Challenges Faced by Companies in Adapting to the New Lease Accounting Standards

Understanding the New Lease Accounting Standards

In recent developments regarding the new lease accounting standards, a thorough investigation conducted by ProShip Co., Ltd., a leading provider of asset management solutions, has brought to light the challenges faced by companies during the preparatory phases. Established in Chiyoda, Tokyo, ProShip conducted a survey targeting finance professionals to assess their readiness and concerns regarding the implementation of these standards, which were finalized last September.

Background of the Survey

The survey was executed via an online platform from May 8th to 9th in 2025, reaching a total of 1,007 finance personnel from companies that meet specific criteria, including publicly listed companies or those with substantial capital and debt levels. The purpose was to comprehend the perceived impact of the new lease accounting standards on their organizations and to identify any ongoing concerns in the adaptation process.

Key Findings and Insights

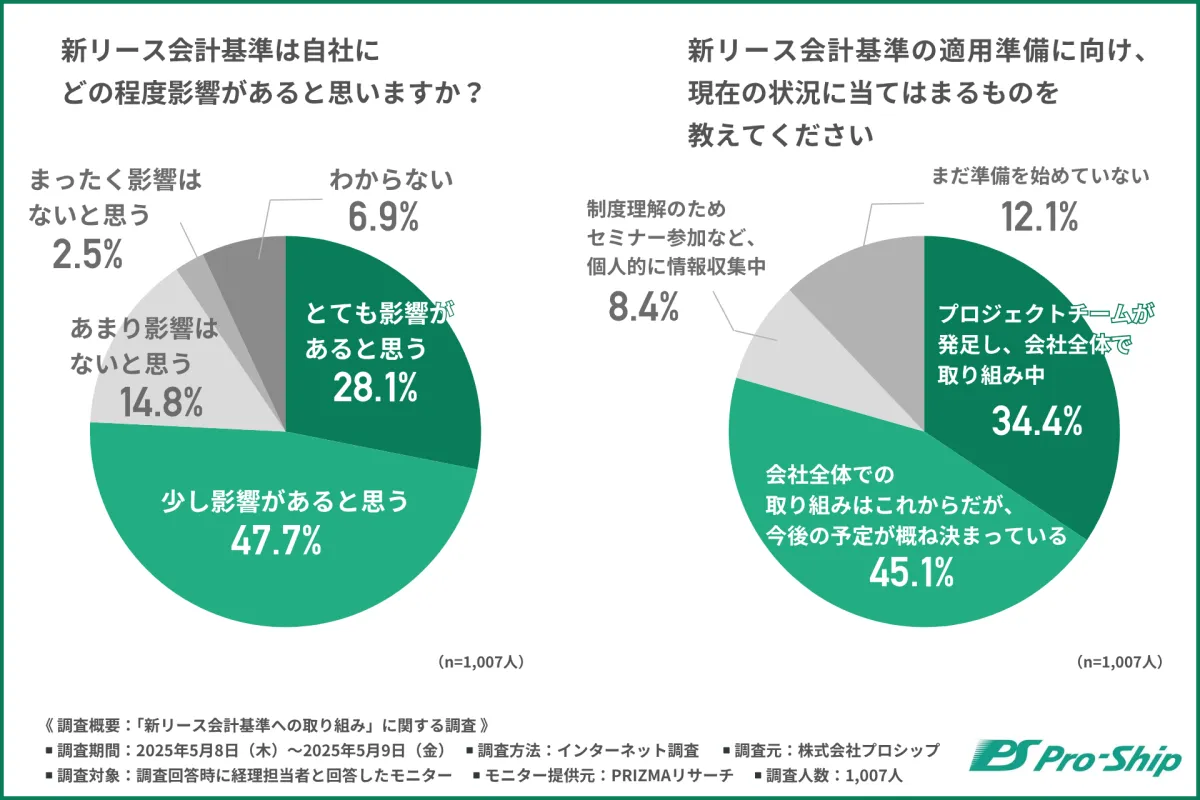

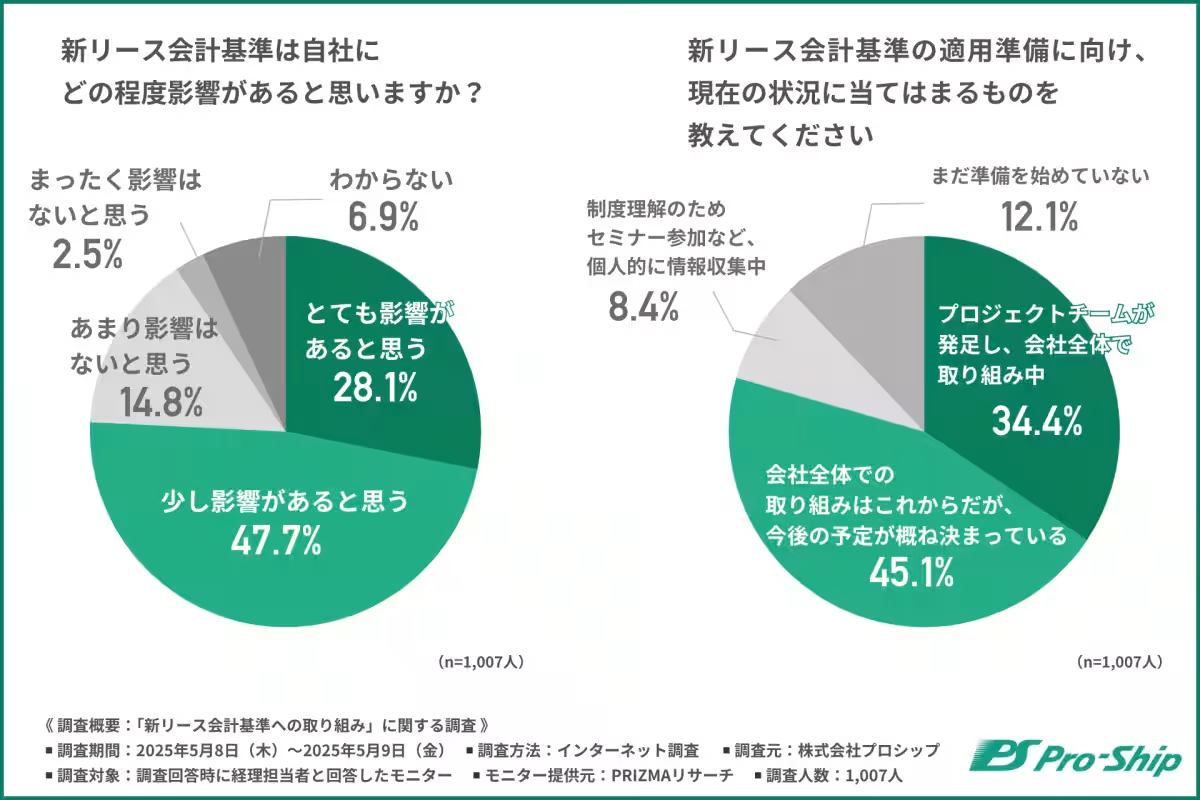

Respondents were asked how significantly they feel these new standards will impact their organizations. An overwhelming 75.8% believed there would be some level of effect, with 28.1% stating it would be substantial and 47.7% suggesting it would be somewhat significant. Conversely, some companies still feel the changes will not affect them, necessitating a swift assessment of the need for compliance measures.

As they approach the implementation date, almost 79.5% have reported entering the planning stage for compliance. Notably, 34.4% have already formed project teams dedicated to tackling this issue, while 45.1% have set plans in motion.

