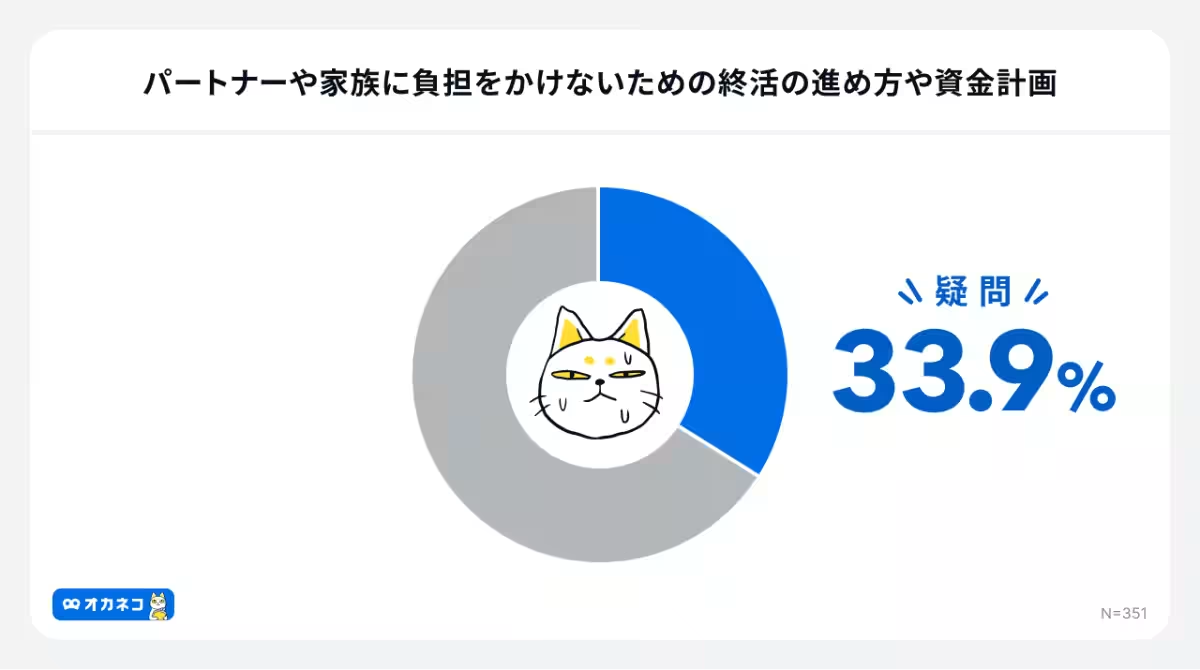

4. How to Proceed with End-of-Life Planning to Avoid Burdens on Family (33.6%) - For those with partners or family, it is vital to share one's financial situation openly, creating a transparent record of assets and liabilities. Reviewing life insurance coverage to ensure it supports surviving family members adequately is crucial, as is preparing for potential funeral and burial expenses well in advance.

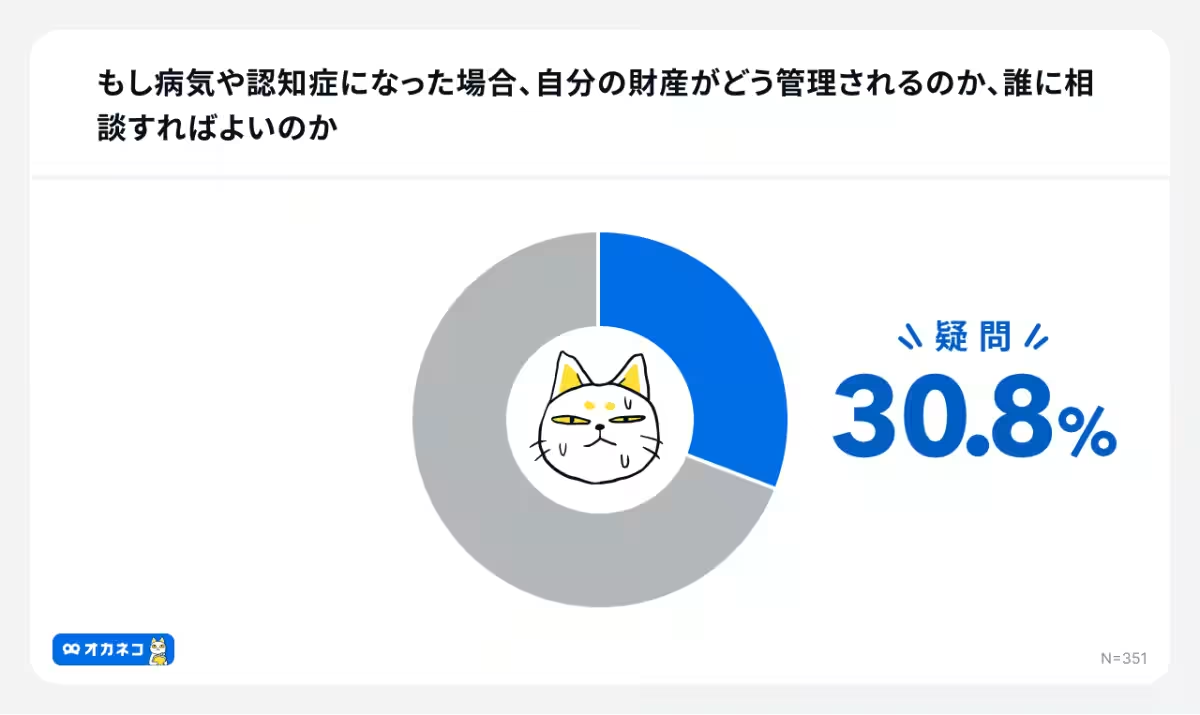

5. Managing Assets in Case of Illness or Cognitive Decline (30.8%) - The concern also extends to the possibility of losing one’s ability to communicate decisions. Establishing a family trust or a voluntary guardianship agreement can ease these worries, allowing chosen individuals to manage assets and provide care effectively without complications.

Conclusion

The survey revealed a significant level of uncertainty regarding end-of-life financial matters among users, suggesting a growing need for structured guidance in these areas. As societal structures and family dynamics evolve, so must the approaches to end-of-life planning, which should be tailored to individual lifestyles. For example, solo individuals might need support with post-death tasks while those with families might focus on minimizing financial strain on their loved ones.

To tackle these emerging complexities, 400F aims to provide personalized advice that respects individual circumstances. As part of its service, 'Okane-Co' offers a platform where users can easily consult financial professionals for tailored guidance on issues that arise during end-of-life planning. By fostering a better understanding of financial options and creating a straightforward path for beginning this essential planning, the aim is to help individuals navigate their financial futures with confidence.

- ---

Author: Daisuke Matsui, 1st Grade Financial Planning Specialist, CFP®

400F, a pioneering FinTech startup advocating for effective financial solutions.

Topics Financial Services & Investing)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.