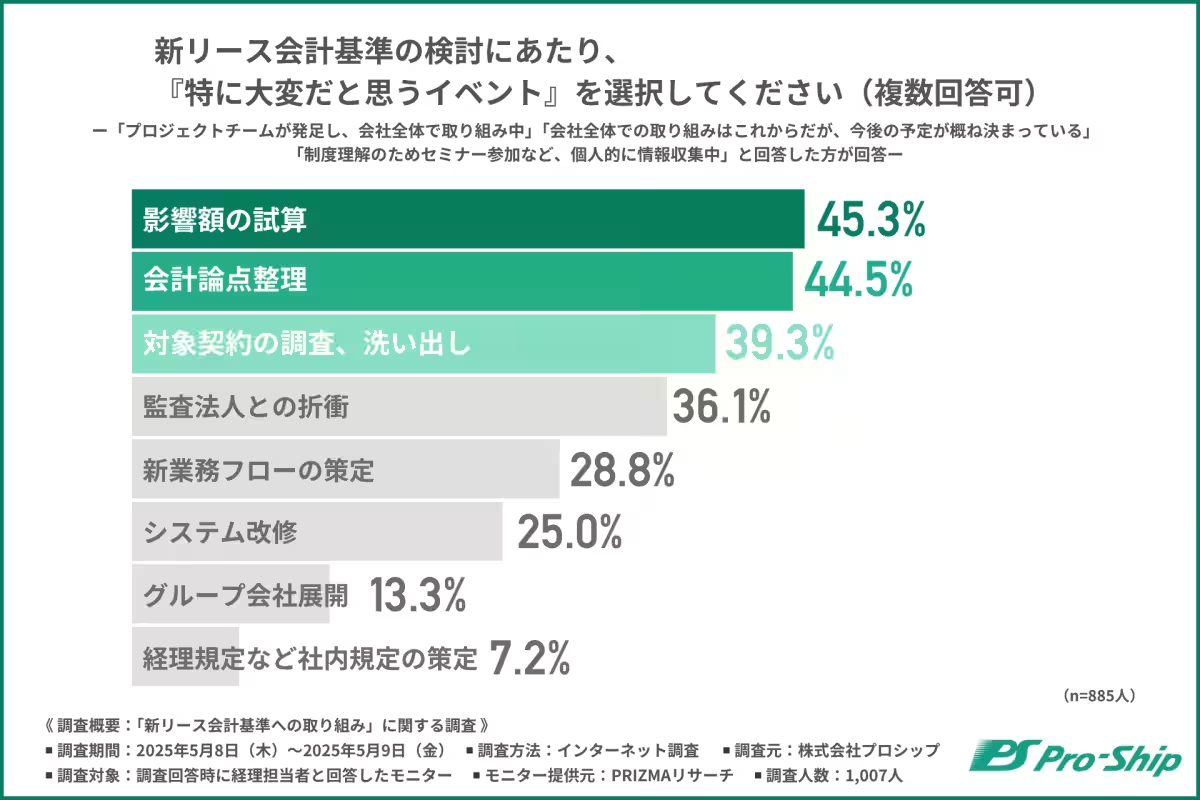

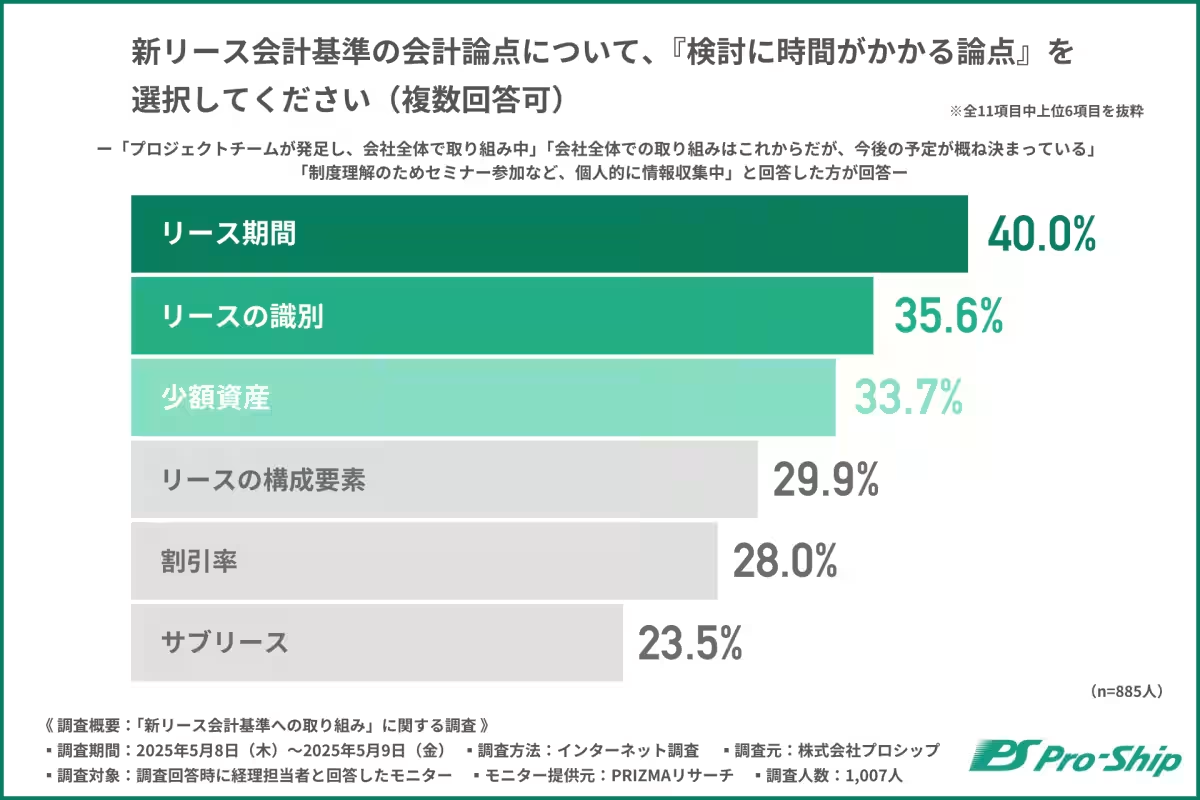

However, amidst these preparations, several pain points have been identified. When prompted about what they find challenging in relation to the new lease standards, 45.3% highlighted the estimation of impact amounts, while 44.5% mentioned organizing accounting principles as troublesome areas. Further, 39.3% pointed towards investigating and categorizing affected contracts as an arduous task.

This reveals a pronounced struggle among organizations to accurately estimate how asset, liability, and profit figures may shift under the new standards, and clarifying these impacts is viewed as a top priority.

Utilizing External Support

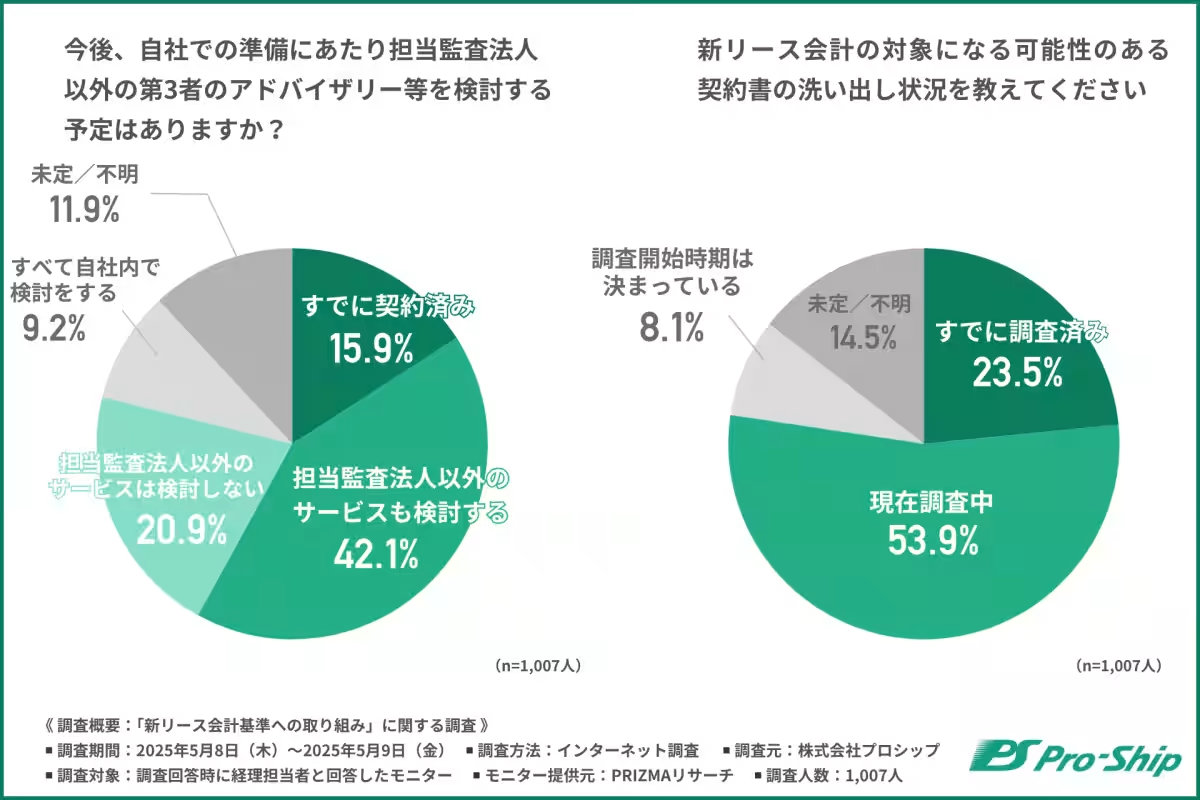

As they grapple with these concerns, many companies are considering external advisory services beyond their accounting firms. The survey revealed that approximately 58% of businesses are already engaged with or considering external support.

Current Contract Evaluation Status

When it comes to identifying relevant contracts influenced by the new standards, 23.5% have already completed evaluations, while 53.9% are currently in the process. These figures indicate that a notable majority are taking proactive steps toward compliance, although some companies still exhibit uncertainty in their timelines for evaluation.

Financial Impact Considerations

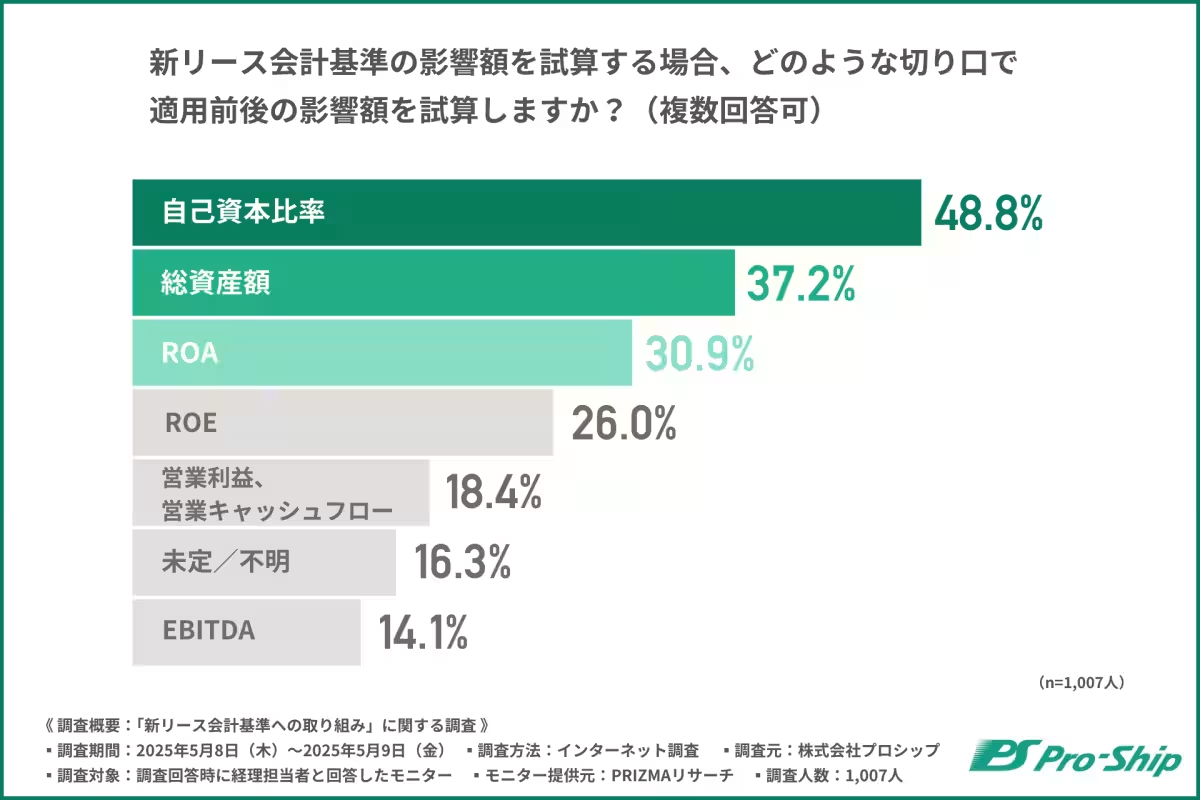

In exploring how organizations anticipate calculating the financial impacts of the new standards, the most frequently cited metrics included equity ratios (48.8%), total asset amounts (37.2%), and return on assets (30.9%). These metrics are crucial as they directly reflect financial health and stakeholder engagement, underscoring the need for precise appraisal during this transitional phase.

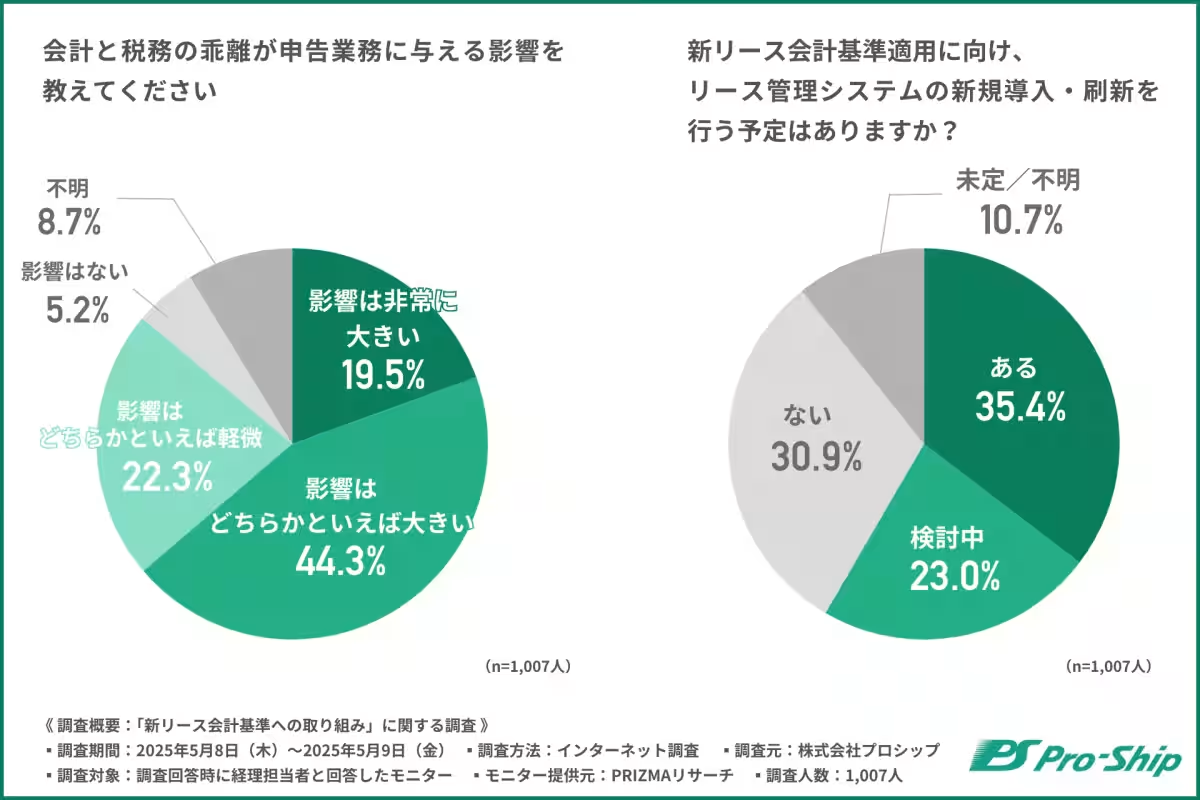

Moreover, as companies prepare for the adjustments, 63.8% anticipate significant implications for their tax filings due to the disjunction that could arise between accounting and tax regulations.

Future Technology Implementations

Furthermore, a considerable number of respondents expressed intentions to either introduce or refresh lease management systems due to the new standards. This indicates a widespread acknowledgment of the necessity for technological support in their compliance strategies.

Conclusion

In summary, while many organizations recognize the vital changes alongside the new lease accounting standards and are initiating practical measures to adapt, a disparity in preparedness levels and specific implementations remains evident. The pivotal challenge lies in estimating impact amounts and making clear interpretative decisions around various accounting principles.

For companies navigating these new regulations, taking a structured approach in organizing internal policies and preparing for the financial implications will be crucial for success. Engaging external assistance may also offer valuable guidance in overcoming adaptability hurdles effectively.

At ProShip, we are committed to supporting businesses as they transition to these new standards. With extensive experience in IFRS16 projects and an array of solutions, we offer a comprehensive process to navigate the evolving landscape of lease accounting management.

Topics Financial Services & Investing)

【About Using Articles】

You can freely use the title and article content by linking to the page where the article is posted.

※ Images cannot be used.

【About Links】

Links are free to use.